The WisdomTree U.S. Quality Growth ETF (NYSEARCA:QGRW) is one of a handful of ETFs following growth strategies, but with a twist: the index adopted by this ETF uses a quality factor that measures companies’ profitability. As a result, this index and, as a consequence, this ETF turn out to have a tilt towards profitable growth stocks.

Although this ETF is relatively new, its performance has been quite good, exceeding the Russell 1000 and S&P 500 indexes and other growth ETFs, underscored by its overweight stance in mega-cap stocks and the technology sector, which have led the market rally.

That said, despite stretched valuations at this moment, I see a constructive outlook for stocks in general, in particular for the technology sector, with a healthy economy and expectations for rate cuts starting in 2024. Against this background, I believe that QGRW is an interesting opportunity to get exposure to higher-growth companies, as it also aims to balance growth and profitability.

Fund Description & Highlights

QGRW is an exchange-traded fund that seeks to track the WisdomTree U.S. Quality Growth Index. This index is designed to select 100 U.S. companies among the top 500 U.S. companies by market cap, best ranked on a composite score combining growth and quality metrics.

The index’s growth metrics include a sentiment measure, the median analyst earnings growth forecast, and two commonly used growth indicators: the trailing 5-year EBITDA growth and the trailing 5-year sales growth. Meanwhile, on the quality side, the index adopted the trailing 3-year average of two efficiency indicators: return on equity and return on assets.

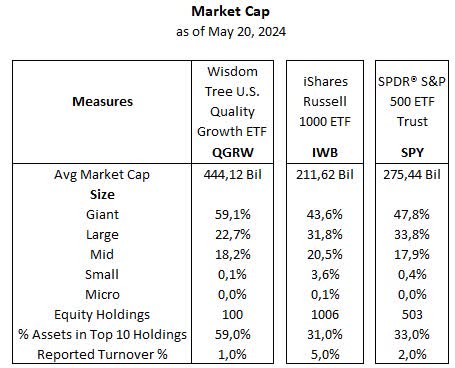

As a result of this stock selection methodology, the index ends up being quite concentrated, with the top 10 holdings accounting for nearly 59% of total assets, as of May 20, 2024. These holdings include big techs that are also among the S&P 500’s top 10 holdings, such as Microsoft, Apple, NVIDIA, Alphabet, Meta, Amazon, Broadcom, and still three names not included in the S&P 500’s top 10 companies, Tesla, Visa, and Mastercard.

In fact, QGRW has a relatively more concentrated portfolio compared to the Russell 1000 index, the benchmark for the larger capitalization universe of U.S. equities, represented here by the iShares Russell 1000 ETF (IWB), and also relative to the S&P 500, represented by the SPDR S&P 500 ETF Trust (SPY). For both the Russell 1000 and S&P 500, the top 10 holdings account for only 31% and 33% of total assets, respectively, nearly half of QGRW’s allocation. In addition, QGRW has a larger proportion of so-called giant names and an average market cap of roughly $444 B, much higher than the Russell 1000 or S&P 500.

Morningstar, consolidated by the author

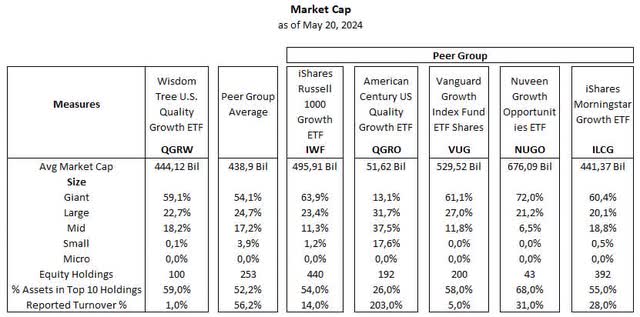

Below, we can also compare QGRW with other ETFs that have growth-oriented portfolios. Interestingly, most ETFs in the peer group have a larger allocation to so-called giant companies, such as Microsoft, NVIDIA, Amazon, Alphabet, Apple, and Meta, with the top 10 holdings representing more than 50% of total assets on average.

Morningstar, consolidated by the author

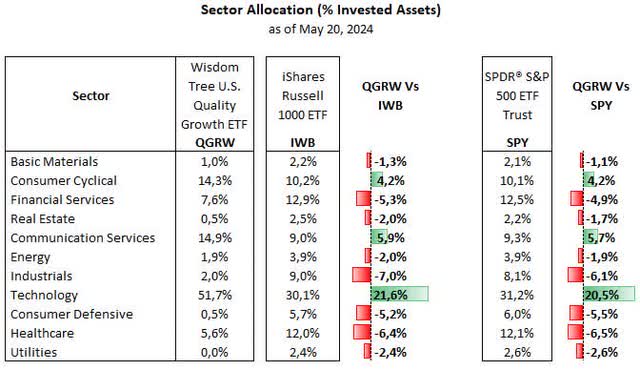

From a sector allocation perspective, QGRW’s largest allocation by far is to the technology sector, with 51.7% of total equities, followed by communication with 14.9%, consumer cyclical with 14.3%, financials 7.6%, health care 5.6%, industrials 2.0%, energy 1.9%, basic materials 1.0%, real estate and consumer defensive with 0.5% each.

