Investment Overview – ProKidney Shows Promise, Then Stock Price Tanks

ProKidney (NASDAQ:PROK) went public last week following a business combination with the Special Purpose Acquisition Company (“SPAC”) Social Capital Suvretta Holdings Corp. III. As a reminder, a SPAC is a company that achieves a listing solely in order to invest in / merge with a private company, helping that company list in a “light touch” regulatory fashion. SPACs trade at a value of $10 per share, and have two years to find a suitable company to merge with, or face delisting.

ProKidney operates in an intriguing space. According to its Q1 2024 quarterly report / 10Q submission:

Our lead product candidate, rilparencel (which we sometimes refer to as REACT), is designed to preserve kidney function in a Chronic Kidney Disease (“CKD”) patient’s diseased kidneys.

Rilparencel is a product that includes autologous Selected Renal Cells (“SRC”) prepared from a patient’s own (autologous) kidney cells. SRC are formulated into a product for reinjection into the patient’s kidney using a minimally invasive outpatient procedure that might be repeatable, if necessary.

Because rilparencel is a personalized treatment composed of cells prepared from a patient’s own kidney, there is no need for treatment with immunosuppressive therapies that are required during a patient’s lifetime when a patient receives a kidney transplant from another, allogeneic donor.

This type of approach is more broadly known as “cell therapy”, and it has proven successful in the field of oncology, where Bristol Myers Squibb’s (BMY) Abecma and Breyanzi, Gilead Sciences (GILD) Tecartus and Yescarta, Legend Biotech’s (LEGN) Carvykti, and Iovance Biotherapeutics’ (IOVA) Amtagvi have all secured FDA approval, the first five to treat hematological cancers, and the latter in melanoma.

More recently, several biotechs – e.g. Cartesian Therapeutics (RNAC) and Cabaletta Bio (CABA) have begun investigating whether a cell therapy may effectively treat autoimmune diseases, such as myasthenia gravis or systemic lupus erythematosus (“SLE”), while ProKidney itself is pioneering the use of cell therapy in kidney disease.

In fact, because cells are harvested from patients using a routine kidney biopsy, rilparencel is able to circumvent the painful and prolonged preconditioning regimes patients must undergo in order to have their cells extracted for other types of cell therapy, suggesting there may be an exciting opportunity in play to challenge current standards of care in CKD.

Initially, the newly merged company’s share price performed reasonably well, reaching a high of $13 per share just over one year post-merger. Around that time, management reported that it had closed on the purchase of a 210,000 square foot facility and approximately 22 acres of land in Greensboro, North Carolina, that would provide the necessary manufacturing for its product, and revealed a cash position of $446m.

Then, the share price began to nosedive – sinking to a low of $1.2 by mid-November last year, a loss of 90% in a little over three months, as the main sponsor of the SPAC that helped list ProKidney – Chamath Palihapitiya – began selling stock in the company.

It seems the investor sold off in the region of 2.5m shares during that period, for prices as low as <$3. The market took note, and ProKidney’s hopes of delivering a first cell therapy directed against kidney disease began to look forlorn.

Stunning Share Price Recovery In 2024

Meanwhile, ProKidney, after appointing a new CEO in November last year, promoting executive vice president for clinical development and commercialization Bruce Culleton to succeed Tim Bertram, who transitioned into an advisory role, continued to trial its lead program, with some success.

Announcing 2023 earnings and business updates in March this year, the company reminded investors it had:

Reported positive interim Phase 2 RMCL-002 study data in November, demonstrating the potential of rilparencel to preserve kidney function in moderate and high-risk patients with CKD caused by type 2 diabetes.

Updated data include information from 83 patients enrolled in the RMCL-002 study and demonstrated a safety profile in line with previous rilparencel Phase 1 & 2 trials, and similar to that of a kidney biopsy.

the updated RMCL-002 data showed preservation of kidney function in several patient groups with advanced CKD caused by type 2 diabetes. Patients with Stage 4 CKD with severe albuminuria– broadly viewed to have the highest risk of kidney failure and where there remains a significant unmet clinical need– showed the most potential benefit.

