Yatra Online, Inc. (YTRA) is the third-largest online travel agency in India based on 2023 booking and operating revenue. It also has the largest corporate contract travel business in India with over 800 large and 56k small business partners plus an indirect network of over 53k live agents. The firm operates a common and scalable technology platform offering both a website and mobile front end that helps one intuitively book air, hotel, train, car, holiday packages and other travel needs. Major competitors include MakeMytrip (MMYT) and Cleartrip (private) as well as major international firms such as Booking.com (BKNG).

Macro:

“India’s domestic air passenger traffic is expected to double in the next six years, reaching 300 million by the end of 2030.”

– India Civil Aviation Minister Jyotiraditya Scindia.

India is considered the fastest growing large travel market in the world. Its travel business has been growing at roughly 12-14% per year, 1.5 – 2x the country’s stellar 7.5% GDP growth rate. Calendar 2024 travel growth is once again expected to be in the low to mid-teens.

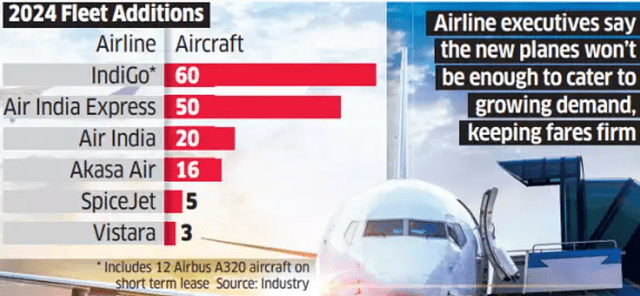

This greater than GDP growth is because the country’s middle class is expanding as a % of the whole (market penetration is expected to grow from 7.8% to 10% over the next four years) and because India has been significantly increasing its travel infrastructure. This includes new airports, growth of existing airports, and significant airline fleet growth. In 2024 alone, India’s air fleet is scheduled to grow by 150 planes.

economictimes.indiatimes.com/industry/transportation/airlines-/-aviation/indian-airlines-set-to-soar-over-150-aircraft-to-join-fleet-in-2024-but-it-might-not-be-enough/articleshow/106586443.cms?from=mdr

Importantly, a higher proportion of this travel is also booked online each year. In 2015, the percentage of all India bookings done online was 43%. This year, Yatra estimates the online percentage of the market reached 65%. By 2025 it is estimated to exceed 70%. In other words, not only is India the fastest growing major travel market in the world, but Yatra’s online solution is gaining significant share in that market.

Yatra:

As the third-largest India Online Travel Agency “OTA,” and a much smaller player than international heavyweights Expedia and Booking.com, YTRA does not yet enjoy the economies of scale of the larger firms. As already stated, it, however, has been gaining market share in the sweet spot (online) of the fastest growing major travel segment in the world, India. Air passenger bookings were up 24% in FY’24, almost double India’s overall 12% – 14% travel growth, and the firm is estimated to experience higher revenue growth next year than any other firm in the industry.

www.stockrover.com/cash-flow-kingdom/

Yatra also now boasts the largest corporate travel base (849 large corporations) and deepest bench of hotel offerings in India (108k hotels). This allows both its direct to consumer and corporate passengers to one-stop shop for air, train, road and hotel travel needs via the Yatra software platform.

s22.q4cdn.com/850749348/files/doc_presentations/2024/May/30/yatra-investor-presentation-may-2024.pdf

Yatra’s latest new software updates also integrate corporate expense management with the booking platform, further encouraging corporate stickiness (Yatra enjoys a 98% corporate customer retention rate).

The overall increased cross-selling ability and improved technology scalability of its platform has helped it to take market share in this growing market and to reduce fixed costs from 38.2% of adjusted Revenue in 2019 (Pre-Covid) to about 28% today.

That in turn has recently turned the firm profitable. Q4 EBITDA was positive at 110 million INR ($1.3 million USD). That increased cash flow, however, has been plowed back into R&D, capacity increases and working capital to maximize the growth opportunity. In particular, the growth in accounts receivable and long DSO period it provides to customers have been sucking up cash.

Nevertheless, Yatra’s debt was reduced 58% over the last year by proceeds from the India IPO with cash on hand, growing to $54 million USD. This helps control the ongoing risk inherent in this high-growth situation.

