Thesis

The PIMCO Multisector Bond Active Exchange-Traded Fund (NYSEARCA:PYLD) is a fixed-income exchange traded fund. The vehicle is a new addition to the ETF world, having come to market only recently in June 2023. With the advent of higher rates, we have seen the large, well known fixed income asset managers bring new funds to the market, in a well-timed move. We have covered the JPMorgan Income ETF (JPIE) here, which is a very similar fund.

This trend is positive, and the timing is good. While nobody can time the market to a ‘T’, when looking back 2 years from now one will certainly be able to say that 2023 was the year of the bond. A picture is worth a thousand words, so let us put that into context:

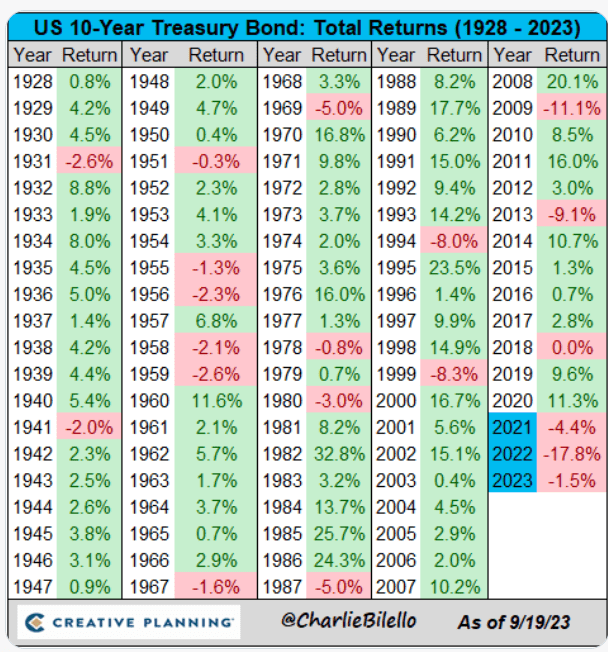

10-year Yields (Creative Planning)

The 10-Year Treasury bond is down 1.5% this year, on pace for its third consecutive annual decline. With data going back to 1928, that’s never happened before. A savvy investor will recognize a contrarian signal here, with 2024 set for positive figures.

PYLD is an active bond fund, and it seeks to maximize yield and long term capital appreciation. In essence, a retail investor is buying into PIMCO’s market views and allocations in the fixed income world, without any structural leverage. The management team for this fund is composed of well-known individuals from the fixed income CEF space: Daniel J. Ivascyn, Alfred T. Murata, and Amit Arora.

Holdings Composition – A True Multi-Sector Fund

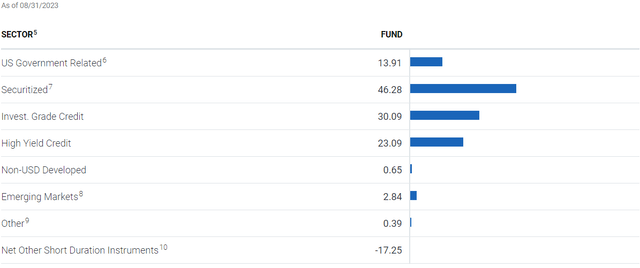

As its name indicates, the fund is a multi-sector one, containing allocations to several asset classes:

Sectoral Allocation (Fund Website)

The highest allocation is to the ‘Securitized’ asset class, one that denotes a mix of securitizations. By far the largest holdings here are collateralized mortgage obligations (CMOs) which make up over 22% of the fund.

Let us take a closer look at one of these bonds so we better understand the risk exposures taken by the fund. One of the largest holdings in the CMO space is the ‘JP MORGAN MORTGAGE TRUST JPMMT 2023 DSC1 A1 144A’ security. This is a new 2023 issuance from JP Morgan:

KBRA assigns preliminary ratings to 24 classes of mortgage pass-through certificates (6 base and 18 exchangeable classes) from J.P. Morgan Mortgage Trust 2023-DSC1 (JPMMT 2023-DSC1), the Sponsor’s second investor cash flow non-prime RMBS transaction, collateralized by investment property loans that were underwritten using debt service coverage ratios (DSCRs). The underlying pool comprises 1,247 loans with an aggregate principal balance of $306.2 million as of the March 1, 2023 cut-off date.

The JPMMT 2023-DSC1 pool is composed primarily of 30-year fixed rate mortgages (98.6% of the pool), the loans exhibit a weighted average (WA) original credit score of 753, a WA original loan-to-value (LTV) of 69.6% and a WA original combined LTV (CLTV) of 69.6%. The WA original DSCR is approximately 1.4x coverage. All the loans were originated for business purpose and are exempt from the Ability-to-Repay (ATR) and TILA-RESPA Integrated Disclosure (TRID) rules.

So the securitization is a pooling of 30-year fixed rate mortgages with a loan-to-value of roughly 69.6% and a borrower FICO of 753. The tranche has an investment grade rating and will be mainly driven by rates and the prepayment speeds present in the collateral pool.

The second-largest exposure in the fund is to corporate investment grade credit, a bucket also largely driven by rates.

