PMV Pharmaceuticals (NASDAQ:PMVP) has been in an uptrend since April as the company closes in on updated results from a phase 1/2 study of PC14586, a p53 reactivator with potential across a range of cancer types. This article takes a look at what we might expect from the data due this half from PMVP.

The PYNNACLE study and PC14586

Mutations in p53, a protein with tumor suppressing function, are present in 50 percent of cancers and PC14586 targets a particular mutation Y220C to restore normal p53 function. The Y220C mutation is present in about 1% of solid tumors.

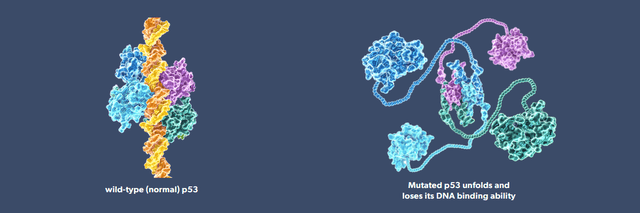

Figure 1: Normal p53 (left) has the ability to stop abnormal cells dividing, an important feature to suppress cancer. Mutated p53 loses function helping abnormal cells to divide anyway. (PMVP website)

While the Y220C mutation is just one of many that can occur within cancer, screening cancer patients to determine which, if any, p53 mutations they have allows PMVP to enroll patients in its PYNNACLE study.

PYNNACLE already produced some data from the phase 1 portion of the study in 2022. At that update, PMVP noted they had 41 patients enrolled as of May 10, 2022. In the 10 patients dosed with lower levels of PC14586 (150 mg a day – 600 mg a day), there were eight patients eligible for evaluation with four cases of stable disease and four cases of progressive disease.

At the higher doses of PC14586 (1150 mg a day to 1500 mg twice a day), from 31 patients, 25 were eligible for evaluation and six had partial responses, two had unconfirmed partial responses, 11 had stable disease and three had progressive disease. A further three weren’t evaluable due to discontinuation.

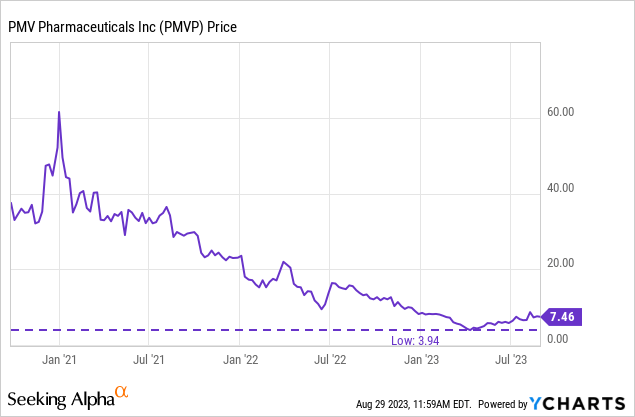

Figure 2: PMVP’s phase 1 data from the PYNNACLE study was met with a rally in June 2022, but it didn’t last. The stock found a low in April this year, perhaps as a run-up into results in H2’23, which PMVP has consistently guided to, began.

The problem with the phase 1 data to date has been discussed in multiple places. For example, Avisol Capital Partners noted that while PMVP’s PC14586 is active, the toxicity profile of the drug isn’t great. Two patients receiving 1500 mg twice daily experienced dose-limiting toxicity including grade 3 increases in liver enzymes and grade 3 acute kidney injury. PMVP determined 1500 mg twice a day as the maximum tolerated dose, and at the time the phase 1 data were shared in June 2022 noted, “Enrollment at doses below the MTD is ongoing to support the determination of a recommended Phase 2 dose.”

The very worst of the toxicity then, which seems to have limited enthusiasm around PC14586, probably won’t feature again and I think PMVP can figure out a goldilocks dose that produces enough efficacy with an acceptable side effect profile. For example, some of the best data came from a small cell lung cancer patient who experienced a partial response with 1150 mg once a day. Perhaps the highest of doses simply weren’t necessary.

More phase 1 data in H2’23

With an update expected from the phase 1 portion of the PYNNACLE trial in H2’23, PMVP will be presenting another year worth of data. From that data the company can demonstrate to the market that some of the moderate doses, lower than the 1500 mg twice a day dose, offer a balance between efficacy and toxicity that is worth developing.

Beyond the monotherapy work, PMVP is enrolling approximately 36 patients to evaluate a combination of PC14586 and Merck’s (MRK) PD-1 inhibitor Keytruda (pembrolizumab).

Further, as PYNNACLE is a phase 1/2 study, the phase 2 portion will get underway as the monotherapy portion of phase 1 concludes enrolment. PMVP’s Q2’23 earnings press release confirms the company has concluded its end of phase 1 meeting with the FDA, and there is an alignment on the recommended phase 2 dose. While PMVP hasn’t specified this dose in the press release, I suspect PMVP will announce this with the updated phase 1 data. The company notes it plans to start that phase 2 work in early 2024.

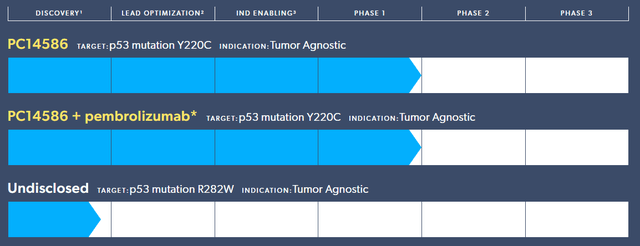

Figure 3: PMVP’s pipeline. (PMVP website.)

Financial overview

PMVP had $218.8M in cash, cash equivalents and marketable securities as of June 30, 2023. R&D expenses were $13.8M in Q2’23, with G&A expenses of $6.3M in the same quarter. Net loss was $17.4M for Q2’23 and net cash used in operating activities was $27.9M in the first six months of 2023. At this rate, then, PMVP could continue on for over 3 and a half years before running out of cash. Of course the start of phase 2 work should come with an increase in cash burn, but I still don’t see PMVP having any issues with cash anytime soon. As of August 7, 2023, there were 48,454,582 shares of PMVP’s common stock outstanding, corresponding to a market cap of $360.5M ($7.44 per share).

Summary and risks

I rate PMVP a buy based on three factors. Firstly, I think the company is likely to be able to show more partial responses at doses away from the highest doses, where the toxicity profile is more acceptable. Secondly, success with PC14586 provides confirmation for PMVP’s ability to develop p53 reactivators. Lastly, PMVP has plenty of cash, which reduces uncertainty over funding for its phase 2 work.

The clearest risk to me is that if the market doesn’t like the updated phase 1 data from PMVP, the stock can easily fall to cash ~$4.50 per share, or below. Especially since the company is planning on going to phase 2, the market could view that as a waste of money.

Further, subsequent work can uncover new toxicity issues that might concern the market or even result in clinical holds on certain doses.

Lastly, other companies have worked in the p53 space previously and renewed efforts in the space could signal competition for PMVP.

Read the full article here