The Company

Prudential Financial (NYSE:PRU), a $30-billion market-cap player in the financial services sector, oversees a vast portfolio of assets totaling around $1.417 trillion as of March 31, 2023 [10-Q filing]. Its operations span across key regions including the United States of America, Asia, Europe, and Latin America. Through its various subsidiaries and affiliated companies, Prudential offers an extensive range of financial solutions, encompassing life insurance, annuities, retirement options, mutual funds, and investment management. These comprehensive offerings cater to both individual and institutional clients, facilitated by one of the most expansive distribution networks in the financial services industry.

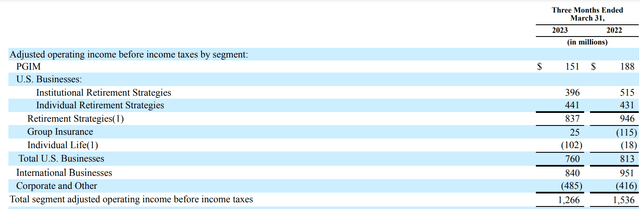

The company’s main operations can be categorized into several segments. These include PGIM, which is a global investment management business. Additionally, there are U.S. Businesses, comprising Retirement Strategies, Group Insurance, and Individual Life businesses. The International Businesses segment is also significant, bringing in over 66% of net consolidated adjusted operating income in Q1 FY23. Furthermore, there is the Closed Block division, treated as a divested business that is reported separately from the Divested and Run-off Businesses within the Corporate and Other operations.

PRU’s 10-Q

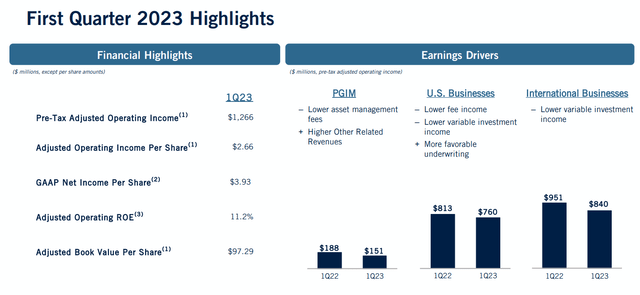

As you can see, Prudential’s Q1 2023 financial results showed a mixed performance across segments, with underlying business growth, but challenges in asset management fees, fee income, and variable investment income. The firm reported Q1 2023 pre-tax adjusted operating income of ~$1.3 billion or $2.66 per share on an after-tax basis. PRU experienced lower asset management fees in its PGIM segment, primarily due to decreased AUM caused by higher interest rates, equity market declines, and net outflows. Prudential’s U.S. Businesses saw lower fee income and less favorable variable investment income, partially offset by higher rates on spread income and improved underwriting. The International Businesses segment faced a decrease in earnings, primarily resulting from lower spread income due to less favorable variable investment income.

Prudential’s Q1 2023 IR presentation

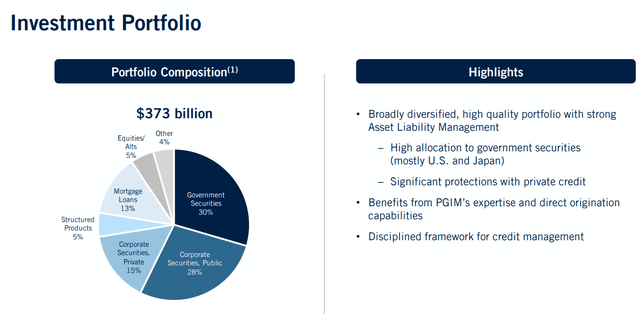

Prudential’s investment portfolio looks quite diversified, with ~30% in government securities, ~43% in investment-grade corporate securities, and nearly 40% in private placements. The company’s focus on conservative underwriting is reflected in its mortgage loans, which represent 13% of the portfolio and have an average loan-to-value ratio of 57% and debt service coverage of 2.4 times.

Prudential’s Q1 2023 IR presentation

Prudential’s PGIM experienced third-party institutional and retail net outflows of $14 billion in the quarter, driven by client redemptions for liquidity needs and investor rebalancing in response to higher interest rates and inflation.

![Prudential's Q1 2023 IR presentation [author's notes]](https://wealthbeatnews.com/wp-content/uploads/2023/06/49513514-16861112336897066.png)

Prudential’s Q1 2023 IR presentation [author’s notes]

Despite these challenges, Prudential aims to expand access to investing, insurance, and retirement security by investing in growth businesses, delivering exceptional customer experiences, and developing innovative financial solutions.

As the most recent example of that, Prudential announced the acquisition of a majority stake in Deerpath Capital Management, a leading US private credit and direct lending manager. This acquisition should enhance PGIM’s alternative capabilities, generate additional fee-based revenue, and complement its existing lending origination capabilities. Before the takeover, the PGIM segment had $237 billion in AUM across alternatives, and now it’ll add another $5 billion, bringing more expertise in lower middle market direct lending.