Relative to the Russell 1000, QGRW is overweight in technology (+21.6%), communication services (+5.9%), and consumer cyclical (+4.2%), given QGRW’s large allocation to mega caps stocks that belong to these three sectors. On the flip side, it turns out to be underweight in industrials (-7.0%), healthcare (-6.4%), financials (-5.3%), and consumer defensive (-5.2%).

Morningstar, consolidated by the author

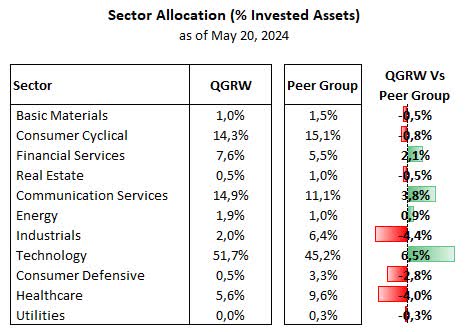

Compared to the peer group of growth-oriented ETFs, QGRW is overweight in technology (+6.5%) and communications services (+3.8%) but underweight mostly in industrials (-4.4%) and healthcare (-4.0%). This indicates how concentrated QGRW’s allocation is, even compared to other growth ETFs.

Morningstar, consolidated by the author

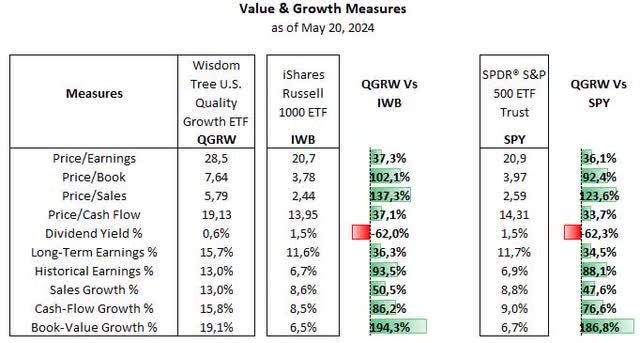

As expected, QGRW shows considerably higher valuations compared to the benchmarks, as its price-to-earnings ratio of 28.5x is much higher than 20.7x and 20.9x of the Russell 1000 and the S&P 500, respectively. Meanwhile, consistent with the growth profile of QGRW’s holdings, its growth metrics, such as earnings and sales growth, are substantially higher than those of the Russell 1000 and the S&P 500 as well.

Morningstar, consolidated by the author

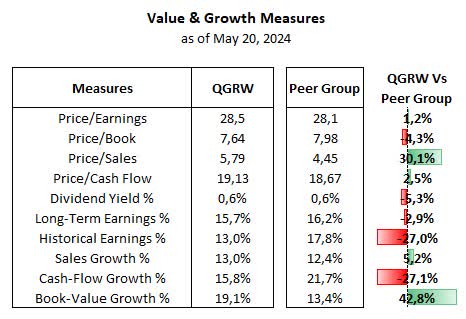

On the other hand, QGRW and the peer group share similar valuations, except for QGRW’s higher price-to-sales ratio. Meanwhile, growth metrics are mixed to some degree, with QGRW showing lower historical earnings growth and lower long-term growth expectations, while still logging higher sales growth. This higher sales growth seems to justify its higher price-to-sales multiple.

Morningstar, consolidated by the author

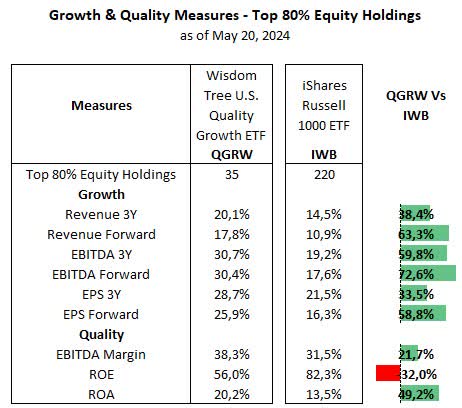

As a complement to the previous analysis, the following figure helps illustrate the impact of quality metrics used for stock selection by the WisdomTree U.S. Quality Growth Index relative to the Russell 1000.

Wisdom Tree, iShares, and Seeking Alpha, consolidated by the author

Using the top 80% stock holdings of both indexes, we can see that QGRW’s holdings exhibit much higher historical and forward revenue, EBITDA, and EPS growth compared to those of the Russell 1000, confirming QGRW’s growth-oriented portfolio. Additionally, quality indicators used by QGRW’s parent WisdomTree index (ROE and ROA) led to a relative improvement of QGRW’s average EBITDA margin to 38.3% versus 31.5% for the Russell 1000.

