When I first covered Progressive (NYSE:PGR), I warned that the stock had been steadily pumped up as a “defensive stock” in the aftermath of the War in Ukraine and the Fed’s rate hikes. Similarly, I cautioned that it was also priced for a level of growth that seems difficult to achieve, given its saturation of the auto market and challenges it might face in penetrating other markets with new insurance products.

The price has increased 24% since then, amid good news for FY 2023 and Q1 2024. Yet, I will maintain my outlook that the current price doesn’t offer an attractive discount and that challenges to growth remain. For the long-term investor, this warrants a better margin of safety before buying.

Recent Results

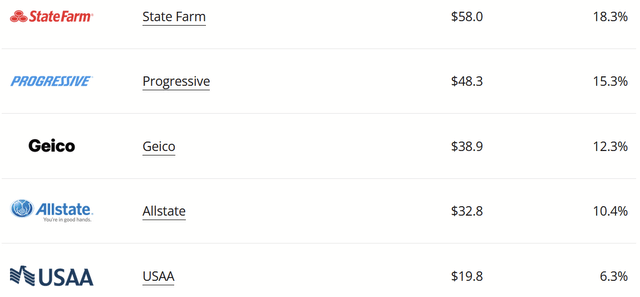

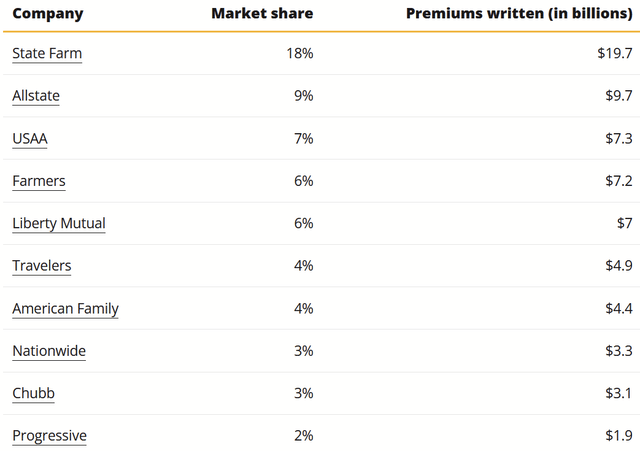

To start, things have been going well for Progressive. Perhaps the most important change occurred in the traditional Auto product. ValuePenguin indicates that their market share has grown.

ValuePenguin

FY 2023 results showed that their auto premiums written jumped from $38.9 billion to $48.3. I mentioned last time that the Top 10 auto-insurers had about 77% of the US market, and the amount remains the same, indicating the Progressive has successfully peeled off business (along with StateFarm) to raise its share for 14.4% to 15.3%.

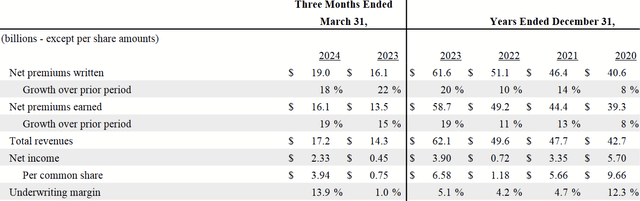

Q1 2024 Quarterly Report

In hard numbers, the table above shows how solidly business has done. Targeting an underwriting margin of 4% (combined ratio of 96%), the company has managed to do this, even in turbulent years such as 2022, allowing to continue to pursue growth.

Q1 2024 Quarterly Report

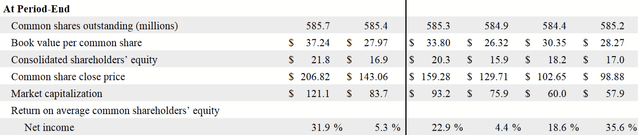

Consequently, PGR has enjoyed good, long-term growth of both tangible book value per share and earnings per share. For the end of Q1, TBV per share stood at $37.24, while TTM diluted EPS was $9.77.

