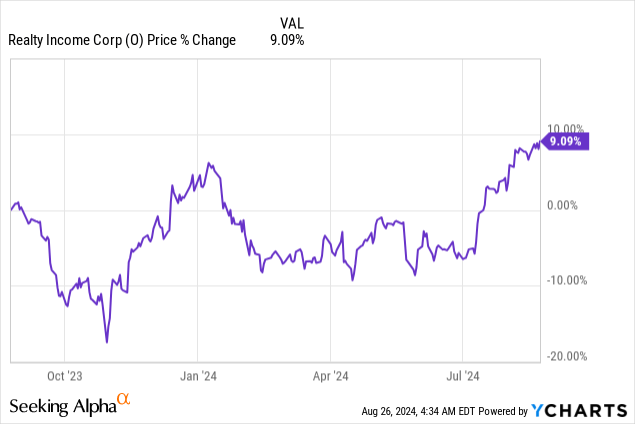

Shares of Realty Income (NYSE:O) started to surge in July and have now crossed above $60 for the first time since July 2024. Realty Income delivered robust second fiscal quarter earnings at the beginning of the month that showed strong AFFO and same-store rental growth results, especially in the industrial portion of the REIT’s business. The Federal Reserve also appears to be on the cusp of finally lowering the federal fund rate, which could lure more investors in rate-sensitive sectors such as real estate. In my opinion, Realty Income will continue to grow its dividend, which makes the REIT a top investment for income investors especially.

Previous rating

I rated shared of Realty Income a buy due to a strong dividend coverage profile, based off of adjusted funds from operations, and robust portfolio metrics (lease terms, diversification, occupancy). As a result, I figured that the REIT’s shares were Set For A New Upleg in May. Realty Income’s Q2’24 showed continual promise in terms of operational execution, especially in the industrial segment, and with the Federal Reserve set to approach its pivot point next month, I believe that more investor money could return to the real estate sector and to high-quality REIT choices like Realty Income.

Strong AFFO growth in Q2, solid dividend coverage

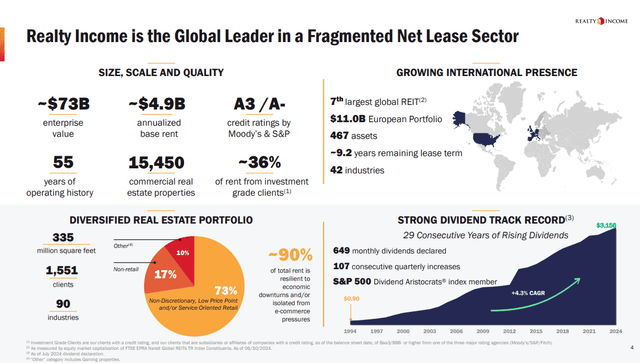

Realty Income remained a leading net lease REIT with a well-performing, diversified portfolio in the second-quarter. The REIT owned a total of 15,450 commercial real estate properties at the end of the June quarter, the majority of which were located in the U.S. Most of Realty Income’s assets belong to the non-discretionary sector and therefore these assets have a high degree of recurring cash flow.

Realty Income

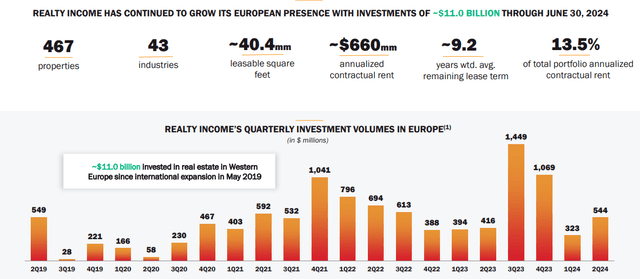

The REIT’s expansion in Europe has resulted in Realty Income building a formidable asset base overseas in recent years as well. In Europe, the REIT owned 467 properties valued at approximately $11B at the end of the second-quarter, and it now has a real estate presence in many European countries, including Germany, France and Portugal. Going forward, I expect Realty Income to continue to invest in lease opportunities (potentially via sale-and-leaseback transactions) in core European markets.

