Investment Summary

There is tremendous value to be unlocked in buying the equity stock of Profound Medical Corp. (NASDAQ:PROF) in my informed opinion. As I’ve discussed ad infinitum in my previous coverage (listed below), the company’s TULSA-PRO segment has the potential to create a systematic and remedial breakthrough in the surgical treatment of prostate disease (“PD”). I have positioned against selective PD names over the past 12 months with varying results, having to remain very active on each of the issues to avoid losses. I am also long of EDAP TMS S.A. (EDAP) on this thematic, which I would encourage all to compare and contrast here to PROF stock.

Previous PROF publications dating back to 2020:

- Upsides into FY22 earnings, revise to buy

- Profound Medical’s TULSA-PRO: Potential For Remedial Breakthrough In Complex Segment

- Profound Medical Lacks Conviction To Overthrow Macro Headwinds

- Profound Medical: Awaiting Positive Movement On TULSA-PRO Numbers

Collectively, there is sufficient evidence on my investment criteria to reiterate PROF as buy. I advocate to go long of PROF stock in order to buy the TULSA-PRO system and the tail of asset returns I believe it can generate over the years to come. It is an inflection point for the company for sure, and the market’s rating of the company reflects these prospects. Net-net, reiterate buy at $19 per share valuation.

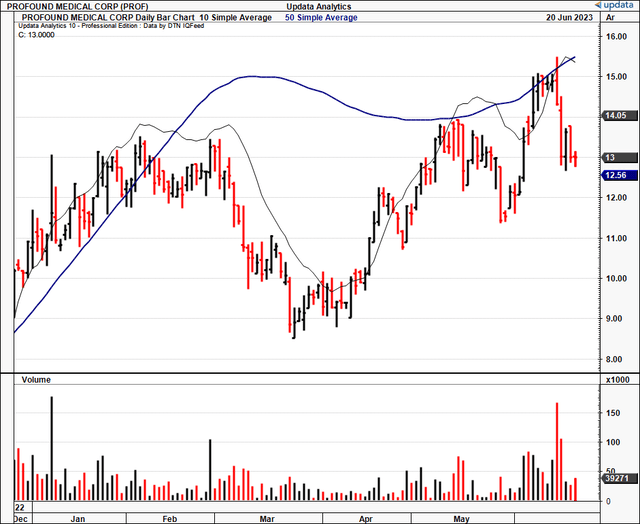

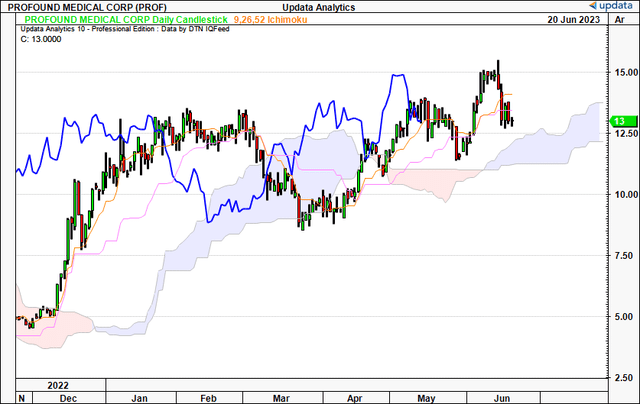

Figure 1. PROF recent price performance

Data: Updata

Critical facts forming buy thesis

There are 3 fundamental tailwinds building for PROF which make it an attractive investment:

One, its TULSA-PRO units are now on the market generating recurring and capital revenues. Already we are witnessing impressive growth numbers, indicating the market’s uptake.

Two, the firm’s gross profitability has spiked alongside the spike in sales and asset growth. This is telling of the productivity to expect from the firm’s capital moving forward.

Three, the economics of the underlying PD treatment market are attractive, forecast to grow at 8–10% annually into 2030, with players such as PROF key to driving that number. Each of these requires further discussion to illustrate where the value lies for PROF.

1. PD market economics

The PD treatment market is a critical segment of the healthcare industry and isn’t going anywhere, considering around 50% of the global population have a prostate gland.

The PD therapeutics market is marred by unmet clinical needs and the equal need for a remedial breakthrough in the way of treatment. These suppositions are underscored by findings presented in the 2023 Annual Report on Prostate Diseases from Harvard Health. The report alludes to the pervasive impact of prostate-related afflictions on the male populous, and the pressing need for efficacious solutions. I have discussed this ad nauseum in previous PROF publications. The fact of the matter is that outcomes post-prostate surgery are terrible. Mainly, factors of incontinence, erectile dysfunction and severe loss of quality of life are the common symptoms.