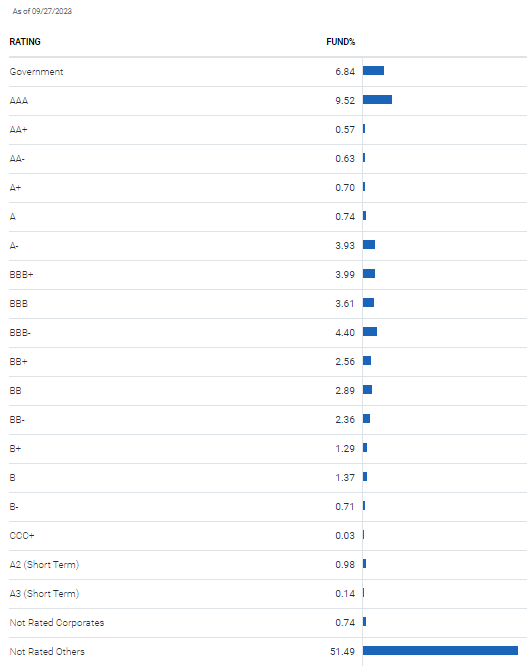

From a ratings perspective, we can again observe the multi-asset / multi-rating profile here:

Ratings (Fund Website)

Mostly the high yield exposures are below investment grade, while the large ‘Not Rated Others’ includes many securitizations. The lack of a public rating does not denote a below investment grade security, it purely talks about the fact that the issuer has not paid the rating agency for a public one, thus none is available. Unfortunately, the collateral tape does not identify the rating of each security, so we are unable to zone-in the exact names which fall in the ‘Not Rated Others’ bucket.

The fund’s main risk is interest rate risk to the 5-year point in the yield curve:

Duration (Fund Website)

We can see the fund having an effective duration of 5.09 years, and a ‘Bear Market Duration’ of 5.54 years. It is interesting to note the definition of this metric provided by PIMCO:

Bear Market Duration: A portfolio’s effective duration after a 50 bps rise in rates. The extent to which a portfolio’s bear market duration exceeds its duration is a gauge of extension risk.

The presence of many CMOs with various convexity levels translates into the bear/bull market duration analytic metrics.

Rates are the main risk factor for this fund

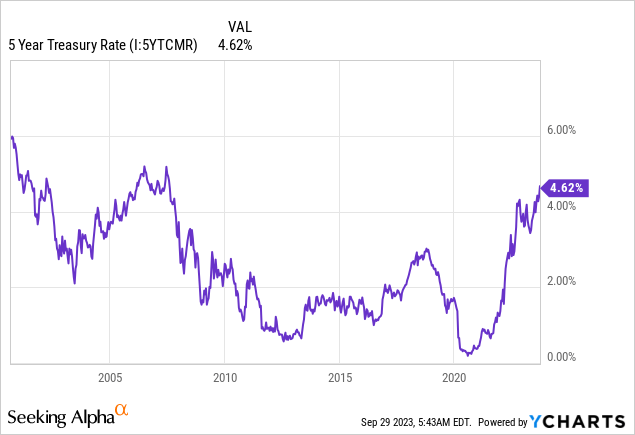

Although the ETF has a 23% allocation to high yield credits, rates are the main risk driver for the fund’s returns. As per its duration profile, the name is mainly driven by the 5-year tenor point in the yield curve:

5-year yields have risen above 4.6%, levels not seen since 2007! While it is entirely possible that this tenor point in the yield curve can go up to 5%, that move would entail only a -2% price drawdown in the fund. Nobody can time the market, but we are fairly certain we are seeing peak rates as we speak.

With the fund’s carry at 5.35%, the potential drawdown can be easily managed via the fund’s dividend. While the fund’s 30-day SEC yield is only 5.35%, its portfolio yield is in excess of 7.2%:

Yields (Fund Website)

Today is a great time to buy into mortgages and fixed rate investments. We have not seen intermediate yields as high as today in almost 20 years, and while nobody can predict the future, a dollar cost averaging strategy here can pay huge dividends down the line for a retail investor.

Conclusion

PYLD is a new fixed income ETF from PIMCO. The fund was just launched in June, and it aims to take advantage of the higher rates environment via a multi-asset portfolio. The vehicle contains a large allocation to collateralized mortgage obligations, which compose over 22% of the fund.

The vehicle is overweight CMOs and securitizations, with investment grade corporates as the second-largest sectoral allocation at 30%. High yield credits represent only 23% of the fund. The main risk factor for this ETF is represented by rates, and specifically by the 5-year tenor point in the yield curve. A move up from the current level of 4.6% to 5%, would generate only a -2% drawdown in the fund’s price.

We like buying mortgages here with rates at 20-year highs, and we like the theme of higher rates this fund is trying to capture via its active management. While nobody can time the market, history is telling us we are witnessing peak rates in 2023, and a retail investor would do well to start dollar cost averaging into good, robust funds. We are of the opinion that PIMCO is a premier, fixed income allocation platform, and dollar cost averaging into PYLD with a 24-month holding period can generate annualized returns in excess of 7% with a minimal standard deviation for the holding period.

Read the full article here