Realty Income

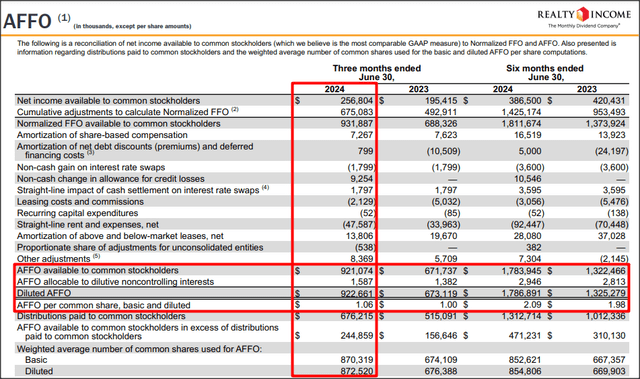

In the second-quarter, Realty Income saw a boost to its adjusted funds from operations, as past acquisitions made a positive impact on the REIT’s most important metric: adjusted funds from operations.

A REIT’s AFFO is typically considered a benchmark metric and used to calculate dividend coverage ratios: in the second-quarter, Realty Income generated $922.7M in AFFO (on a diluted basis) which calculated to 37% year-over-year growth. Last year’s second-quarter results did not include the properties previously belonging to Spirit Realty Capital, a REIT that Realty Income acquired last year in order to boost its portfolio and AFFO growth specifically.

Realty Income

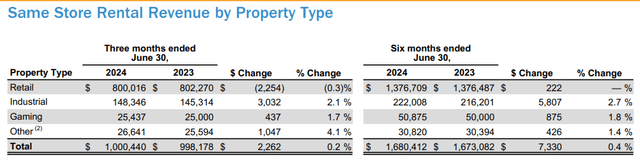

Key to Realty Income’s adjusted funds from operations growth is that the REIT succeeds in growing its same-store rents… which are depicted in the table below. In the first six months of the year, same store rents increased 0.4% year-over-year, but they rose especially quickly in the industrial segment: industrial properties increased their same-store rent contributions by 2.7% year-over-year, almost 6.8X faster than Realty Income’s consolidated results.

Industrial properties represented 14.5% of annualized rent in the second-quarter, which made it the second-biggest investment group after retail. Retail had a revenue share (on an annualized basis) of 79.4% at the end of the June quarter. Going forward, it would make sense for Realty Income to be especially aggressive in terms of growing its exposure to industrial properties.

Realty Income

Turning to dividend coverage and dividend growth.

Realty Income’s Q2’24 dividend coverage ratio, based off of adjusted funds from operations, was 1.37X in Q2’24 compared to 1.31X in the year-earlier period. The dividend is therefore very safe and has a high sustainability factor, in my opinion. Realty Income is also consistently raising its dividend, which makes the REIT a preferred income play for dividend investors.

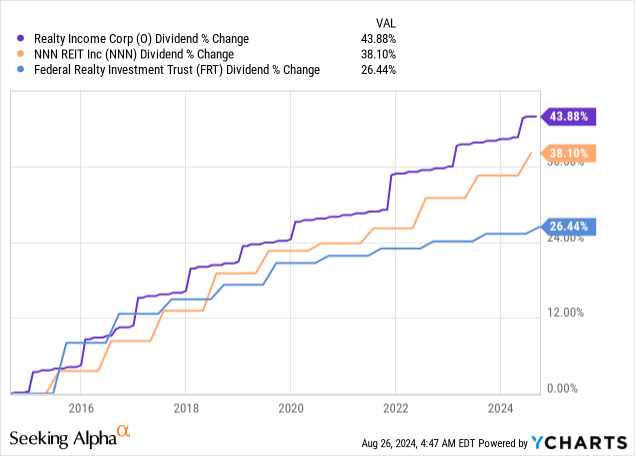

Realty Income has beat other net lease REITs in terms of dividend growth in the last 10 years and with management being laser-focused on growing the monthly dividend, I believe it has a good chance of extending this record into the future. Realty Income out-performed other net lease REITs in terms of dividend growth, including NNN REIT (NNN) and Federal Realty Investment (FRT).