Stock selection played an important role in this case, as QGRW’s top 80% holdings represented just 34% of the Russell 1000, with QGRW’s concentrated portfolio averaging much higher margins on top of its higher growth profile.

Delivering Strong Total Return Since Inception

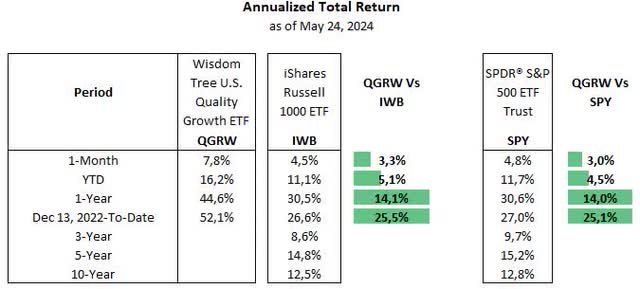

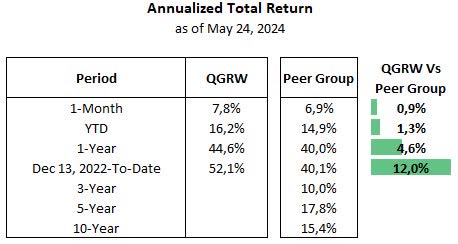

While QGRW is a relatively new fund, as its inception occurred less than two years ago on December 13, 2022, its performance has been quite promising so far, outpacing the Russell 1000 and the S&P 500 by a large margin.

Morningstar, consolidated by the author

QGRW has also outperformed its peer group since inception, though by a smaller margin, as the peer group has also surpassed the Russell 1000 and the S&P 500. These strong results were driven in large part by their overweight allocation to mega-cap stocks, which climbed even more than 70% over the period, with the exception of Apple and Tesla.

While Visa and Mastercard, the other two top 10 holdings, returned nearly 30% over the period, we can see that other relevant holdings within the top 20 holdings surged above 80% during the same stretch, such as Advanced Micro Devices, Qualcomm, Applied Materials, ServiceNow, Lam Research, all technology names. Holdings from different sectors, such as Blackstone, Intuitive Surgical, rose 67% and 51%, respectively, also outperformed the benchmarks.

Overall, although mega-cap stocks have driven QGRW’s performance to date, it is fair to say that its allocation to other tech names and even other plays outside the technology sector have all contributed to its strong performance.

Morningstar, consolidated by the author

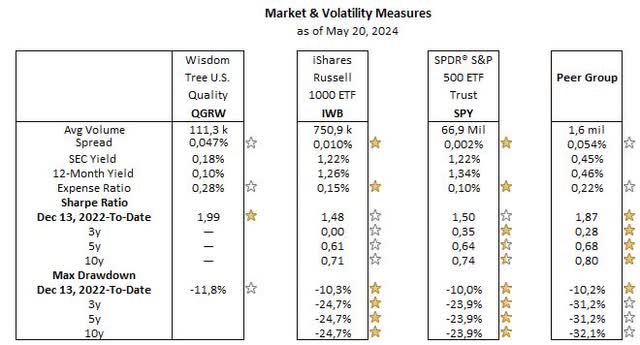

Looking at the risk-adjusted returns, QGRW’s outperformance is confirmed by its higher Sharpe ratio compared to the Russel 1000, the S&P 500, and the peer group of growth ETFs. However, it is interesting to see that the peer group of growth ETFs has also demonstrated better Sharpe ratios over longer periods (3, 5, and 10-year). Still, we should note that the Russell 1000 and S&P 500’s drawdown at roughly 24% are considerably lower than the peer group at 31-32%, which suggests a higher volatility of these growth-oriented ETFs.

Morningstar, consolidated by the author

In summary, the WisdomTree U.S. Quality Growth Index’s approach adopted by QGRW has worked quite well, driven by its overweight allocation to mega caps and other major players, mostly in the technology sector, which have seen strong price appreciation.

Looking ahead, whether mega caps can continue to outperform is uncertain, a potential stock market rotation to more value names may be a reasonable concern for investors, especially if stock market leadership starts to broaden somehow, including smaller capitalization companies that have lagged the market lately.

On the flip side, the start of a new interest rate easing cycle expected in the back half of the year is certainly a welcoming environment for growth stocks since lower rates can increase the present value of future earnings, which is an important aspect of how growth stocks are typically valued.

That said, despite worries over current high valuations, I still view it as the best course of action for investors to maintain a portion of their portfolios positioned in growth stocks, notably mega caps and the technology sector, as these can continue to generate higher earnings growth over time. With that in mind, QGRW is an alternative for investors looking for growth but still want a portfolio skewed toward quality, as evidenced by its above-average EBITDA margin.

Read the full article here