At a Glance

In light of new data from the PROTECT study, my previous caution on Travere Therapeutics (NASDAQ:TVTX) has intensified. Filspari’s mixed efficacy—significant in proteinuria reduction but inconclusive in pivotal eGFR total slope—casts doubt on its long-term clinical value. While the Mirum deal has shored up liquidity, extending the cash runway to approximately 28 months, the company’s escalating operational costs remain a point of concern. Coupled with a diminished market cap following a 40% stock plunge, these factors significantly undermine Travere’s financial footing and strategic agility. Consequently, I am revising my investment recommendation from “Hold” to “Sell.”

Earnings Report

To begin my analysis, looking at Travere’s most recent earnings report, a few key metrics stand out. Net product sales show a YoY growth of $6M, registering $57M this quarter, largely driven by Filspari’s launch. However, both R&D and SG&A expenses have also significantly increased: R&D spiked to $69.4M from $59.7M, largely due to pegtibatinase clinical trials and hiring; SG&A rose to $74M from $53M, attributable to Filspari’s market launch. The net loss widened to $85.6M this quarter from $67M YoY. What’s concerning is that despite revenue growth, higher operational expenses have nullified gains, deepening the net loss. This suggests Travere needs to exercise stricter cost management alongside its revenue-generating strategies.

Financial Health & Liquidity

Turning to Travere Therapeutics’ balance sheet, with the addition of the expected $210M upfront payment from the Mirum deal, the company’s liquid assets would surge to $701.4M. Specifically, ‘cash and cash equivalents’ would stand at $280.9M, and ‘marketable debt securities’ at $420.5M. For the six months ended June 30, the monthly cash burn rate from operating activities is approximately $25.1M. With the augmented liquidity, Travere’s estimated cash runway extends to about 27.9 months. As usual, these values and estimates rely on past data and may not forecast future performance.

In light of the impending transaction, Travere’s liquidity profile significantly improves, bolstering its financial stability. Its convertible debt of $376.4M remains significant but becomes more manageable when offset by the prospective increase in liquid assets. Given this robust liquidity status and relatively balanced debt portfolio, the company would be in an even stronger position to secure additional financing, whether debt or equity-based, effectively mitigating short-term financial risks. These are my personal observations, and other analysts might interpret the data differently.

Capital, Growth, Momentum, & Ownership

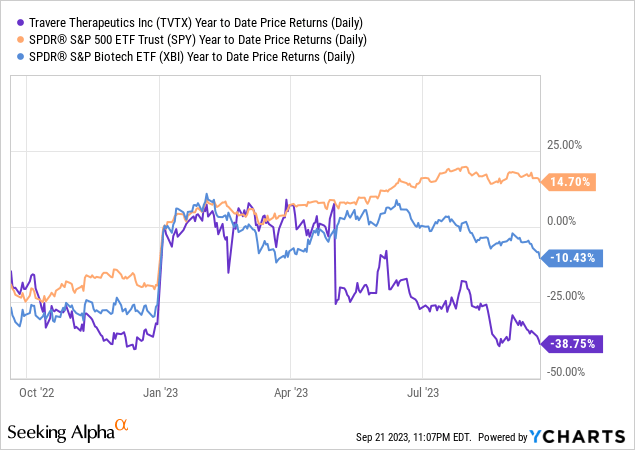

Travere Therapeutics’ recent 40% stock plunge significantly impacts its financial profile, reducing the market cap to $573.08M. This constrains leverage and capital-raising abilities. In terms of growth, revenue projections, according to Seeking Alpha data, for 2025 appear bullish, but warrant skepticism given mixed clinical data and a more constrained financial runway. The stock’s underperformance relative to SPY, especially post-plunge, further underscores the bearish sentiment.

Regarding ownership, institutional backing at 82% may lend some credibility, but their potential future actions in light of the plummet become crucial.

Navigating Filspari’s Gray Area in eGFR

The PROTECT study yielded several key data points that warrant close scrutiny. Filspari’s eGFR total slope showed a 1.0 mL/min/1.73m^2 per year improvement over irbesartan but missed statistical significance with a p-value of 0.058. This narrow miss introduces a level of clinical ambiguity that’s concerning, especially when framed within the higher cost of Filspari relative to irbesartan.