Realty Income’s valuation

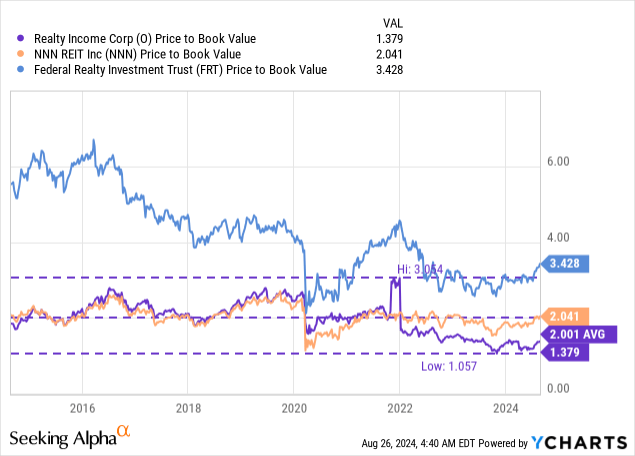

Realty Income can be evaluated based off of book value since the REIT is a large investor into, mostly, U.S.-based real estate. Realty Income is currently trading at a price-to-book ratio of 1.38X, which is still way below the company’s 10-year average price-to-book ratio of 2.0X. REITs like National Retail Properties and Federal Realty Investment trade at much higher P/B ratios, although I don’t believe this is really justified. Investors have turned more bearish on Realty Income in recent quarters due to the company doing a lot of acquisitions in the last several years.

I expect Realty Income, given the quality of its dividend/growth potential, to return to its historical price-to-book ratio of 2.0X in the longer term. A revaluation to the longer-term average P/B ratio therefore implies 45% upside revaluation potential and a fair value in the neighborhood of $88 per-share. This revaluation could be driven by a normalization of interest rates, which may attract more buyers to the REIT sector.

REITs are also often valued based off of funds from operations, or a derivative, such as adjusted funds from operations. The difference between FFO and AFFO tends to relate to one-off items like transaction or merger expenses as well as non-cash items, and the difference is typically very small on a per-share level. Realty Income and National Retail Properties have submitted AFFO guidance for FY 2024 (see below) and trade at P/AFFO ratios of 14.8X and 14.1X. Federal Realty Investment is trading at a P/FFO ratio of 17.1X, based off of funds from operations guidance. The higher multiplier for FRT is likely due to the company have an extremely long dividend growth history.

| REIT | Share Price | FY 2024 FFO Guidance | P/FFO Ratio |

| Realty Income | $61.77 | $4.15 – $4.21/share | 14.8X |

| National Retail Properties | $47.02 | $3.31 – $3.37/share | 14.1X |

| Federal Realty Investment | $115.96 | $6.70 – $6.88/share | 17.1X |

(Source: Author)

Risks with Realty Income

The biggest risk for Realty Income, as I see it, is a potential down-turn in commercial real estate. Although the REIT is focused on long-term leases and has strong occupancy ratios (98.8% in Q2’24), a correction in U.S. real estate would likely impact Realty Income’s ability to raise rents. Since Realty Income is seeing strong growth, especially in its industrial property segment, a slowdown here would likely impact the attractiveness of Realty Income as an investment negatively and may also lead to weaker dividend coverage. Additionally, a slowing expansion in Europe is something that I would consider to be a negative development as well. What would change my mind about Realty Income is if the REIT were to see a decline in its occupancy rates, weaker same-store growth in industrial, as well as lower AFFO-based dividend coverage ratios.

Final thoughts

Realty Income continues to represent top value at a $61 share price. Shares have revalued higher in the last two months, which may be related to investors seeing less risk in the real estate market now that the Federal Reserve is nearing its rate inflection point. Realty Income’s financial results for the second-quarter were strong, and the REIT faced no material challenges to its dividend coverage profile. Industrial is doing well for Realty Income and investors should expect a growing diversification profile going forward, with more investments in industrial as well as in Europe.

Read the full article here