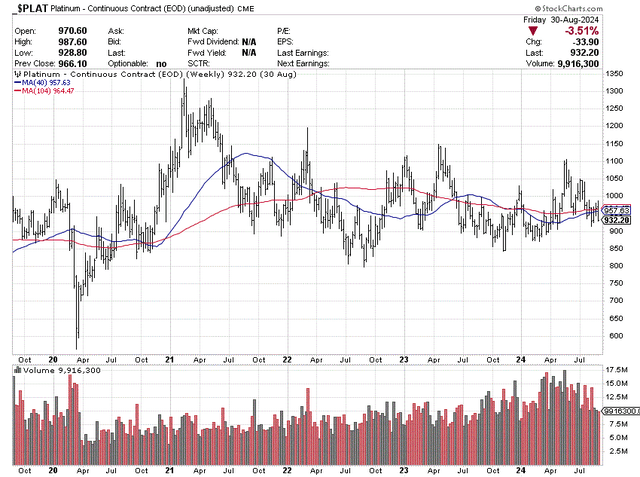

I have talked about platinum trading at an ultra-low relative valuation to other metals for almost five years on Seeking Alpha. Unfortunately, the spot bullion price still has not moved in a multi-year bull run to play catch up with other metals gains, following the record pandemic-related money-printing spree by central banks.

However, platinum’s price as a function of the value of other precious metals and a variety of base metals has gotten so out of whack with historical trading patterns, I am moving my rating into the must-own camp. With nearly all new production coming from the unstable nations of Russia and South Africa, any political hiccup or turmoil from either area of the world could ignite a spike rally in platinum, perhaps pushing its quote over US$2,000 an ounce rapidly (from $932 at Friday’s close closer to the all-time high of 2008).

StockCharts.com – Platinum Nearby Futures, Weekly Price & Volume Changes, 5 Years

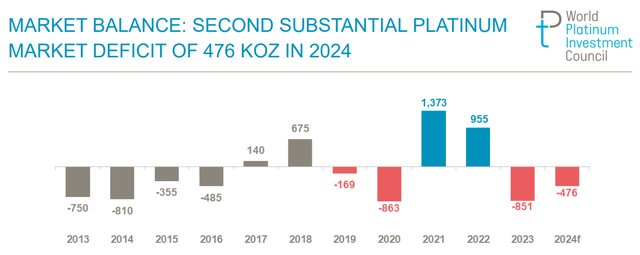

For investors in platinum, the economic surpluses of 2021-22 have reversed into shortages of supply vs. industrial and investor demand in 2023-24. A deficit of 476,000 ounces is expected for all of 2024, according to the World Platinum Investment Council. The end result of a marketplace in better balance: if any unexpected uptick in investor demand appears, dramatic price upside could be part of platinum’s future.

World Platinum Investment Council – Q1 2024 Presentation, Net Platinum Shortage

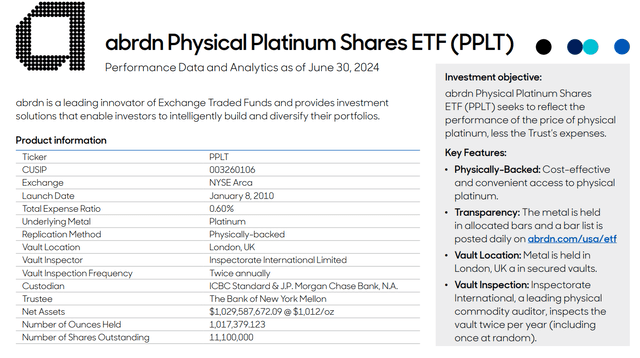

What valuation logic am I using to move the top platinum bullion ETF by AUM ($1 billion in assets) into Strong Buy territory? Let me explain the underlying bullish metal story for the abrdn Physical Platinum Shares (NYSEARCA:PPLT).