However, it’s worth noting that the eGFR chronic slope demonstrated a statistically significant 1.1 mL/min/1.73m^2 per year advantage (p=0.037) over irbesartan. Yet, given the stringent regulatory environment, especially in the U.S., whether this is enough to sway a favorable review remains a point of contention. In IgAN, a disease characterized by proteinuria and declining kidney function, eGFR serves as a pivotal long-term indicator. While proteinuria reduction is a significant short-term goal, it’s eGFR that truly informs us about long-term renal outcomes.

The trial also showed a remarkable 42.8% proteinuria reduction from baseline at week 110 for Filspari, dwarfing irbesartan’s 4.4% reduction. While this data is undoubtedly positive, it still leaves us questioning whether Filspari can convert this proteinuria improvement into long-term kidney function benefits, as indicated by eGFR.

In summary, while Filspari exhibited certain advantages over irbesartan in proteinuria and to some extent in eGFR chronic slope, the inconclusive total eGFR results introduce a gray area in Filspari’s risk-benefit profile. These mixed signals necessitate a meticulous interpretation of the data, given the significant market and regulatory implications.

My Analysis & Recommendation

In the wake of the recent events surrounding Travere Therapeutics, it’s evident that the biotech sector remains a terrain fraught with volatility and unpredictability. The PROTECT study’s ambiguous data casts a penumbra of clinical uncertainty over Filspari’s prospects. Despite achieving statistically significant improvements in the eGFR chronic slope and proteinuria reduction, the failure to meet statistical significance in the eGFR total slope, a key metric for renal function, is a clinical red flag. While the drug is unlikely to be quickly pulled from the U.S. market, these results may fail to invigorate prescribers, particularly when considering Filspari’s limited market penetration to date (as evidenced by $3.5M in revenue for its second quarter on the market).

Travere’s bolstered liquidity position, post-Mirum deal, is a silver lining but doesn’t exonerate the company from its operational expenditure woes. With a monthly cash burn rate of approximately $25.1M, even an extended cash runway of 27.9 months will evaporate if the company doesn’t reassess its fiscal strategy. It should also be emphasized that the strong liquidity position is a temporal grace; the high operational costs are an ongoing liability that could dilute future earnings, undermining long-term shareholder value.

Moreover, Travere’s valuation has contracted significantly, as evidenced by its $573.08M market cap post-plunge. This restricts the firm’s capital-raising capacity at a time when it should be investing in another clinical trial to reinforce Filspari’s competitive differentiation. If institutional investors, who currently back 82% of the company, decide to cut their losses, we could see a more accelerated decline in stock value.

In the coming weeks and months, investors should scrutinize the company’s subsequent regulatory interactions, and any strategic shifts to lower the operational expenditure. Additionally, watch for signals regarding a potential new clinical trial aimed at solidifying Filspari’s value proposition, which at the moment remains tentative at best.

Given the aforementioned risk factors and Filspari’s clouded path forward, I am downgrading my investment recommendation from “Hold” to “Sell.” The drug’s uncertain clinical profile, combined with the company’s financial fragility and shrinking valuation, makes Travere a riskier proposition than the upside potential would justify. At this juncture, I find it more prudent to disengage and reallocate capital towards more compelling opportunities in the biotech sector.

Risks to Thesis

While I stand by my “Sell” recommendation for Travere Therapeutics, several counterarguments should be considered. First, Filspari’s statistically significant improvement in eGFR chronic slope and proteinuria reduction may be enough to gain niche market acceptance, particularly in refractory cases or as a second-line therapy. Regulatory leniency for unmet medical needs could tilt the balance favorably. Second, the company’s enhanced liquidity, post-Mirum deal, is not trivial. It provides a buffer for potential debt servicing and future R&D. Third, institutional ownership at 82% could signal insider confidence rather than a selling risk; large stakeholders may double down after a drop. Lastly, the stock’s steep decline may make it a potential takeover target, offering shareholders a premium.

Read the full article here