Prospect Capital Corporation (NASDAQ:PSEC) is a well-managed business development company that had no issues whatsoever in the last year to cover its dividend with net investment income.

As a matter of fact, Prospect Capital presently has a better dividend pay-out ratio than some of its larger and more appreciated BDC cousins.

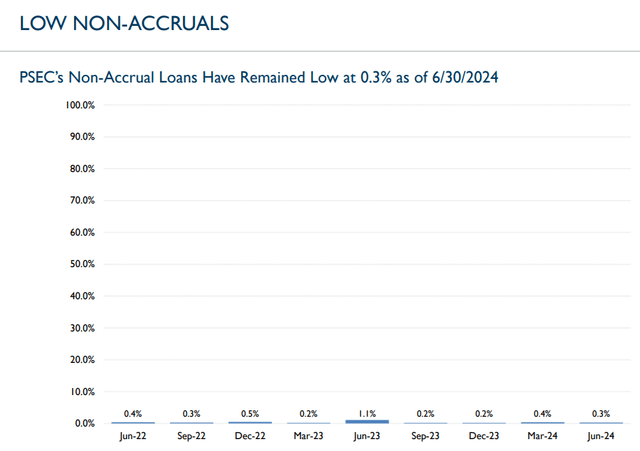

Prospect Capital’s credit profile also improved QoQ as the non-accrual ratio dropped to a low 0.3%, suggesting impressive loan quality for the business development company.

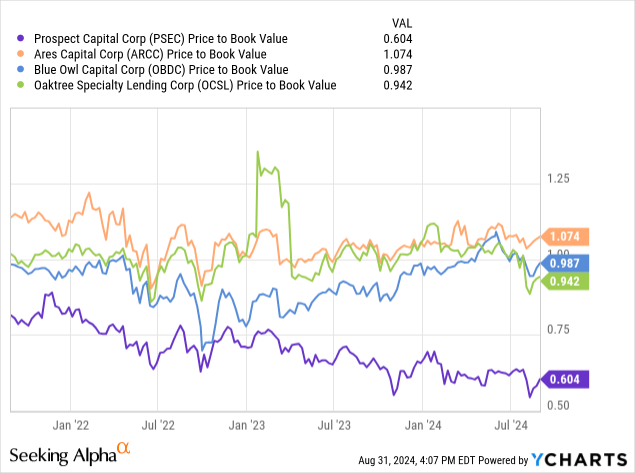

I don’t think the big discount to net asset value is justified when taking into account Prospect Capital’s robust financial condition and performance. The 14% dividend yield is sustainable, in my view.

My Rating History

My last stock classification for Prospect Capital was Buy as a higher-for-longer rate environment benefited Prospect Capital and the business development company had strong credit quality.

Prospect Capital’s loan quality further increased in 4Q24 and the dividend was even better covered with net investment income than in the prior quarter.

Portfolio And Income Review

Prospect Capital is structured as a business development company under the Investment Company Act of 1940 and therefore must distribute 90% of its taxable income to shareholders.

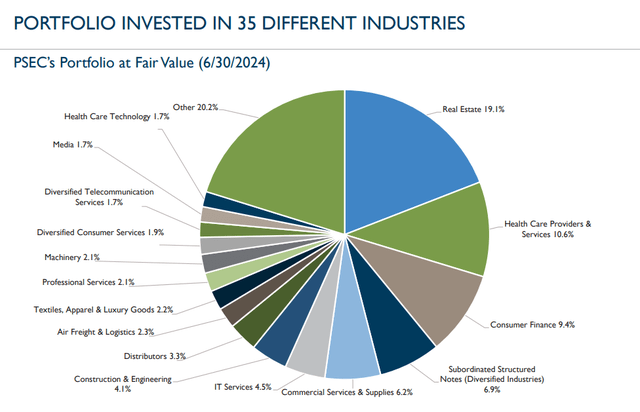

The business development company owns a large portfolio of lower middle market loans and has a considerable real estate investment exposure. Real estate accounted for about one-fifth of Prospect Capital’s investment portfolio as of June 30, 2024 which was valued at $7.7 billion.