Abrdn.com – Physical Platinum Shares ETF, June 2024 Fact Sheet

Metals Price Comparisons

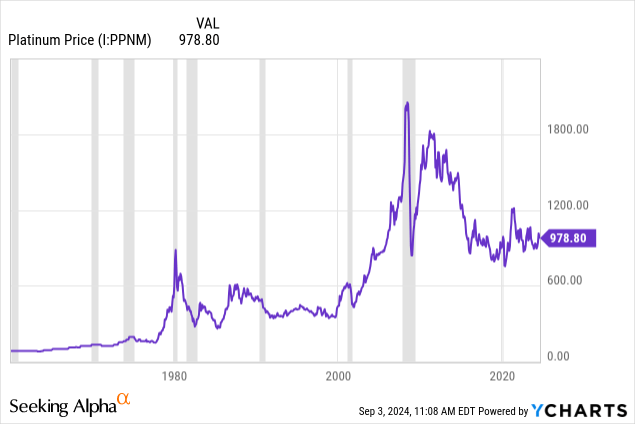

Monthly platinum prices are trading at roughly half the March 2008 quote above $2,300, while sitting at a level about the same as the March 1980 spike high of $1,050 per ounce. Why would anyone want to own a metal that has gone nowhere over 44 years?

YCharts – Platinum, US$ Price per Troy Ounce, Since 1960, Recessions Shaded

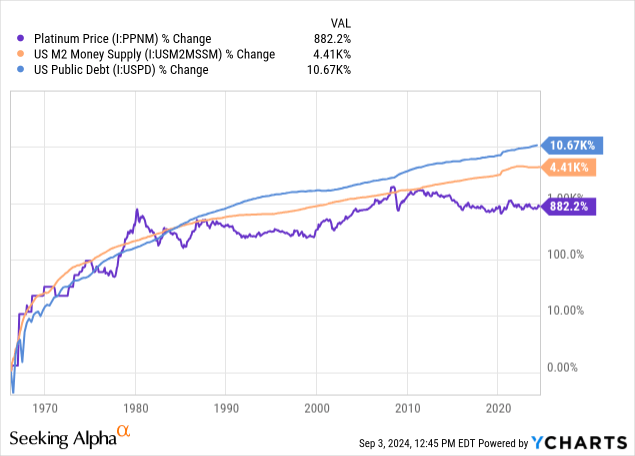

Platinum has throughout the ages been considered a monetary metal, with performance characteristics that have hedged local currency problems and inflation generally, especially over long periods of time.

On the chart below, you can review how U.S. platinum price gains in the 1960s, 1970s & 1980s largely mimicked growth in the U.S. M2 money supply and increases in Treasury debts owed by Uncle Sam (future inflation inputs if you will). However, starting around 1989 then again in 2008, platinum has been a clear laggard for investors, despite steady M2 and Treasury debts outstanding hitting growth rates of 7% to 8% annually on average.

When we compare platinum to core monetary inflation aggregates, the spread between actual price and estimates of where it should be trading are the largest in modern times during early September 2024. To get back to the M2 growth curve, price would have to rise above $4,700 per ounce (+400% gain from today), while an advance to $11,500 (+1,100%) per ounce would be necessary to catch Treasury debt expansion.

YCharts – Monthly Platinum Price vs. U.S. M2 & Treasury Debt Growth, Since 1966

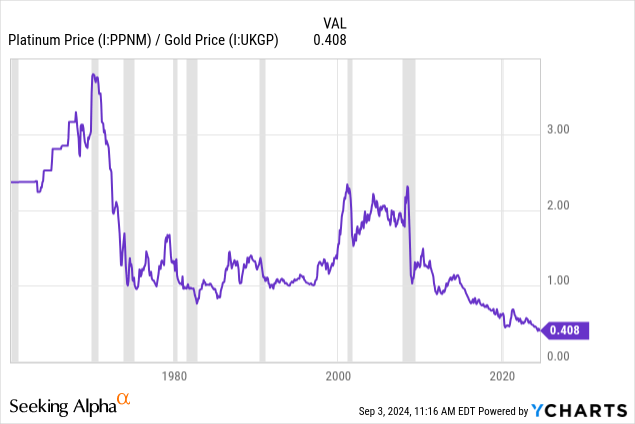

Gold

Gold and platinum have battled for the title as best monetary and wealth hedge over the centuries. With much greater scarcity on the planet, platinum has usually been priced at a premium number per ounce. Nevertheless, this traditional relationship has broken down since late 2015. The current 0.41x ratio (59% discount to gold) is a modern record low in the summer of 2024.