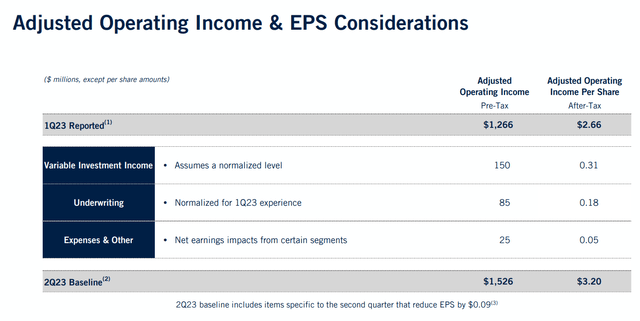

During the latest earnings call, Prudential’s CFO, Ken Tanji, mentioned that variable investment income in the first quarter was below expectations by $150 million, and underwriting experience was adjusted by $85 million to normalize for Q1 performance. Additionally, other items are expected to increase adjusted operating income by $25 million due to seasonally elevated expenses. These adjustments result in baseline EPS of $3.20 for the 2nd quarter, while excluding specific items would yield $3.29 per share, indicating an improvement in underlying earnings power driven by business growth and higher interest rates. Tanji emphasized the company’s strong capital position, with cash and liquid assets at $4.6 billion, and their balanced approach to capital deployment, prioritizing financial strength, flexibility, investment in their businesses, and shareholder distributions.

Prudential’s Q1 2023 IR presentation

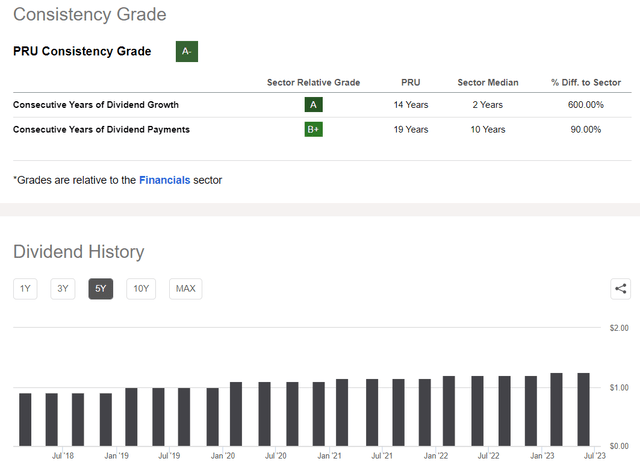

In Q1, Prudential indeed returned $700 million to shareholders and increased the quarterly dividend by 4%, marking its 15th consecutive annual dividend increase. Prudential Financial stock holds a strong “A-” in Seeking Alpha’s Dividend Consistency grade, beating the whole Financials sector by a margin:

Seeking Alpha, PRU

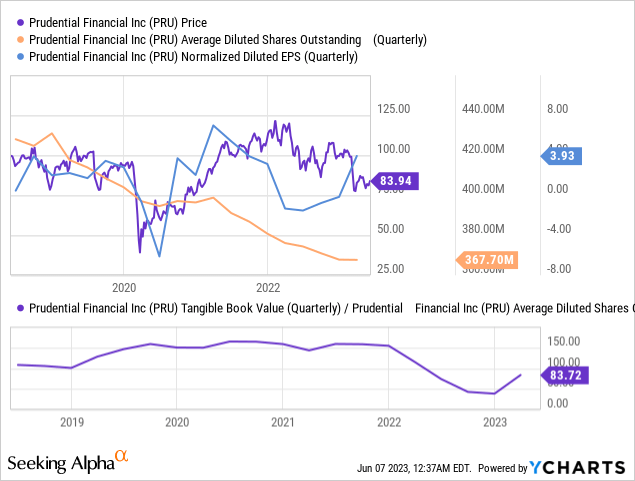

Over the past 5 years, Prudential has demonstrated a dividend growth rate of 8.23%, based on the data on hands. The projected annual dividend payout is $5.00 per share, which gives us a forwarding yield of ~6.02% amid a solid payout ratio of just 54.19%, according to Seeking Alpha. At the same time, PRU’s average number of outstanding shares fell by >14% over the past 5 years, and the tangible book value per share began to gradually recover in Q1 FY23 after falling sharply since early 2022. The EPS recovery started even earlier, from the middle of last year.

From all this, I can conclude that Prudential Financial’s business is relatively stable over the long term and has the potential for further dividend increases and buybacks, which is good for long-term shareholders seeking value.

Valuation

From financial theory, we know that a low P/E ratio likely indicates that investors are concerned about the financial health of the company, while a high P/E ratio suggests that the company is well-positioned for growth.