Thanks to the many recent developments in the field (and there have been many), forecasts project anywhere from 8.5% to c.10% in annual compounding growth, to reach a market valuation of $48 to 92Bn by 2027–2030. In parallel, an array of therapy types has emerged, TULSA-PRO being one of these. This is attractive for any medical market especially one that has a total addressable market of potentially 50% of the population. Importantly, the utilization trends PROF is witnessing thus far are matching the market’s growth rates as will be discussed later. Nevertheless, the underlying economics of the PD treatment market remain a bullish factor in the investment debate.

2. PROF business economics

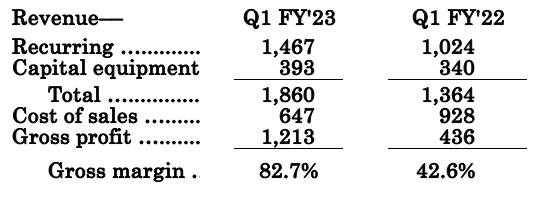

The company clipped Q1 revenue of $1.9mm, up 36% YoY and well ahead of the PD market’s forecasts, indicating it likely took market share in my view. It pulled this down to a quarterly net loss of $6.8mm. Of particular interest was the increase in recurring revenue, which soared by 43% to reach ~$1.5mm, while the one-time sale of capital equipment experienced a solid 16% growth as well to c.$400,000.

Further, the company’s business model is fairly efficient and has potential to drive operating leverage when at scale. It generates $8,000 per patient/per procedure. That implies that in Q1 it did 238 procedures, up from an implied 128 in Q1 last year.

Very importantly in my eyes– it pulled this to an 82.7% gross margin, nearly double that of Q1 last year. This is telling of the company’s ability to make money. Whilst the revenue clip is still tight, (~$8–$10mm annualized), it is much better to collect ~83% than 42.5% on this.

Table 1.

Data: Author, PROF SEC Filings

Disaggregating the top-line into the drivers of revenue change:

- Recurring revenue, that books consumable sales of the TULSA-PRO, along with medical device leasing, procedures, and ancillary services, witnessed a significant upswing of 43% to ~$1.5mm.

- Capital revenue, which is booked as one-time sales of capital equipment, was up 16%, to $393,000.

Looking forward, you’d want to be paying very close attention to both metrics. Number (1) says of the amount of utilization of each TULSA-PRO that is already placed. Whereas number (2) says of how many new placements PROF made during the period. Moving down the P&L, the firm increased its R&D investment by 21%, and committed an additional $3.8mm to its growth programs.

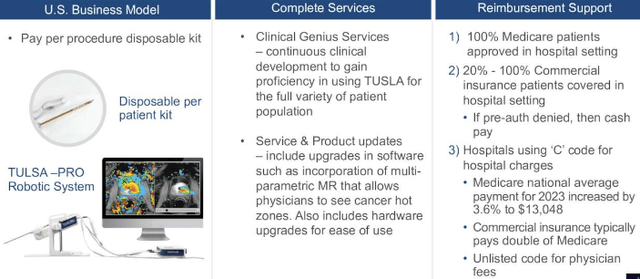

Figure 2.

Data: PROF Investor presentation

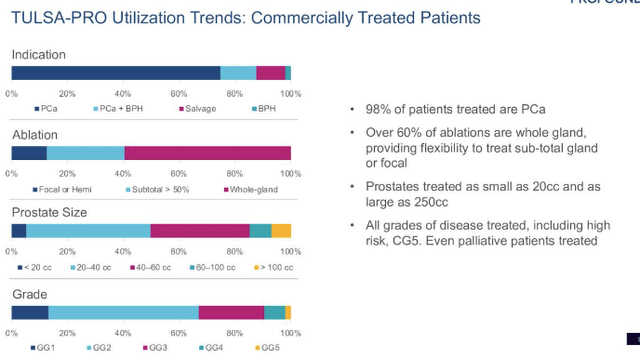

Some intriguing trends are observed when looking at utilization trends now the firm is selling its TULSA-PRO units. In Figure 3, it shows that:

- Q1 prostate cancer treatment comprised ~72% of the cases. The other 23% comprised hybrid patients, i.e., those with cancer and benign prostatic hyperplasia (“BPH”).

- Salvage treatments accounted for 5% of the total cases.

- These results are telling. It highlights a strengthening trend towards employing TULSA in a more diverse group of patients, versus just those candidates for surgery– specifically:

- Those patients who are under active surveillance,

- Those exhibiting patients in-line with BPH.

- Hence, this puts TULSA-PRO in the picture as a potential leading choice for clinicians opting for minimally invasive treatment for their PD patients. And the push from surgeons nowadays is minimally invasive, for better outcomes, and faster surgical times.

- In addition to the above, the TULSA-PRO procedure also enables surgeons to perform 2–3 procedures per day, versus the current standard of surgery where only 1–2 maximum can be performed. This is a potential tailwind to utilization in my view.

Figure 3.

Data: PROF Investor presentation

Market generated data

Much is gleaned from observing what active PROF investors have worked into the company’s market price. You can see a couple of very interesting points on Figure 4 and Figure 5, [ (4) and (5) from hereon in].

