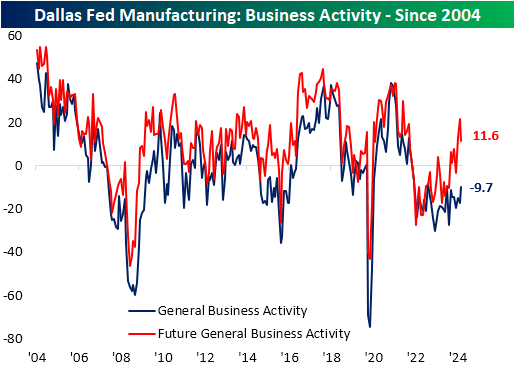

The Dallas Fed released its latest regional manufacturing survey this morning. At the headline level, the report showed the region’s manufacturing activity was stronger (or less worse) than expected, with the index for general business activity rising to -9.7 versus -16.3 expected and -17.5 previously. That is also now the highest reading since January 2023.

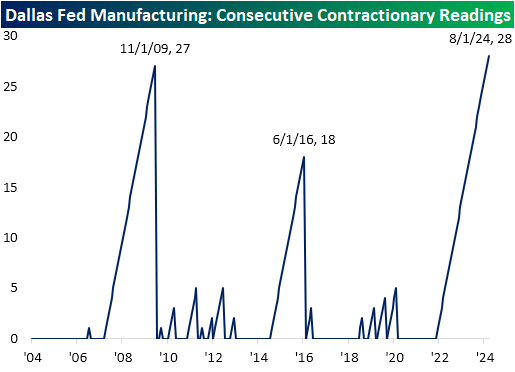

Although that result was stronger than expected and relative to the past few years, the index remains in negative territory meaning it was a 28th consecutive month of contractionary readings. As shown below, that now surpasses the 27 months ending November 2009 for the longest streak of contractionary readings in the survey’s history.

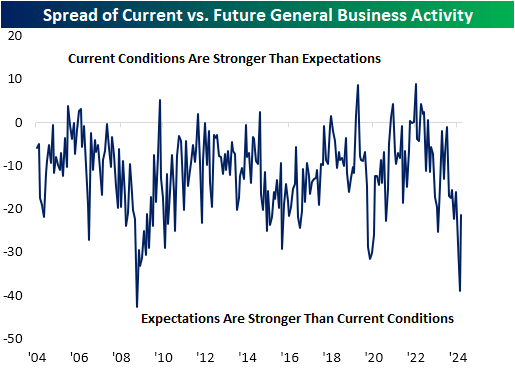

Additionally, headed into this month, the spread of the current and future General Business Activity indices was close to a record low, meaning that the region’s firms reported much more optimistic expectations for the months ahead than what they are currently observing. Historically, it has been common for expectations to be stronger than current conditions, but not to such an extreme degree as last month. With the increase in the current conditions index concurrent with a 10-point drop in the expectations index in August, the spread has narrowed dramatically, rising from a first-percentile reading into the 13th percentile.

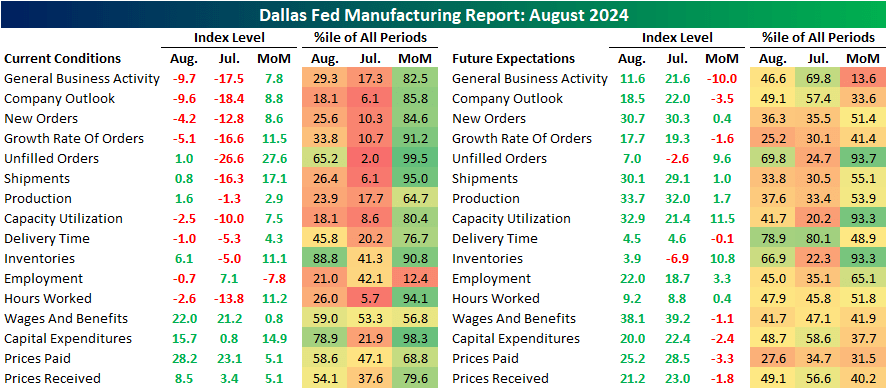

That improvement in General Business Activity occurred with strong breadth across most of the report’s categories. As shown in the table below, for current conditions, every index was higher month over month except for Employment which dropped 7.8 points. Not only were most indices higher, but several of those monthly jumps rank in the top 10% of all MoM moves on record. Thanks to those big increases, four indices went from contraction, back into expansion: Unfilled Orders, Shipments, Production, and Inventories. Again, the actual level of expectation indices has been stronger, but breadth in August was more mixed with half of the categories falling month over month and the other half rising. That being said, the 10-point drop in General Business Activity stood out as an outlier in terms of the size of the decline.

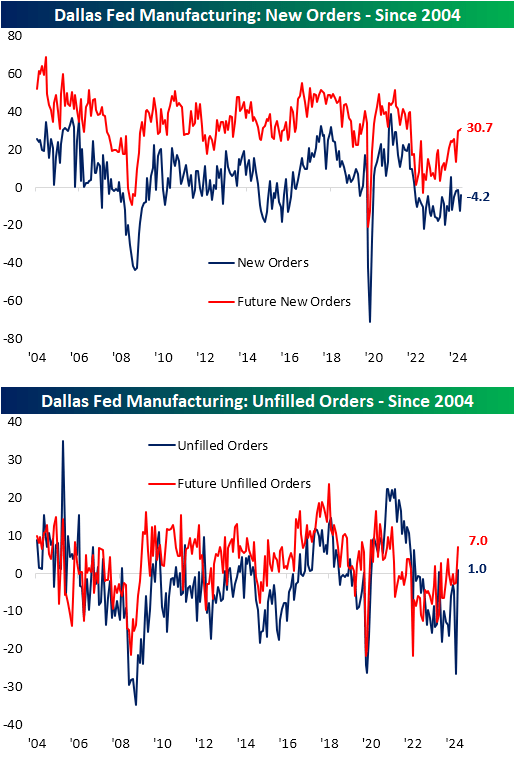

As noted above, multiple indices went from contraction to expansion in August, and most were related to demand. While the new orders index is still in contraction at -4.2, the expectations index for that category has climbed to the strongest level since March 2022. The Unfilled Orders index was even more impressive, with the index’s 27.6 point MoM jump ranking as the second-largest on record behind September 2005 when it rose by over 30 points. While that is only the first expansionary reading since last September, it’s the highest reading in 25 months. Meanwhile, expectations rose to the highest level since June 2021. In all, the report indicated that conditions are not yet improving, albeit there are some silver linings under the hood.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here