Since my previous article on the stock, Polaris Inc. (NYSE:PII) has reported three quarters of financials, starting to show more earnings turbulence due to a weaker macroeconomic backdrop. The company guides for some continued weakness during 2024, but I believe that the persisting macroeconomic uncertainty warrants skepticism around Polaris’ ability to achieve the guidance.

In the previous article, titled “Polaris: Cheaper Than Before, But Still Not At A Discount”, I initiated the stock at Hold as the valuation seemed fair in light of Polaris’ debt and cyclical nature despite a lower-than-historical P/E. The article was published on the 4th of October, and since, the stock has had a total return of -20% compared to the S&P 500’s great return of 30%. As I believe the long-term investment case to stand nearly as strong, I believe that the valuation is starting to get more attractive.

My Rating History on PII (Seeking Alpha)

Recent Financial Performance Shows Consumer Weakness

After my previous article, Polaris has reported the second half of 2023 and Q1 in 2024. The company has begun to show financial weakness – revenues started to fall in Q3 with a decline of -3.9%, -4.8% in Q4, and have now deepened into -20.3% in Q1.

The weak demand that Polaris started to see during 2023 related to an increasingly cautious consumer environment weakened in the first quarter, as marine sales fell dramatically by -53% year-over-year. Responsible for the majority of Polaris’ sales, off-road products performed better with -16%. On-road sales performed the best with -14%, still showing increasing weakness.

So far, Polaris’ earnings have still been relatively resilient as the operating margin stands at a current 6.7%, still surprisingly near the 8.6% average from 2018 to 2022. Polaris has had good cost control, as the company expects to achieve $150 million in operational savings in 2024 – the cyclical nature of Polaris’ products has been partly softened with good cost flexibility. The company still anticipates further declines in 2024 as macroeconomic uncertainty persists, though, and further margin declines seem likely. In Q1, as revenues had the most dramatic fall so far, the margin declined by 5.1 percentage points year-over-year.

The Financial Turbulence Seems to Last Longer Than Guided For

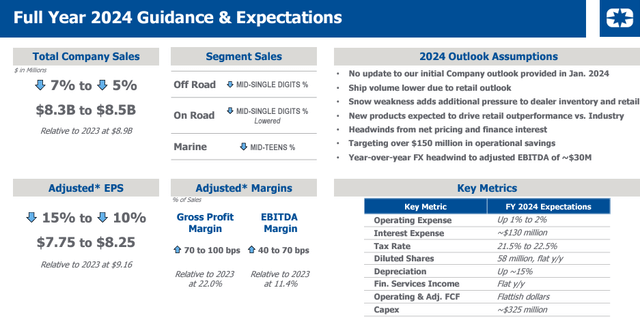

Polaris reaffirmed the company’s 2024 outlook with the Q1 report, and still expects sales to fall by -5% to -7% in the year into $8.3-8.5 billion. The current trailing sales of $8.49 billion only imply the sales to fall by around $91.1 million in the rest of 2024 compared to 2023 financials – it seems that very good gradual improvements are expected in the back half of the year.

Polaris Q1/2024 Investor Presentation

I believe that the outlook has a good likelihood of being lowered during the year as the industry continues to face challenges. For example, BRP (DOOO), a large powersports vehicle and marine product manufacturer which I recently wrote an article on, lowered the company’s guidance regarding the ongoing fiscal year with its Q1/FY2025 results. BRP now expects year-round products’ sales to fall by -7% to -10%, seasonal products’ by -26% to -28%, and marine products’ dramatically by -40% to 50% – the guidance expects a significantly worse revenue performance than Polaris despite a similar sales performance in the quarter. High dealers’ floorplan interest as interest rates persist high, and continued weak customer sentiment are still driving poor demand.

Especially the marine mid-teens downward sales outlook looks to be too optimistic – boat manufacturer Marine Products’ (MPX) sales are expected to fall by -28.5% in 2024, Malibu Boats’ (MBUU) by -40.4% in FY2024, and MasterCraft’s (MCFT) by -45.2% in FY2024. Notably, all the mentioned boat manufacturers performed better than Polaris in marine sales in the quarter from January to March.

