Article Thesis

Prologis, Inc. (NYSE:PLD) is a leading logistics real estate investment trust that is currently trading with one of the highest dividend yields in recent memory. While the valuation is not especially low, the company deserves a premium valuation thanks to its strong track record and convincing longer-term outlook. With interest rates likely declining in the coming quarters and years, Prologis could be an attractive income investment right here.

Company Overview

Prologis, Inc. is a real estate investment trust focused on logistics properties, such as warehouses, distribution facilities, and fulfillment centers. Demand for these properties is, not surprisingly, tied to the ongoing rise of e-commerce — Prologis thus has been able to show highly appealing growth in the past and should be able to deliver compelling business growth in the future, too.

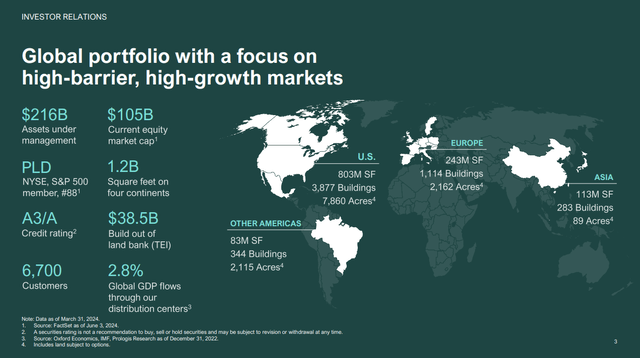

Prologis focuses on markets with above-average entry barriers and above-average growth rates, thus one could say that Prologis has somewhat of a “premium” focus. The company’s biggest market is the US, but Prologis is active in Europe, South America, and Asia on top of that. Its international operations include properties with a square footage of around 430 million, meaning the US business, with properties of slightly more than 800 million square feet, is roughly twice as large as the non-US business. The following slide shows how exactly the company’s properties are distributed around the world:

Prologis’ asset footprint (Prologis presentation)

Prologis serves close to 7,000 different customers, meaning its business is well-diversified. Of course, some of these customers are more important than others, but the biggest customers, such as Amazon (AMZN), Home Depot (HD), FedEx (FDX), or DHL (OTCPK:DHLGY) are huge corporations with strong profits and healthy balance sheets, thus the counterparty risk is pretty low. With more than $200 billion in assets under management, Prologis is among the largest REITs in the world, which also holds true when we look at market capitalization — PLD is valued at $108 billion at the time of writing.

The Macro Picture

Prologis, Inc. should benefit from several macro trends in the future.

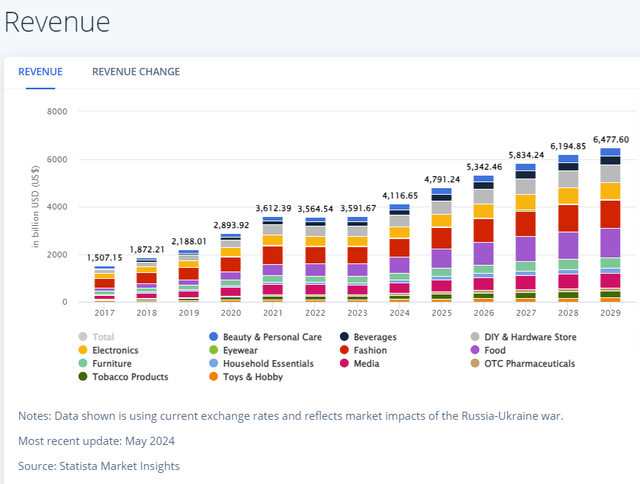

First, logistics properties are oftentimes used for e-commerce, thus growing e-commerce sales are good for Prologis and its peers in the logistics REIT industry. According to statista.com, e-commerce sales are forecasted to hit a new record high this year, while growth in the coming five years is expected to be healthy as well, at almost 10% annually, as we can see in the following chart:

E-commerce sales (statista.com)

Higher e-commerce sales for companies such as Amazon will result in more products being sold to customers, all else equal, which should result in increasing demand for storage room for all of these products. While Amazon and its peers are not growing at the ultra-high relative growth rates from their early days any longer, it can be expected that Amazon and co. will continue to grow at a nice pace, and logistics real estate providers such as Prologis should be able to benefit from that. E-commerce sales should also benefit from improving consumer sentiment in the long run. Right now, consumer sentiment is rather weak, due, in part, to a still-high inflation rate. But in the long run, consumer sentiment should improve, which should result in more discretionary consumer good purchases — e-commerce companies will be among the beneficiaries of this, and so will logistics REITs such as Prologis.