Portfolio Investments (Prospect Capital Corporation)

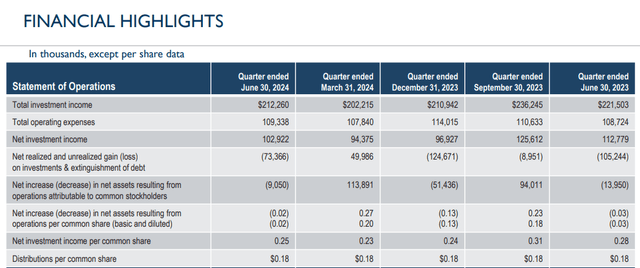

Prospect Capital’s earned $102.9 million in net investment income in the quarter ending June 30, 2024, reflecting a YoY decline of 9%. The majority of this income comes from interest income from Prospect Capital’s First and Second Lien debt and the business development company has built a floating-rate posture amounting to 82.1% of assets.

Financial Highlights (Prospect Capital Corporation)

What is going well for Prospect Capital right now is its portfolio performance. The business development company has a very low amount of non-accruals in its portfolio which translates into a substantial excess coverage for passive income investors.

Prospect Capital’s low non-accruals of 0.3% based on fair value helps separate the BDC from some of its peers, particularly companies like Oaktree Specialty Lending Corp. (OCSL) which recently suffered an increase in non-accruals, triggering concerns about the dividend.

Low Non-Accruals (Prospect Capital Corporation)

Dividend Pay-Out Ratio Is Actually Kind Of Impressive

The business development company has not the best reputation in the BDC industry because Prospect Capital occasionally under-earned its dividend with net investment income which, in some cases, led to dividend cuts.

Furthermore, Prospect Capital’s net asset value record is not the best either, with the BDC reporting a long-term decline in its NAV.

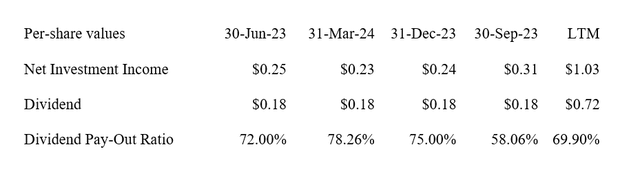

Be that as it may, Prospect Capital’s dividend pay-out and credit quality look great at the present time. Prospect Capital earned $0.25 per share in net investment income in the last quarter which equates to a dividend pay-out ratio of 72%.

The dividend pay-out ratio for Prospect Capital in the last 12 months was even better: The BDC paid out only about 70% of its total net investment income.

Most BDCs that I have reviewed lately, including industry heavyweights such as Ares Capital Corp. (ARCC) or Blue Owl Capital Corp. (OBDC) had higher dividend pay-out ratios. Ares Capital Corp. paid out 85% of NII whereas Blue Owl Capital paid out 73% of its net investment income.

Dividend (Author Created Table Using BDC Information)

Excessive NAV Discount

Prospect Capital’s stock is selling for a 40% discount to net asset value which seems to be a bit exaggerated when taking into account that the credit profile (non-accruals) is healthy and that the business development company did not have any problems covering its dividend pay-out.

Prospect Capital’s net asset value amounted to $8.74 per share as of June 30, 2024 (my implied intrinsic value estimate), reflecting a decline of $0.25 per share, predominantly because of net realized and unrealized losses.

It seems to me that a 40% discount to net asset value is quite a bit exaggerated given that the BDC’s most important KPIs are actually looking quite good, and, in some cases, are even better than those of BDCs that have a higher perceived investment quality, such as Ares Capital Corp.

Why The Investment Thesis Might Disappoint

The central bank is poised to lower short-term interest rates next month which points to a weaker lever for net investment income growth, particularly for those BDCs that are heavily concentrated in floating-rate BDCs.

Prospect Capital is not the most aggressively positioned floating-rate BDC, but the company does have considerable exposure to high interest rates.

As far as the dividend is concerned, however, I don’t see any major issues, but I would want to assert that following Prospect Capital’s dividend pay-out ratio is a must.

My Conclusion

Prospect Capital, like it or not, looks quite solid as a BDC investment right now and I suggest that the business development company’s 14% yield is relatively safe.

It is the big 40% discount to net asset value, together with the 70% LTM dividend pay-out ratio and the low amount of loans on non-accrual that make Prospect Capital’s 14% yield surprisingly competitive.

Prospect Capital’s credit quality and dividend pay-out ratio look compelling and I don’t see any major issues in the portfolio or in the BDC’s income trend that would indicate to me that the dividend is headed for the chopping block.

With such a high net asset value discount to book, I think that Prospect Capital remains an exceptionally attractive investment choice for passive income investors and I think that PSEC should be able to trade at a much lower discount to NAV moving forward.

Read the full article here