YCharts – Platinum to Gold Price, Since 1960, Recessions Shaded

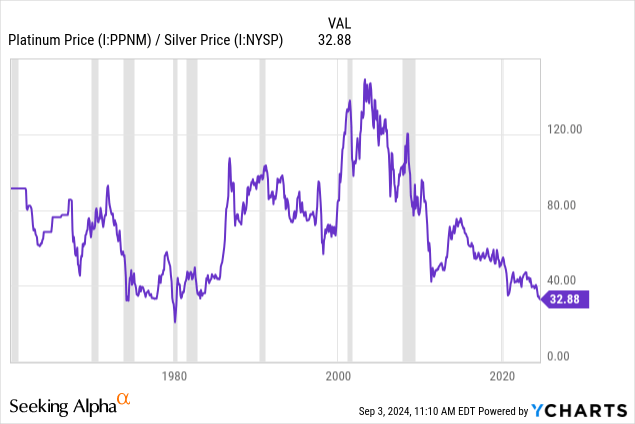

Silver

But that’s not all. Outside of the platinum group metals, silver is the closest cousin, as both metals have monetary and industrial uses/demand. Once again, the relative pricing of platinum really stands out currently. With 32.9 ounces of silver required to buy one ounce of platinum, you have to go back to a few months in early 1980 (the failed Hunt Bros. attempt to corner the silver market) to find this relationship any more skewed.

YCharts – Platinum to Silver Price, Since 1960, Recessions Shaded

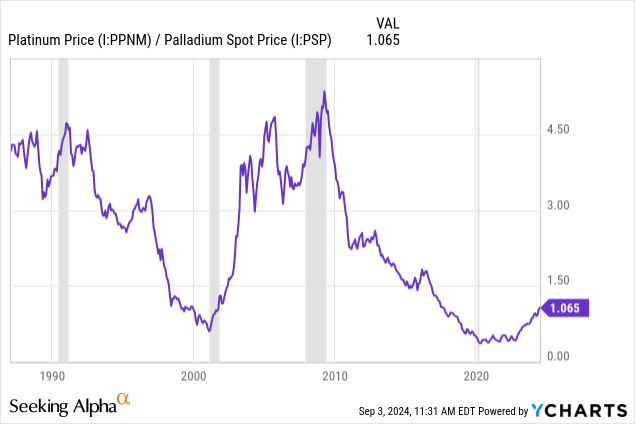

Palladium

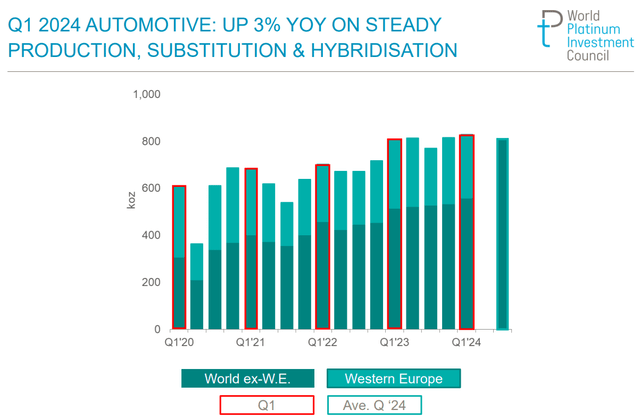

One of the reasons I felt comfortable owning platinum years ago was the super high palladium price. Platinum and palladium have battled for supremacy in the catalytic converter market for ICE automobiles. A chemical reaction from either is used to combat air pollution in gas-powered engines. With platinum being measurably cheaper, automakers have increasingly turned to platinum in new car designs. You can see how platinum demand has been rising nicely since 2020 in the auto sector below. The really good industrial-demand news is both platinum and palladium are key ingredients in many renewable and green energy products.