When announcing Q1 2024 earnings earlier this month, the company revealed that:

Final results from RMCL-002 Phase 2 trial to be presented in the Late Breaking Clinical Trials session at the European Renal Association (ERA) Congress on May 25, 2024.

Incidentally, ProKidney also reported a net loss for the quarter of $(25.8m) – down from $(27.2m) in the prior year period – and a cash plus marketable securities position of ~$329m – sufficient to last until the fourth quarter of 2025, management believes.

Last November, based on the data gained from its Phase 2 study, management opted to make a protocol amendment to its potentially pivotal Phase 3 study, in order to “focus on patients with higher risk of kidney failure”. Specifically, the company reported:

In the PROACT 1 Phase 3 clinical study, the eGFR enrollment range will be modified from the current range of ≥ 20 to ≤ 50 ml/min/1.73m2to a new range of ≥ 20 to ≤ 35 ml/min/1.73m2. The Company believes that focusing on patients with more severe CKD will better align with RMCL-002 results and feedback from payers and providers. The Company continues to expect PROACT 1 will resume enrollment, and PROACT 2 will commence enrollment, in mid-2024.

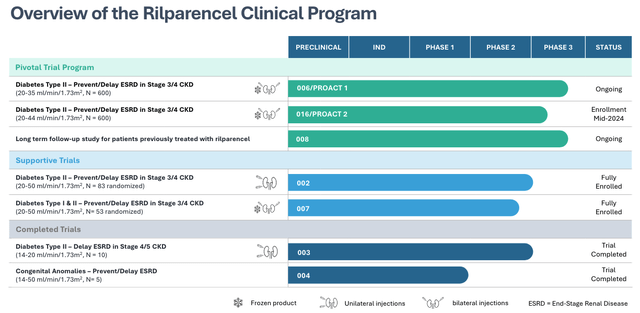

The study has been paused while the FDA considers whether to accept the amendment, however the fact that ProKidney’s share price has risen in value from >$1.45 in late April, to >$3.5 at the time of writing – a gain of nearly 150% – seems to suggest the market is once again being won over by ProKidney’s work in the clinic. Below I share a full list of studies past, present, and future, as per the company’s latest investor presentation.

ProKidney clinical studies overview (investor presentation)

Current Market/Competitive Overview

The reasons for the heavy insider selling have never truly surfaced, but there are some reasons why anyone considering buying into ProKidney’s recent bull run ought to exercise caution.

One important development involves a drug the market is wildly excited about, albeit not in the field of CKD – at least not yet. Novo Nordisk’s (NVO) GLP-1 agonist drug semaglutide – marketed and sold as Ozempic as a therapy for Type 2 diabetes, and as Wegovy to treat weight loss, is being hailed as a drug of major significance thanks to its miraculous weight loss qualities, and pegged for >$50bn of annual sales in the not-too distant future.

The once-weekly self-injectable drug is now beginning to show it may have “best-in-class” therapeutic qualities in other disease areas, including cardiovascular, and significantly for ProKidney, CKD as well. In March, Novo Nordisk reported updated data from its FLOW clinical study, which enrolled >3,500 patients with type 2 diabetes (“T2D”) and CKD. The company stated:

The trial achieved its primary endpoint by demonstrating a statistically significant and superior reduction in kidney disease progression as well as cardiovascular and kidney death of 24% for people treated with semaglutide 1.0 mg compared to placebo.

The combined primary endpoint included five components measuring the progression of CKD and the risk of kidney and cardiovascular mortality.

Both CKD and cardiovascular components of the primary endpoint contributed to the risk reduction. Further, superiority of semaglutide 1 mg vs placebo was confirmed for the confirmatory secondary endpoints.

The reality is that a once-weekly auto-injector is substantially more convenient, and cost-effective, than an autologous cell therapy like REACT.

This may explain why insiders have been selling ProKidney stock, but on a more positive note, it may explain why ProKidney is changing its pivotal study protocols to patients with more severe forms of the disease – such patients may have diseases that are too advanced to be successfully treated with a GLP-1 agonist drug like semaglutide.

