Recently, a reader sent me a message asking for my opinion on the PGIM Ultra Short Bond ETF (NYSEARCA:PULS) and how the fund compares against one of my recommendations, the Janus Henderson AAA CLO ETF (JAAA). Rather than give specific advice through a private message, I will use this article to summarize my thoughts on the PULS ETF so readers can make an informed decision themselves.

By itself, the PULS ETF is a top-quartile short-term bond fund primarily investing in treasuries, commercial paper, and money market instruments. However, compared to the JAAA, I believe the JAAA has higher credit quality, higher historical performance, and a higher distribution yield. The one caveat against the JAAA is that its portfolio is highly credit-sensitive, so it may suffer mark-to-market losses during periods of market turmoil.

Overall, I prefer the absolute safety of treasury bill funds or the higher returns of CLO funds. I rate the PULS ETF a hold.

Fund Overview

The PGIM Ultra Short Bond ETF seeks to deliver total returns through a combination of current income and capital appreciation. The PULS ETF primarily invests in a portfolio of investment grade, U.S. dollar-denominated short-term fixed and variable rate debt instruments including U.S. Government securities, agency securities, commercial paper, money market instruments, collateralized loan obligations, and other short-term corporate debt securities.

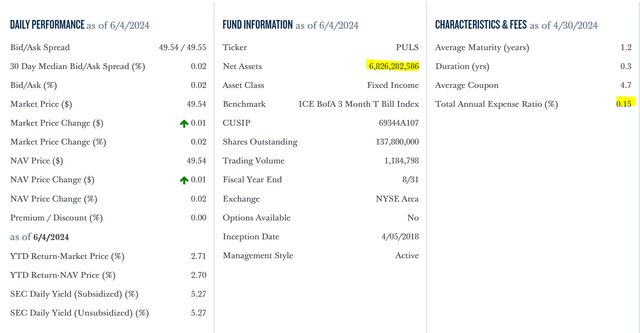

The PULS ETF is a sizeable fund, with $6.8 billion in assets while charging a 0.15% expense ratio (Figure 1).

Figure 1 – PULS overview (pgim.com)

Portfolio Holdings

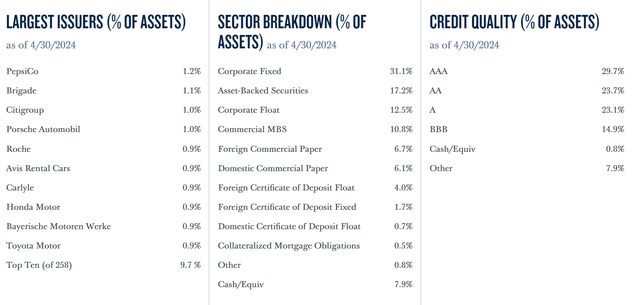

Figure 2 shows the portfolio allocations of the PULS ETF. The largest sector weights in the PULS ETF are Corporate fixed-rate securities at 31.1% of the portfolio, Asset-Backed securities at 17.2%, Corporate floating-rate securities at 12.5%, Commercial MBS at 10.8% and Commercial Paper of foreign companies at 6.7%.

Figure 2 – PULS portfolio allocations (pgim.com)

PULS’ portfolio is predominantly investment-grade rated, with 29.7% AAA-rated, 23.7% AA-rated, 23.1% A-rated, and 14.9% BBB-rated.

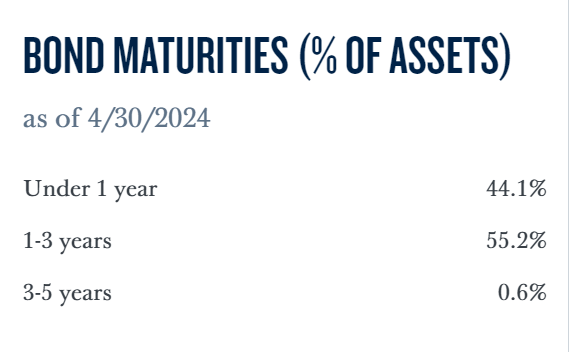

In terms of maturities, 44% of the portfolio matures within a year and 55% matures within 1-3 years (Figure 3). This gives the portfolio an overall duration of 0.3 years.