World Platinum Investment Council – Q1 2024 Report, Net Platinum Shortage

Historically, platinum has traded at a huge premium to palladium. With today’s quotes per ounce near parity (down from an unheard of 50% discount to palladium in the early 2020s), platinum remains a screaming buy if traditional benchmarks for a valuation come back into vogue.

YCharts – Platinum to Palladium Price, Since 1987, Recessions Shaded

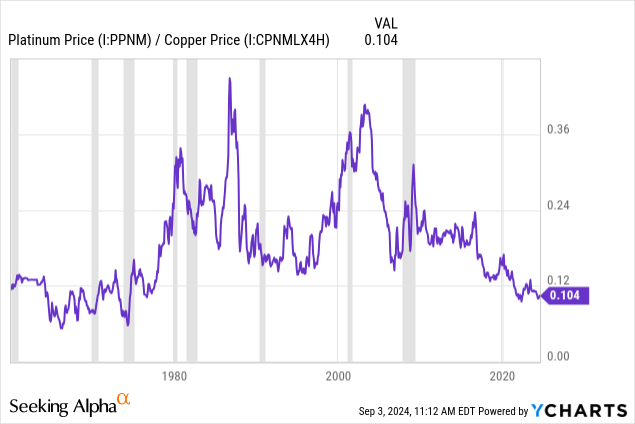

Copper

Another important industrial commodity, only a step away from being a precious metal, is copper. Below is a chart comparing the price of one ounce of platinum to one metric ton of copper. Today’s 0.10x ratio is the lowest since 1978, if you exclude a few months in 2022. That would be a 46-year low!

YCharts – Platinum Oz. to Copper Tonne Price, Since 1960, Recessions Shaded

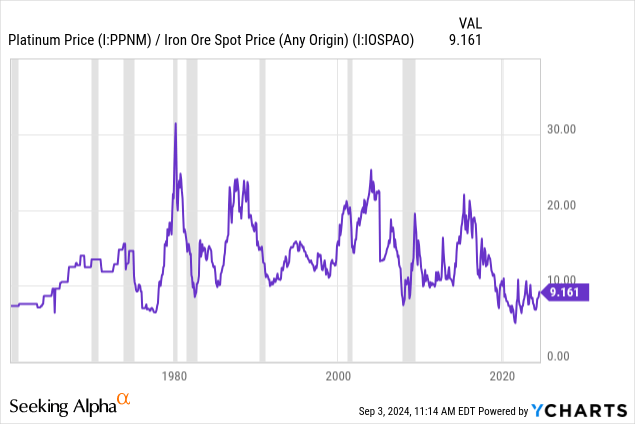

Iron Ore

Lastly, we can review iron ore values in relation to platinum. The most critical metal in heavy construction and deep cyclical manufacturing, iron is the key ingredient to make steel. The relative price chart looks very similar to copper. Platinum’s price today has only been lower about 10% of the time since 1960, with the current relative level (9.16x platinum ounces vs. iron ore metric ton) about the same as 1965.