GLP-1 agonists are not the only drug type, ProKidney needs to be concerned with – according to the company’s 2023 10K submission:

We believe that our principal competitors include developers of SGLT2 inhibitors, including canagliflozin (marketed as Invokana by companies including Janssen Pharmaceuticals, Inc.), dapagliflozin (marketed under the brand names Farxiga® and Forxiga® by companies including AstraZeneca plc (AZN) and Bristol-Myers Squibb Company (BMY), and empagliflozin (marketed as Jardiance® by companies including Boehringer Ingelheim and Eli Lilly and Company (LLY)), and MRAs, which are small-molecule therapies recently approved to lower risks of CKD progression, notably finerenone (marketed as Kerendia® by companies including Bayer AG).

It has to be said that this is a formidable list of competitors – on its own, a compelling reason not to invest in a company like ProKidney which is almost entirely reliant on a single pipeline product, with funding set to run out in less than two years.

Nevertheless, if ProKidney can prove that its unique approach carries a higher benefit to patients than any other therapy, then it may well be approvable, and the CKD market comprises some 35m patients, of whom ~135k progress to dialysis every year, which is an expensive procedure, not to mention an unpleasant experience for any patient.

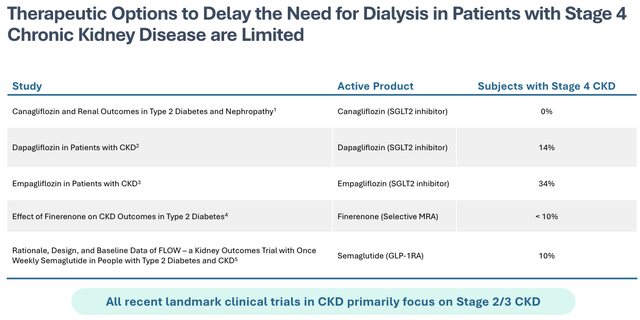

Therapeutic options for later stage patients limited (investor presentation)

As we can see above, ProKidney management points out that the likes of Invokana (Canagliflozin) and Farxiga (Dapagliflozin) have tended to focus more on patients with less advanced stages of CKD in studies, so it is still possible that Rilparencel could prove itself to be the right option for T2D / CKD patients with stage 4 or later disease. Even in that smaller subset of patients, the market opportunity would likely be more than sufficient to support a “blockbuster” (>$1bn revenues per annum) revenue opportunity.

Concluding Thoughts – Rearranging the Deckchairs, Or A Meaningful Opportunity? We’ll Know More on May 25th When Updated Phase 2 Data Is Shared

Insider selling is considered a major red flag within the biotech industry, even if there are many reasons why a billionaire investors may pull money out of one investment and pump it into another that the general public is not privy to.

Changing study protocols is arguably another red flag, that suggests management is searching – possibly in vain – for a niche where its drug performs better than others.

The rise of GLP-1 agonist drugs has been extraordinary, but there is at least an argument to suggest this drug class works better in early-stage disease, while current standards of care are inadequate in later stage CKD.

As such, we can argue that the investment case for ProKidney is finely poised. Shares continue to trade at a massive discount to former highs, even after the recent run-up, and in a couple of days, new data may add ballast to the “Stage 4 and beyond” case for a standard of care of treatment in the making.

There is no question that cell therapy can treat diseases extremely effectively, and that we may well see more and more cell therapies directed against kidney disease going forward.

Despite these potential plus points, I would personally stop short of giving ProKidney a “buy” recommendation. Kidney Disease is a complex and hard to treat indication, and multiple biotechs have tried and failed to successfully develop drugs for this indication.

The lack of support from insiders should not necessarily be a reason for a retail investor to sell, but the Phase three studies will take a long time to complete, so even if there is a boost when the updated Phase two data is announced this week or next, there may well be opportunities further down the line to buy in at around the price ProKindey stock trades at today, in my view, as biotech stock prices drift downward in the absence of data catalysts.

For all of the reasons discussed above, I am remaining on the sidelines when it comes to ProKindey – I can see both sides of the argument for and against the new study protocols and the risk of being eclipsed by GLP-1 agonists and SGLT2 inhibitors, and the bull thesis is not sufficiently compelling for me at this time.

Read the full article here