Welcome to another installment of our Preferreds Market Weekly Review, where we discuss preferred stock and baby bond market activity from both the bottom-up, highlighting individual news and events, as well as top-down, providing an overview of the broader market. We also try to add some historical context as well as relevant themes that look to be driving markets or that investors ought to be mindful of. This update covers the period through the first week of July.

Be sure to check out our other weekly updates covering the business development company (“BDC”) as well as the closed-end fund (“CEF”) markets for perspectives across the broader income space.

Market Action

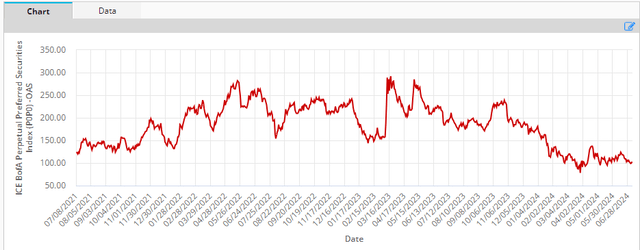

Preferreds enjoyed a solid week as a result of the drop in Treasury yields. Credit spreads have range traded near their tightest level in several years.

ICE

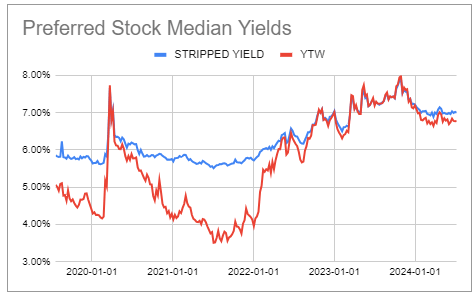

Yields have been fairly stable this year, with the median yield-to-worst trading a bit below 7%.

Systematic Income Preferreds Tool

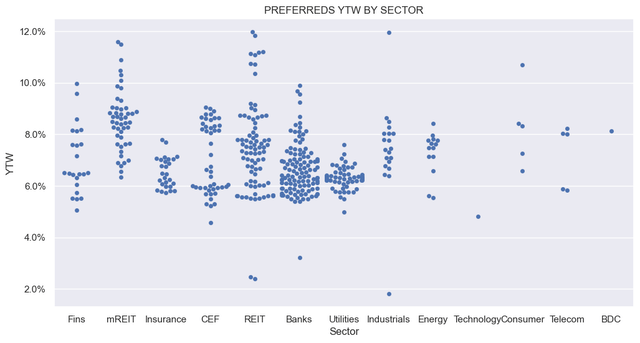

REIT and mortgage REIT preferreds continue to offer the highest yields across the preferreds space, while Banks and Utilities are trading at relatively low yield levels.

Systematic Income

Market Themes

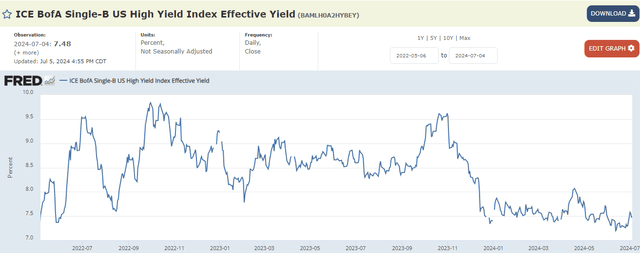

Corporate bond yields are trading at their lowest levels in over 2 years as a result of very tight credit spreads and range-bound Treasury yields.

FRED

CEF OXLC has priced its new bond (OXLCI) which will have an 8.75% coupon and a 2030 maturity. This is significantly higher than the 8% or so yields on the two existing bonds (OXLCZ, OXLCL) and it would make a lot of sense to switch or to buy OXLCI outright. OXLC bonds offer very attractive risk / reward within the broader CLO CEF / BDC senior security sector.

The latest bond (NEWTG) from Bank Newtek looks favorable against the other 3 bonds at an 8.7% yield. Recall NEWT used to be a BDC which converted to a Bank a few years ago.

The 9% 2029 bond (RWTO) was just issued by mortgage REIT Redwood Trust, which allocates primarily to single and multifamily bridge loans. It’s trading at a yield slightly below its sister bond RWTN at a 9.3% yield.

Mortgage REIT NYMT is issuing a 9.125% 2029 bond (NYMTI). This adds to the recent bond issuance by mortgage REITs from MFA and MITT. NYMT is interesting because they have been sharply growing their Agency holdings – fairly unusual for a historical credit mortgage REIT. And although recourse leverage has grown, that’s largely because of the Agency holdings.

Outside of the Agency holdings, recourse leverage is very low as much of the remaining financing is in securitized form. Agencies are a good diversifier in the portfolio as it also provides the company an ability to deleverage quickly as Agencies will remain liquid even in very difficult markets, as was the case during COVID. Specified pools which NYMT holds are not as liquid as Agency TBA, but they’re miles better in a downturn than anything with a whiff of credit in it. Despite significant derisking in its portfolio, the bond is trading at a hefty 9% yield.

Stance And Takeaways

Some of this recent issuance in the baby bond space looks very compelling, not just in terms of absolute yields – near or above 9% – but also in terms of risk / reward. We particularly like NYMTI and OXLCI. We have recently added NYMTI to our Income Portfolios, and we are waiting for OXLCI to start trading, at which point it will likely find a place there as well.

Check out Systematic Income and explore our Income Portfolios, engineered with both yield and risk management considerations.

Use our powerful Interactive Investor Tools to navigate the BDC, CEF, OEF, preferred and baby bond markets.

Read our Investor Guides: to CEFs, Preferreds and PIMCO CEFs.

Check us out on a no-risk basis – sign up for a 2-week free trial!

Read the full article here