YCharts – Platinum Oz. to Iron Ore Tonne Price, Since 1960, Recessions Shaded

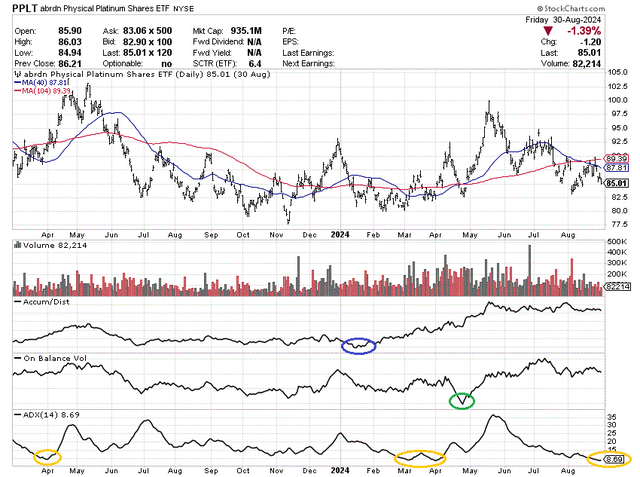

Technical Chart Looking Better

Why else am I mentioning platinum and PPLT as an investment idea? Outside of the excellent valuation arguments vs. alternative metals, the trading chart pattern is getting quite interesting. It appears to me the U.S. price bottomed early in the year. Momentum indications are improving rapidly. Plus, another round of Fed easing (starting in weeks if you believe Chairman Jerome Powell) could provide the catalyst for investment funds to flood the platinum market.

On the 18-month chart below, I have circled in blue the January Accumulation/Distribution Line bottom, alongside the On Balance Volume reversal in April (circled in green). Similarly, low 14-day Average Directional Index scores (circled in gold) are also highly correlated with price bottoms in platinum over the past five years.

StockCharts.com – abrdn PPLT, Daily Price & Volume Changes, 18 Months, Author Reference Points

Final Thoughts

Believe it or not, taking the long-term average valuation numbers from each gold, silver, palladium, copper, and iron ore (using equal weightings), platinum’s relative “fair value” today is mathematically around $2,250! So, if you can ride this important metal to such a level from $932 an ounce, gains of roughly +140% are now theoretically available in a reset upmove. Essentially, platinum is trading at a -58% discount to its relative value on other metals.

The best fundamental bullish argument may be platinum is overdue to catch up to paper money printing, potentially about to go into overdrive again if a recession is to be avoided. Using an average of M2 and Treasury IOU growth, you can easily argue a platinum price range of $5,000 to $10,000 is coming over the next 5-10 years. Don’t say that’s crazy. If gold is sitting at $3,000 or $4,000 years down the road (which is my forecast), the more typical 2.3:1 ratio of 2008 puts platinum at $6,900 to $9,200 an ounce!

I personally know individuals that like to own both gold and platinum in lieu of cash reserves, as physical bullion has no bank or currency liability marked against them. If you can handle a little price volatility, platinum today may serve as an excellent choice to add next to your CDs and money market funds. I understand you will not receive any yield holding PPLT, and the risk of loss on price declines is definitely real. However, just like gold, platinum bullion ideas can increase in value quickly during times of financial upheaval and political division, no matter the country in which you own it.

I am confident platinum will (over time) work as a terrific monetary inflation hedge, although it has been a significant laggard during the past five years. If we get a reversion-to-the-mean move with immediate production shortfalls vs. industrial demand supporting the effort, a +50% to +100% gain on your liquid reserves over 2-3 years has a decent chance of playing out.

I am using PPLT as a diversifier tool to hold in portfolio construction, just as important as my large gold/silver bullion and cash-like investments, but with greater underlying long-term value as a backstop.

What go wrong with my super bullish forecast? At this stage, I would say recession risk is the main worry. On my graphs above, I intentionally inserted recession periods in grey for readers to contemplate. Platinum doesn’t have a perfect record of declining during U.S. GDP contractions, but odds are tilted heavily in favor of such an outcome. You can go back to the 2020 economic shutdown fears during the early days of the pandemic to see how poorly platinum can perform in a bank liquidity and Wall Street trading crisis.

The good news is platinum can rebound quickly once global fiat monetary expansion gets set into motion, with the remainder of 2020 providing a large boost to platinum’s price as an example.

Anyway you cut it, buying now or later in the year could produce outstanding gains in your long-term portfolio. My plan is to cost-average into a sizable platinum position over the next couple of months. I am upgrading my 12-month rating of platinum and the abrdn Physical Platinum Shares ETF to Strong Buy.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Read the full article here