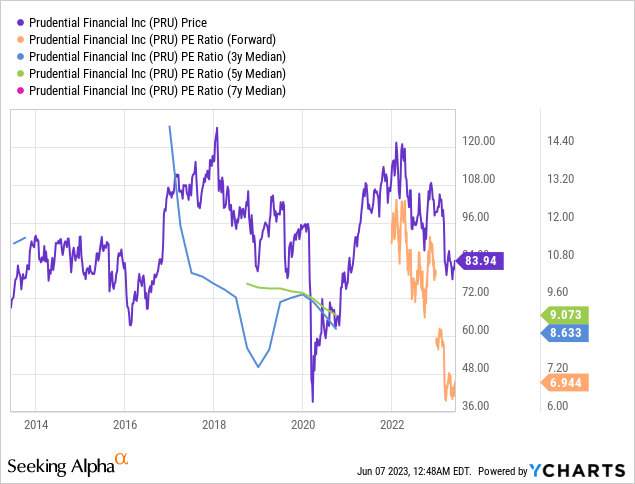

PRU’s forwarding P/E multiple is by no means high – they’re currently 20-24% below the 5- and 7-year medians, respectively:

Still, PRU cannot be said to have problems with EPS expectations. Wall Street analysts’ consensus assumes roughly the same P/E ratio for the next 5 years, which seems unrealistic to me:

![Seeking Alpha [author's notes]](https://wealthbeatnews.com/wp-content/uploads/2023/06/49513514-16861141199786017.png)

Seeking Alpha [author’s notes]

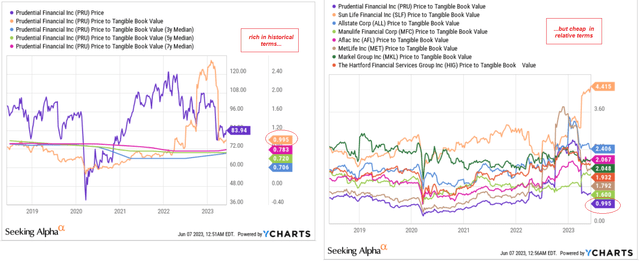

On the other hand, if we look at the P/TBV ratio, we see a slightly contradictory picture: PRU shares currently look expensive in the context of their historical perspective, but at the same time they’re the cheapest among their industry peers:

YCharts, author’s notes

Argus Research analyst Kevin Heal wrote about the same things in his research paper [May 11, 2023 – proprietary source]. He wrote that PRU appears attractively valued relative to a group of comparable life insurers based on long-term ROE and dividend yield. Argus’ revised price target of $95 implies a multiple of 8x projected EPS for FY2023, in line with the median of the peer group.

At the same time, Morningstar Premium gives PRU a generous fair value price of $105 per share:

![Morningstar Premium, PRU [author's notes]](https://wealthbeatnews.com/wp-content/uploads/2023/06/49513514-1686114632489409.png)

Morningstar Premium, PRU [author’s notes]

The Verdict

Of course, I’m puzzled by a number of risks mentioned by Seeking Alpha fellow analyst Real Investments, among others, in his recent article. First, Prudential Financial has a significant investment portfolio in CMBS that could be negatively impacted by a decline in value. A potential decline in CMBS values may reduce the company’s overall profitability and net worth and affect its ability to originate new loans and investments. It may also lead to a credit downgrade, making it more expensive for the company to borrow money. Second, high claims and an increased mortality rate continue to weigh on Prudential Financial’s profitability. Although management believes in a return to pre-pandemic mortality rates, current reports indicate that mortality rates remain high, which could impact the company’s financial performance. Third, I’m concerned that the impending recession could severely hurt PRU for the foreseeable future.

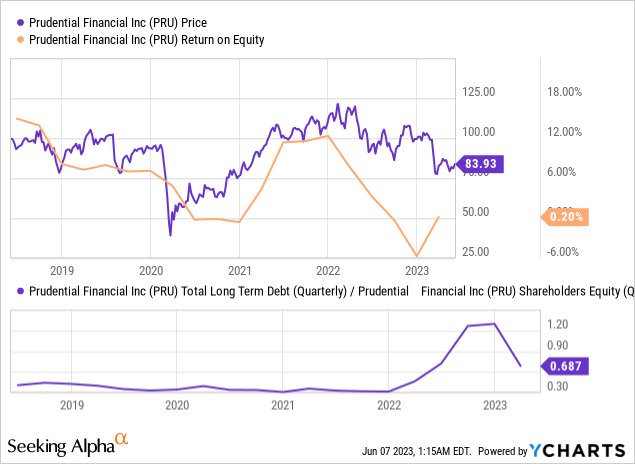

But despite these risks, I like Prudential Financial’s stock at current price levels if we take a 5-10 year investment perspective. The shareholder return is good when we have a dividend in the region of 6% and a $1 billion share repurchase program for 2023. There is also a chance that ROE will continue to recover from the recent sharp decline and that the credit risk to debt ratio will continue to decline, making PRU more attractive.

So I assign PRU stock a Buy rating with a year-end price target of $95 per share.

Thanks for reading!

Read the full article here