Polaris does have some positive drivers in 2024 ahead with the launch of Indian Scout and MY’25 RANGER expected to affect Q2 deliveries positively. With the company’s long-term market share growth in mind, a performance stronger than the industry’s could still happen. The outlook expects quite a dramatic improvement, seeming too optimistic, though.

A lowered outlook wouldn’t necessarily deteriorate Polaris as a long-term investment as the lower sales are seen throughout the industry, but a potentially lowered outlook still adds notably to short-term stock price risks and the company’s earnings outlook turbulence.

Polaris’ Valuation Is Starting to Get Attractive

As the stock has fallen from my previous discounted cash flow model due to temporary headwinds, the valuation has started to get more attractive.

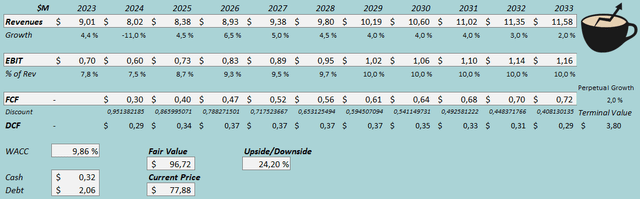

In my updated DCF model, I now estimate a revenue decline of -11% in 2024, lower than Polaris’ outlook suggests as the industry’s struggles seem to persist. Afterwards, I estimate a gradual recovery into similar growth as before, representing a revenue CAGR of 4.2% from 2024 to 2033, similar to my prior estimates.

I now also estimate more margin pressure in the short term than Polaris seems to expect with a 7.5% EBIT margin in 2024. Afterwards, I still estimate margin expansion back into 10.0%, nearly the same as the 10.4% previously. Due to the short-term weakness, though, the cash flows end up at a moderately lower level in the long-term as well in my new estimates.

DCF Model (Author’s Calculation)

The estimates put Polaris’ fair value estimates at $96.72, 24% above the stock price at the time of writing – the valuation is starting to get attractive. Still, as the outlook could well be lowered during the year even more than I anticipate, potentially causing further stock & earnings turbulence, I believe that caution is still needed for the time being. The fair value estimate is up from $91.63 previously due to a lower WACC.

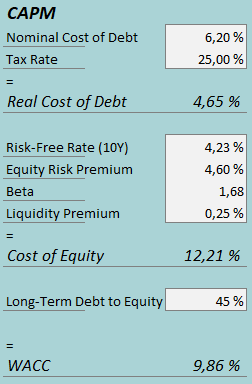

A weighted average cost of capital of 9.86% is used in the DCF model. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q1, Polaris had $31.9 million in interest expenses, making the company’s interest rate 6.20% with the current amount of interest-bearing debt. I now estimate a higher debt-to-equity of 45% compared to 25% previously due to a lower equity valuation and remaining high debt.

To estimate the cost of equity, I use the United States’ 10-year bond yield of 4.23% as the risk-free rate. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the United States, updated on the 5th of January. I have kept the beta estimate the same as previously at 1.68. Finally, I add a liquidity premium of 0.25%, creating a cost of equity of 12.21% and a WACC of 9.86%. The WACC is down from 12.32% previously due to lower expected market returns.

Takeaway

Polaris has started to report weaker demand after my previous article on the company, as the company started to predict in 2023. The weakness has also persisted in 2024 so far with the deepest decline so far seen in Q1. While Polaris’ outlook expects quite a stable rest of 2024, but I believe that the outlook could be too optimistic with a good likelihood – other companies in the industry have continued reporting weaker revenues and are expected to perform poorly in upcoming quarters, well below Polaris’ own expectations. The valuation is starting to get attractive as the stock has fallen, but due to the short-term turbulence, I maintain my rating for Polaris at Hold.

Read the full article here