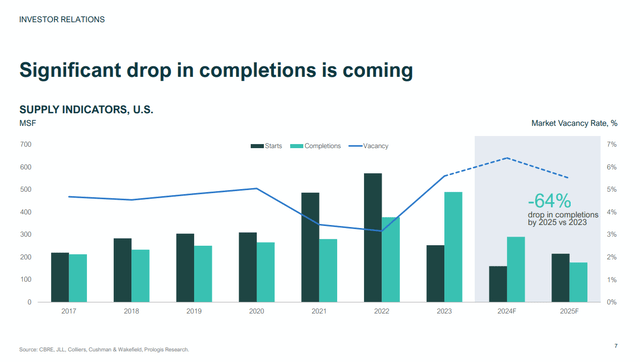

Second, Prologis should benefit from lower new completions of logistics properties in the future. During the pandemic, when e-commerce sales boomed, demand for logistics properties grew nicely. This resulted in a boom when it came to building new properties, which has, in turn, resulted in a lot of supply coming to the market. This was negative for the rent growth Prologis and its peers experienced. But due to the fact that interest rates have risen substantially and since the market became a little oversupplied, new logistics properties starts have declined substantially, which should result in lower completions in the foreseeable future:

Completions are declining (Prologis presentation)

Completions hit a record high in 2023 due to a high number of starts in the previous two years, but the number of completions will drop significantly this year, with another decline being expected for 2025. This should result in a firming leasing market, as supply-demand dynamics move in the favor of logistics real estate players such as Prologis. An improving rent growth rate in the second half of this year and in 2025 would thus not be surprising, I believe.

Prologis Has Solid Growth Prospects

Prologis has delivered strong business growth in the past, and its future growth outlook is good as well. The company should be able to drive funds from operations growth via several contributing factors, including same-property rent growth, the organic buildout of new assets, and M&A.

While rent growth has not been overly strong in the very recent past due to the aforementioned overbuilding of logistics properties, the lower completions in the coming years should help improve same-property rent growth.

Prologis has a deep pipeline of future growth investments, with management stating that the pipeline for logistics properties alone is around $39 billion, or around 20% of the company’s current assets under management. Prologis also plans to invest in data centers, including via conversions of existing properties.

Due to the rise of AI, data centers are a huge growth market and will likely remain so in the foreseeable future. This will result in higher electricity demand, but also in higher demand for data center properties. Prologis plans to benefit from this trend by converting its most suitable properties into data centers, having identified more than 150 conversion candidates so far. Management plans to invest $2.75 billion in these conversions over the coming five years, with Prologis also having the option to build out new data centers from scratch — another $4.75 billion will be invested that way over the coming five years, according to the most recent investor presentation.

Between these business growth drivers and some potential margin tailwinds from improving scale (company-wide costs are distributed over a larger revenue and gross profit number), Prologis is forecasted to grow its FFO per share by double-digits over the coming three years: The analyst consensus estimate for PLD’s FFO per share growth stands at 12%, 11%, and 12%, respectively, in 2025, 2026, and 2027. While there is no guarantee that the company will hit these estimates, PLD’s track record versus analyst estimates is pretty strong — over the last 20 quarters, there was not a single FFO miss, as the company beat estimates 15 times while hitting the estimate 5 times. If history is a guide, there is thus a very solid chance that Prologis will be able to grow at least in line with what analysts are forecasting right now. But even if growth was slower, let’s say at 70% of what is expected, i.e. 8% per year, that would be very solid, considering Prologis also offers a nice dividend yield of 3.4% at current prices. Between a dividend yield of well above 3% and a high-single-digit FFO per share growth rate, total returns could easily come in at 10%+ per year in the foreseeable future — and that would be weak compared to current analyst estimates.

Is Prologis An Attractive Investment?

The share prices of many REITs have suffered from interest rates rising substantially over the last couple of years. But while the Fed has not started to lower interest rates so far, recent comments by Jerome Powell indicate that the Fed could lower rates soon. The CMEWatch tool indicates that there is a 97% chance of at least one rate cut by the end of the year, thus investors likely won’t have too long until interest rates are declining again. This should help Prologis in refinancing its future maturities (mostly in 2026 and beyond) at more favorable rates, while declining interest rates could also attract more investors to income stocks such as Prologis, especially if the company continues to deliver dividend increases regularly.

Today, Prologis trades at 21x forward funds from operations. While that is not an ultra-low valuation, it does not look excessively high, either. Prologis is a quality REIT with a strong balance sheet, a great track record, compelling growth opportunities, and an excellent market position — paying 21x FFO for such a REIT does not seem outlandish at all to me.

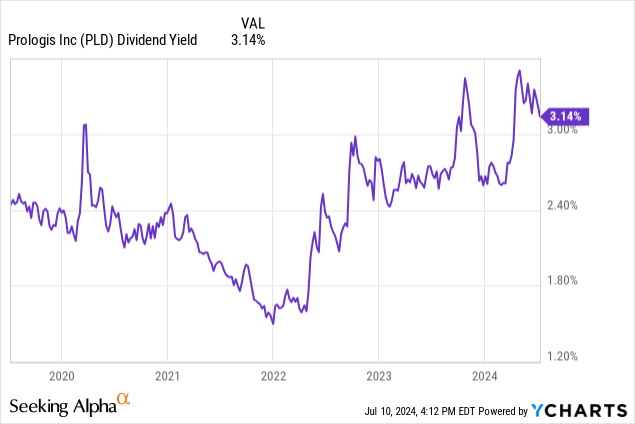

Shares are down 4% over the last year and currently trade close to 20% below the 52-week high. To me, it looks like right now is a rather good time to enter or expand a position, especially when we consider that Prologis’ dividend yield has seldomly been this high:

Prologis mostly traded with a dividend yield of less than 3% over the last five years, sometimes even with a yield of less than 2%. Today, with a trailing yield of 3.1% and a forward yield of 3.4%, Prologis looks quite attractive in comparison, making me give this quality REIT a “Buy” rating.

Read the full article here