Figure 3 – PULS portfolio duration (pgim.com)

Portfolio Returns

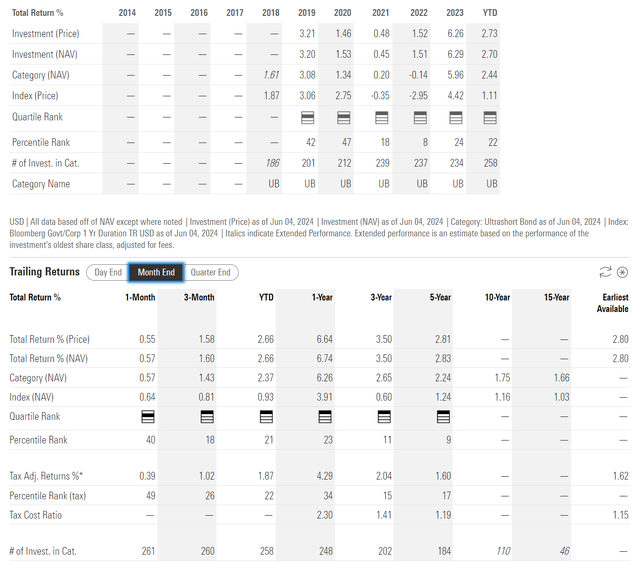

The PULS ETF has performed well against its peers, the Ultrashort Bond category on Morningstar. The PULS ETF is rated top quartile on most timeframes and has returned 6.7%/3.5%/2.8% on a 1/3/5-yr basis to May 31, 2024 (Figure 4).

Figure 4 – PULS historical returns (morningstar.com)