Q1 2024 Form 10Q

In fact, TBV per share grew in large part because net income was mostly used to grow PGR’s portfolio of fixed income securities, enjoying high yields.

Capital Allocation (Q1 2024 Form 10Q)

Dividends and buybacks remained light, hardly a priority for the company at this moment in time (and given my feelings about the price, I’m glad buybacks have been scant).

Q1 2024 Quarterly Report

While some of these results were due to improved pricing, total policies grew too. This was seen not just in their bread-and-butter Personal Lines for Auto but in their budding Commercial Lines as well. The same goes for their Property line.

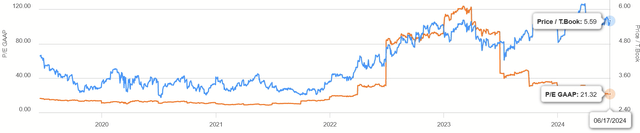

Price Ratios (Seeking Alpha)

This has also brought the P/E and P/TB to relative highs. The current P/TB of 5.59 is some of the highest it’s ever been, with so much growth in Personal Auto already behind them. P/E needs to be contextualized, as 2022’s storms created a squeeze from a surge in claims. Prior to that, the highest PGR traded was normally around 20, while often being below 10.

Future Outlook

We have to ask ourselves what exactly supports the growth assumptions baked into these valuations, whichever one might prefer (and there’s merit to both). Similarly, we have to consider the foils that might weaken this and, consequently, result in a correction or flat price movements over the long run.

Property Line

In Q1 earnings, CEO Tricia Griffith talked more about the efforts to improve the focus of their Property line, which was something I noted last time had been a drag for the company, given their exposure to costly states like Florida. She explained:

Our property profile, as we talked about, we are growing in what we would call growth states or more non-volatile states as far as weather, and we’re shrinking in the volatile state…As I laid out last year, we’re starting to see the over 100,000 homeowners policies in Florida start to non-renew that took a while because we needed to notify the customers and talk with the DOI.

So the good news is that growth is not occurring at the total expense of return on equity, which was essentially the problem from when they began pursuing Property more ambitiously. It’s good that they are learning this lesson.

ValuePenguin

It’s worth noting that Progressive’s share of U.S. homeowner’s insurance is much smaller, and so the potential for growth is higher. StateFarm is their main competitor, who leads in both Auto and Property. Yet, part of why competitors like Allstate (ALL), which I also covered, lost share is because of this extra exposure to property and how those losses tied up their capital. Progressive can aim for a market share of 9% to 18%, but this may only be possible if they risk their underwriting profitability.

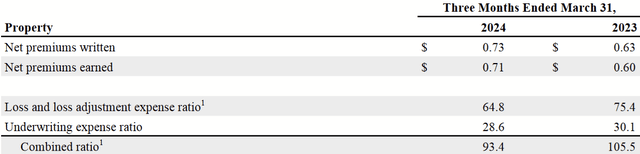

Q1 2024 Quarterly Report

While the company-wide CR was about 86%, Property was only 93.4 for Q1, and prior to that, it had been a money-loser. Growth in this area is more difficult than the Auto line, and doing so at a lower ROE than their traditional product complicates a story of earnings growth, particularly as the idea is to convert Auto customers into Property customers.

Cyclical Factors

There are two cyclical factors to consider here as well that may complicate the straight line of growth implied by the current share price. One is that insurance companies go through cycles of being squeezed by large claims and having to wait for state governments to approve rate increases. What we are seeing now is combined ratios improving as Progressive raises prices.

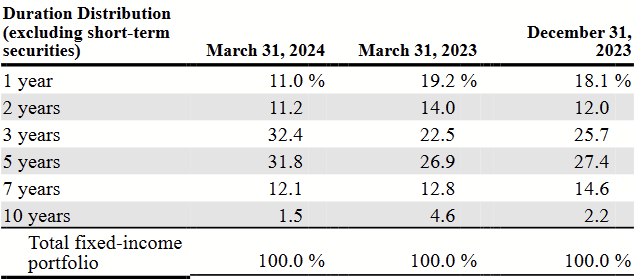

Similarly, there is an interest rate cycle, as their portfolio will yield more when interest rates go up. It’s unsurprising that nearly all of recent earnings went into fixed-income.