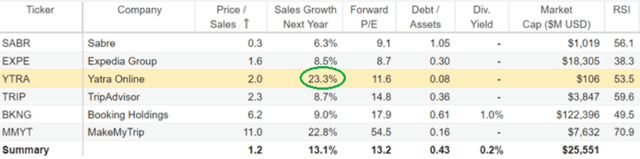

Valuation:

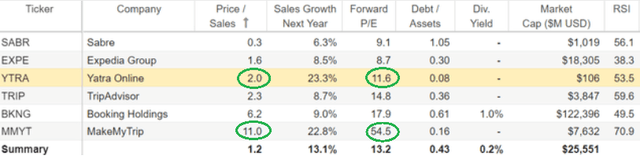

Yatra is not cheap in a general sense, but it is a bargain relative to their main high-growth India competitor, MMYT.

www.stockrover.com/cash-flow-kingdom/

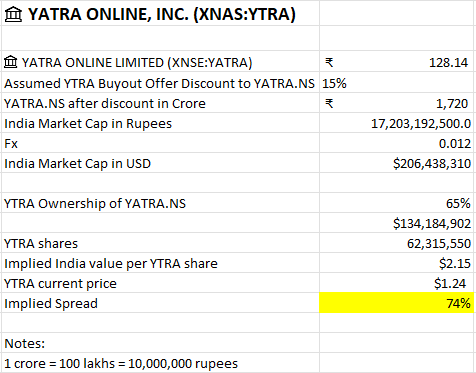

Importantly, YTRA’s US shares are also significantly underpriced compared to what their shares trade for in India (Yatra Online Limited; YATRA.NS, YATRA.BO).

Author’s Spreadsheet, and Yahoo Finance data

This valuation disparity is probably because, as an Indian focused travel firm, they and their prospects are much better known in India than in the US. Hence, India shareholders are simply willing to pay more for a firm they realize has excellent prospects.

This spread between the US YTRA shares and the India YATRA.NS shares is important because it may represent an opportunity. While the two are not currently fungible, management is pursuing remedies to make them more so. They have an incentive to do so in part because 10-15% of the US YTRA shares are held by insiders (including the CEO and Co-Founder Dhruv Shringi) and another 20% is owned by MAK Capital (whose CEO Michael Anthony Kaufman sits on Yatra’s board).

In reducing the YTRA/YATRA.NS spread, any remedy therefore also likely has a goal of increasing the value of YTRA shares. Further supporting an expected resolution to this problem is a 6k filing which Cash Flow Club member GK_1 pointed out last Friday and a press release Monday morning. It gave a big hint as to what a potential remedy might be,

“The board of directors (the “board”) of Yatra Online, Inc. (the “Company”) is looking to explore certain strategic options regarding simplifying the Company’s multi-jurisdictional corporate structure and in that direction has established an independent committee of the board (the “committee”). The committee is expected to engage with industry experts, legal counsel, regulatory bodies, and other stakeholders to gather insights, perspectives, and requirements for approval on any proposed corporate structural changes.

After such review, the committee will develop a set of strategic recommendations for the board that outline potential pathways, the anticipated benefits, and any associated risks or challenges. The committee will aim for a plan that can reduce administrative overhead, rationalize costs, and facilitate organic and inorganic growth for the Company.

There is no assurance that the Company will necessarily take any near-term course of action, or will pursue any recommended plan.”

A potential solution that would help in “simplifying the Company’s multi-jurisdictional corporate structure” and “reduce administrative overhead, rationalize costs, and facilitate organic and inorganic growth for the Company” is to grow the YATRA.NS floating share count (YTRA owns 101 million YATRA.NS shares) and use the proceeds to repurchase and delist all the US YTRA shares.

Yatra would thus focus their listing where it is more highly known and valued, the India stock market. In doing so, they would both eliminate meaningful US market registration cost and the time, hassle and cost of having to prepare two separate sets of financials (GAAP accounting is used in the US, IFRS accounting is used in India).

The process could potentially be accomplished by engaging Wall Street to buy YATRA.NS shares (at an assumed 10% discount to current price) and using the proceeds to make an offer to buy up and delist all US YTRA shares (at an assumed 5% in friction costs for a total discount of 15% off the YATRA.NS current price). I estimate however that this process might take about 6 months to fully accomplish, as well as a positive vote from 67%+ of YTRA shareholders. So, one still needs to be happy with the general India travel opportunity in case things don’t go as planned or take longer than expected.

We, of course, don’t know that any of this will happen. The press release may be telling, but it is not binding nor guaranteed. So, for now, YTRA remains a speculative opportunity.

I note, for instance, there is another potential alternative the firm could instead choose to implement. That being to put in place the equivalent of an ATM “At the Money” facility, which periodically sells new shares in India and uses the proceeds to gradually repurchase YTRA shares at market in the US. This wouldn’t cut complexity or costs, one of their stated goals in the press release, but over time it would still likely be supportive for YTRA shareholders.

Regardless, one can see in the spreadsheet provided above, that the current 74% difference between YTRA and YATRA.NS (even assuming a 15% friction loss) is compelling enough for one to consider taking on the risk.

Take Away:

Yatra’s is taking market share in the fastest growing major travel market in the world, India. However, its cash flow is being used to foster this growth instead of directly rewarding investors via dividends and/or share buybacks. Thus, YTRA is not your typical Cash Flow Club stock.

We, however, still choose to own it because the firm is both an excellent growth opportunity and there is a potentially significant trigger in the near to intermediate term. That trigger being the potential that management will find a way to successfully close the spread between US YTRA vs. India YATRA.NS shares.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here