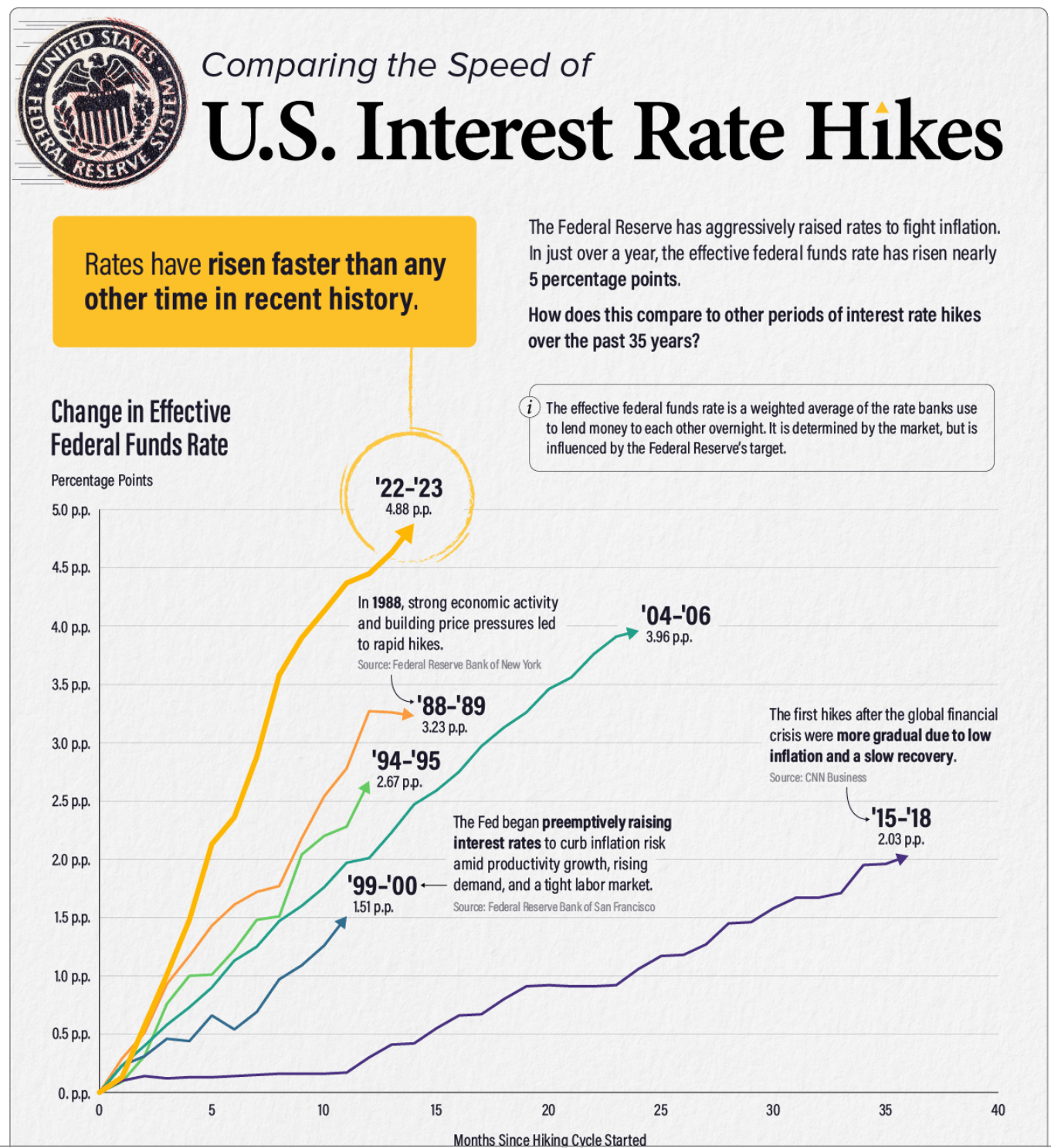

I believe PULS’ strong relative performance is because of PULS’ short 0.3-year portfolio duration and the Fed’s interest rate hiking cycle. In the past few years, we have seen the Federal Reserve raise interest rates rapidly to fight inflation, taking the Fed Funds effective rate to over 5% (Figure 5).

Figure 5 – Fed has raised interest rates at the fastest pace in history (visualcapitalist)

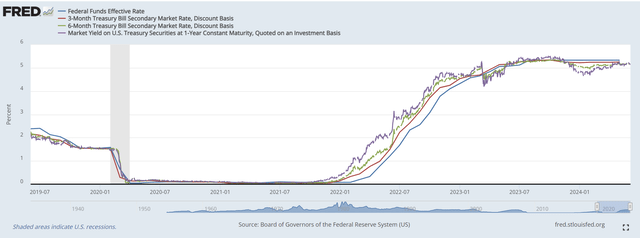

This has the effect of dragging up interest rates at other tenors from 3 months to 2 years (Figure 6). Funds with any significant duration exposure would have underperformed as short-term interest rates re-priced higher.

Figure 6 – Fed policy dragged up short-term interest rates at all tenors (St. Louis Fed)

Implication Of A Fed On Hold

However, with the Fed having stopped raising interest rates since mid-2023, the question going forward is whether PULS’ portfolio will continue to outperform its peers?

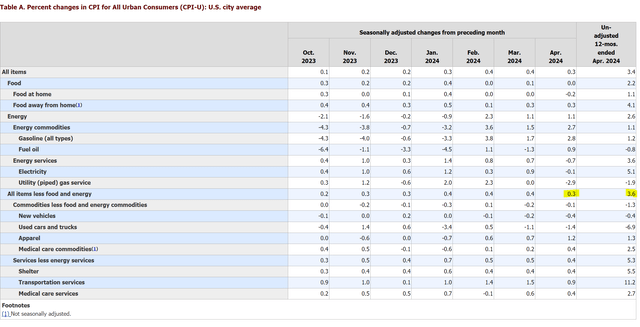

In my opinion, the Fed is effectively ‘on hold’ as it tries to wait out the current resurgence of inflation that we have seen since the beginning of 2024. April’s 3.6% YoY increase in core CPI inflation is still far above the Fed’s mandate of 2% inflation, but may not be high enough to force the Fed’s hand (Figure 7).

Figure 7 – CPI inflation still too high (BLS)

I believe the hurdle rate to the Fed restarting policy rate increases is very high. This is because for the Fed to restart rate hikes now, they will have to admit they made a policy mistake in November when they ‘pivoted’ to an easier monetary stance.

Instead, it is far easier for the Fed to remain on hold indefinitely until either inflation slows down enough to give the Fed sufficient ‘confidence’ to cut policy rates, or inflation reaccelerates above 5% and forces the Fed’s hand to resume rate hikes.

The current stalemate should allow PULS and other low-duration funds to earn high current yields, as short-term interest rates remain elevated. However, with Fed monetary policy on hold, I believe further outperformance for the PULS ETF going forward will have to come from security selection and not duration management.