Fixed-Income Maturities (Q1 2024 Form 10Q)

Seen above, Progressive is locking in these higher rates, mostly for 3 – 5 years out. If rates decline, this means they won’t be reinvested with as high of interest, and that can lag some of the apparent earnings growth. Considering investment income accounted for 26.6% of net income in Q1, this isn’t just a story of growing policies.

2021 Form 10K

Seen above, investment income declined as interest rates were pushed to zero in the wake of COVID.

Both cyclical factors occurring in proximity to each other could put a dent in earnings and long-term returns for the shares.

Challenges for Auto Line

I did address one aspect of this in my previous thesis, which I’ll reiterate:

Lastly, I believe the number of drivers who need insurance is unlikely to rise by any major degree. There are already 240m licensed drivers in the U.S. With the millennials all grown up now and declining birth rates for years, there’s not a large, new cohort of drivers for insurers to scoop up anymore. Realistically, Auto Line’s growth will be incremental.

This is an issue because even maintaining market share has some diminishing prospects over a long period of time. One thing I did not mention before is how this can be paired with the impact of self-driving cars as well. Interestingly, Progressive is optimistic about this on its website:

In fact, the higher cost of vehicles with driver assistance features may result in more expensive insurance due to the potential for greater loss. Technologically advanced vehicles require specialists to make repairs, which means the standard automotive repair shop may not be able to service your car.

I think what they are saying is true today, but I don’t think it’s necessarily true in the future. As these vehicles become the standard, the shortage for specialists likely works itself out. Moreover, even if we assume the product doesn’t become cheaper, automation is known to reduce human error and thus accidents. As the US Department of Transportation explains:

Vehicle safety promises to be one of automation’s biggest benefits. Higher levels of automation, referred to as automated driving systems, remove the human driver from the chain of events that can lead to a crash. While these systems are not available to consumers today, the advantages of this developing technology could be far-reaching.

As accidents go down, insurance risk goes down. This reduces the risk to insurers. This is good for Progressive in one sense.

This might also force them to compete on prices because now Allstate or GEICO can offer lower rates for safer policies. If Progressive ultimately has to write smaller premiums, that hurts their growth. It will require them to earn a larger margin, as keeping a CR of 96% on a smaller premium would reduce earnings.

Automation is also something that occurs on a spectrum of partial to full, so it doesn’t require an immediate leap for this to occur or to be realized in pricing wars and financial results. Rather, it could gradually wear things down.

Valuation

Whether one wants to use P/TB or P/E is perhaps not too important because both multiples are quite high in this case. I’ll talk about both.

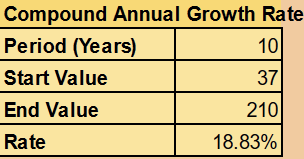

Author’s calculation

TBV would need to grow by 18.83% each year to match the current share price. Yet, over the past decade (starting from about 9% auto market share) the CAGR of TBV was 12%. It’s possible for PGR to achieve a streak of high returns on equity to grow the book, but that’s not what their strategy is right now.

If we look at earnings and let the PEG-ratio be our guide, we can ask if 20% average growth is possible to justify a P/E around that level. That’s suggesting earnings in the range of $30B to $40B after a decade. I think it’s a bit much, given the potential headwinds I discussed before and the astonishing volume of sales such growth would require. Slower growth (the kind if any setbacks occur) makes a $122B market cap seem more like a fair value, not a discount.

Conclusion

Recent results show why Progressive is as successful as it has been. Yet, the current price assumes a very bright future and long-term results without hiccup. While possible, the current price doesn’t offer a margin of safety, which is crucial for a long-term investment.

The business is fine and not in trouble. I think investors looking for safety simply need to wait for a safe price. Until then, it’s just a Hold for me.

Read the full article here