Looking at the daily cloud chart in (4), PROF is trading above the cloud and the lagging line with it in bullish territory. This tells me the trend is likely still bullish, and we can afford yet a small pullback from here and still remain on trend. I would be looking to $13 as a key support zone from here. However, this is telling. It shows the directional bias of investors controlling PROF at the moment is bullish.

Figure 4.

Data: Updata

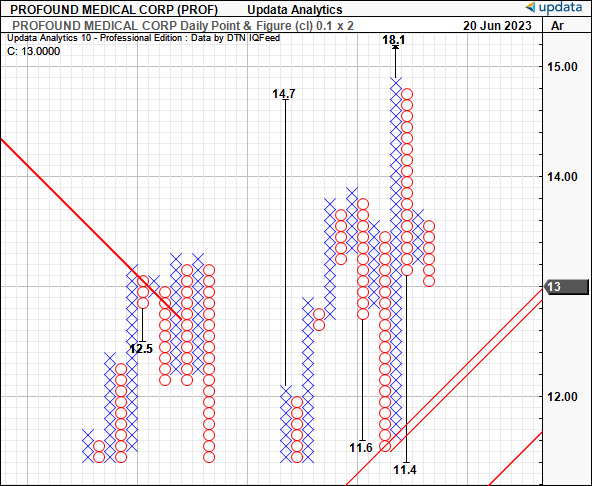

Turning to (5), you can see we have upside targets to $18.10 on the point and figure studies. These are excellent uses of data as they show the directional bias of a trend by removing the intra-trend noise (volatility) and time. This provides a cleaner view of the price action, and therefore, arguably, the market’s expectations on PROF. Given the presence of the upside target, a move higher would be confirmatory on this. However, there is also a downside target to $11.40 that must be considered as well, and thus a push lower could see us heading to this level if hands get tired. I would say this is one potential risk in the debate here.

Figure 5.

Data: Updata.

Valuation

The market is paying high multiples to buy PROF and investors aren’t letting go of their stock so easily, charging 5x book value of 19x forward sales to do so. Therein lies the dilemma. On face value, 5x forward the net asset value of the company is a dichotomous position to be– on the one hand, the market values the company’s equity by that much, on the other, PROF hasn’t really invested a whole lot of capital to justify this– all assuming no growth.

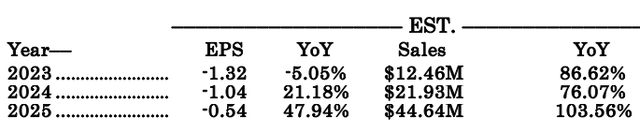

What needs to be factored is the points raised so far in this report, and projected growth numbers. My assumptions have the firm to grow revenues by ~87% this year, climbing to a >100% growth in turnover by 2025. Further, the company’s market value closely tracks the value of its operating assets. An uptick in asset growth would also be positive for the company’s valuation.

Hence, at 19x forward sales, you’re getting to $19 per share in equity value on my FY’24 assumptions, ~50% upside potential on the current market price. This is directly in-line with the technical targets obtained above, adding confidence. This supports a buy rating.

Table 2. PROF growth assumptions

Data: Author Estimates

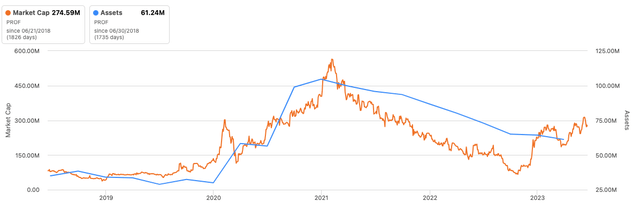

Figure 6.

Data: Seeking Alpha

In short

After extensively reviewing the moving parts in the PROF investment debate, I believe there is sufficient evidence to remain bullish on the company’s future prospects. It is building momentum around its TULSA-PRO division in growing recurring and capital revenues. Further, growth is forecast at attractive rates into FY’25, getting me to a $19 per share valuation. Despite the pricey multiples, I believe these will re-rate to be worth it over time. Net-net, given the culmination of factors discussed here, reiterate buy.

Risks to investment thesis

Before proceeding with any investment decision, investors must recognize the following risks:

1. There is risk the company may not convert on its TULSA-PRO ambitions, and fail to sell more units. This would dampen the thesis entirely, as much of the growth hinges on the firm’s ability to place more units.

2. There are market risks to consider too given PROF’s small cap size, especially with macro risks that could cause markets to swing without a change in company fundamentals.

3. There is a risk that PROF will require additional funding to finance its operations given it is not profitable. This could lead to equity dilution, and see investors sell shares as a reaction.

4. General market risks must be identified too, including the facts of interest rates, inflation and potential slowdown in economic growth.

Investors must recognize these risks in full before proceeding any further.

Read the full article here