PULS vs. JAAA

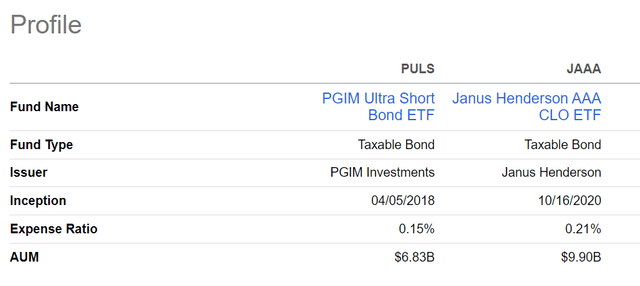

Returning to the main point of this article, comparing PULS to JAAA, let us remind readers about the JAAA ETF and compare the two funds (Figure 8). The JAAA ETF charges a 0.21% expense ratio, slightly more expensive than PULS.

Figure 8 – PULS vs. JAAA structure (Seeking Alpha)

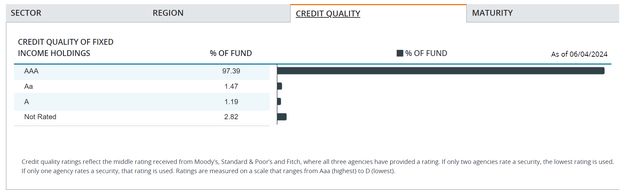

The JAAA ETF primarily invests in AAA-rated CLO debt tranches (Figure 9). In terms of credit quality, 97% of JAAA’s portfolio is AAA-rated, so in theory, its investments should have a lower probability of default than PULS.

Figure 9 – JAAA portfolio allocation by credit quality (janushenderson.com)

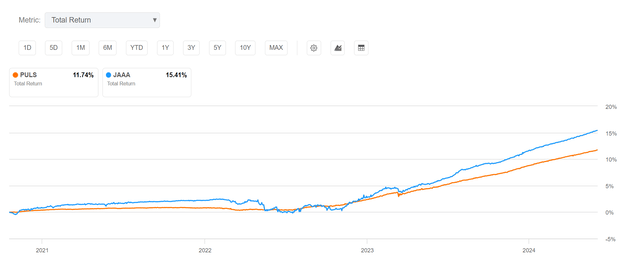

With respect to performance, JAAA has delivered higher total returns since inception of 15.4% compared to 11.7% for the PULS ETF (Figure 10).

Figure 10 – JAAA vs. PULS historical returns (Seeking Alpha)

However, the caveat is that PULS’ returns appear to be ‘smoother’. Isolating the returns in 2022, PULS outperformed JAAA in 2022, returning 1.5% compared to 0.5% (Figure 11).

Figure 11 – JAAA vs. PULS, 2022 returns (Seeking Alpha)

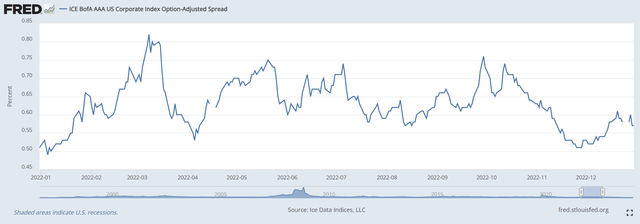

JAAA’s poor 2022 performance appears to be inversely correlated to AAA credit spreads (Figure 12). As spreads widened, JAAA’s market price declined. This makes intuitive sense, as JAAA’s portfolio holdings are synthetically created AAA-rated securities that should decline in price when credit spreads widen.

Figure 12 – AAA credit spreads in 2022 (St. Louis Fed)

PULS, in contrast, has a higher proportion of government securities and money market securities that are not as affected by credit spreads.

In a hypothetical recession scenario, I believe JAAA will experience higher price volatility, since credit spreads tend to widen during recessions, which will negatively impact JAAA to a greater extent.

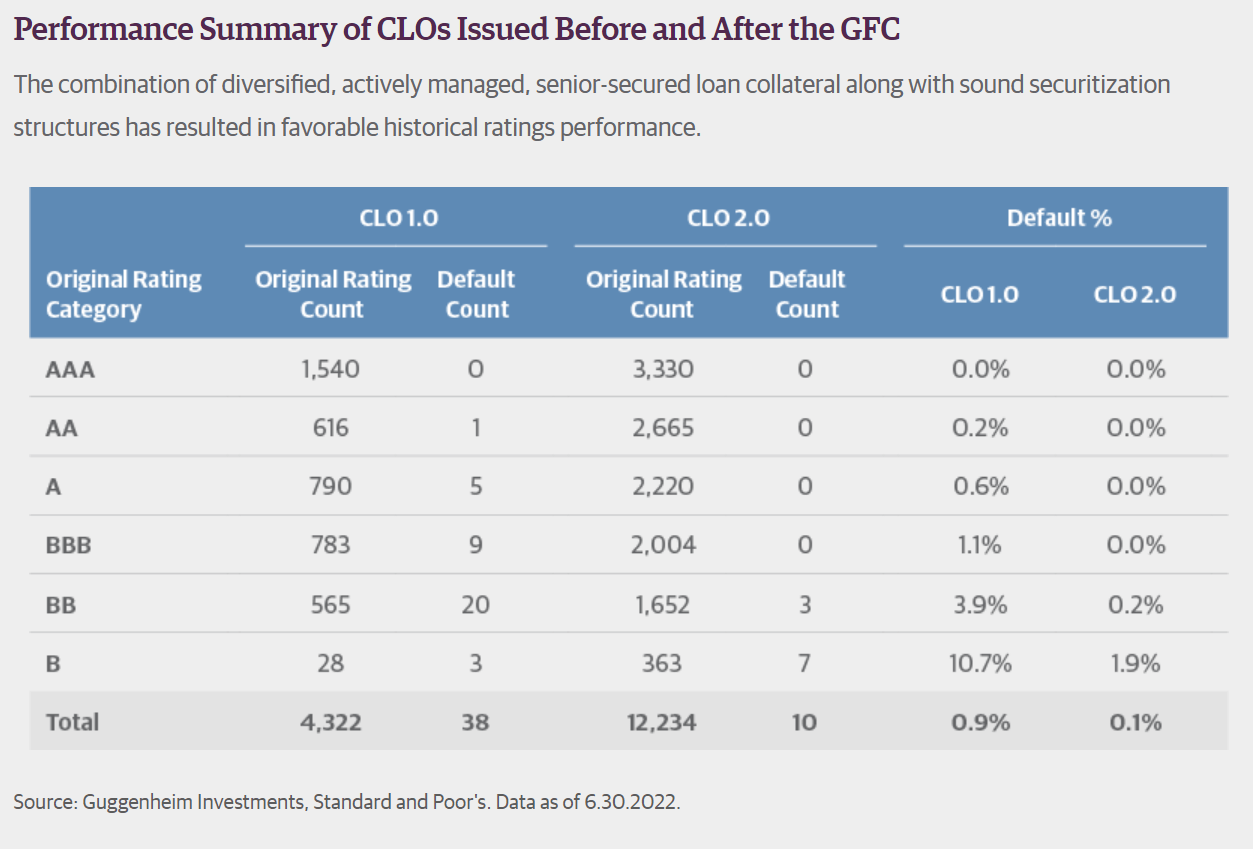

However, it is important to mention that historically, CLO debt tranches have had very strong credit performance, with only 38 out of over 4,000 rated CLO 1.0 tranches having defaulted (Figure 13). So JAAA’s ultimate credit experience should be strong.

Figure 13 – CLOs have very few lifetime defaults (S&P via Guggenheim Investments)

Finally, in terms of distribution yield, the JAAA pays a trailing 6.4% distribution yield compared to PULS at 5.7% (Figure 14).

Figure 14 – PULS vs. JAAA distribution yield (Seeking Alpha)

Overall, PULS and JAAA are both high-quality, short-duration ETFs. JAAA has a higher credit quality, with a greater proportion of its portfolio AAA-rated. Historically, JAAA has delivered stronger returns and JAAA currently pays a higher distribution yield.

However, due to the nature of its investments, the JAAA ETF may experience higher price volatility during periods of market turmoil, as its portfolio may fluctuate with credit spreads.

I last wrote about the JAAA ETF here.

Conclusion

By itself, the PGIM Ultra Short Bond ETF is a top-performing short-term bond fund, with top quartile performance against peers.

Comparing PULS against JAAA, the JAAA ETF has historically delivered stronger performance with higher credit quality and pays a higher distribution yield. The downside to the JAAA ETF is that during periods of market volatility, its portfolio will experience greater fluctuations as its investments are all credit sensitive.

While the PULS is a fine short-term bond fund by itself, I personally prefer the absolute safety of treasury bill funds like the iShares 0-3 Month Treasury Bond ETF (SGOV) or the higher returns from the JAAA ETF. I rate PULS a hold.

Read the full article here