Introduction

Acelyrin (NASDAQ:SLRN) is a late-stage clinical biopharma aiming to fast-track the development and commercialization of therapies for diseases linked to overactive immune responses. Their portfolio includes several clinical-stage candidates targeting multi-billion-dollar markets. The lead product, izokibep, is a small protein therapeutic in Phase 2b/3 trials for multiple immunological conditions. Acelyrin also has ongoing trials for other candidates like lonigutamab and SLRN-517 for thyroid eye disease and chronic urticaria, respectively.

In my previous analysis, I recommended a “Buy” stance on Acelyrin due to its strong prospects in HS treatment with izokibep and robust financial backing. While the company faces risks inherent to biotech, such as clinical trial outcomes and regulatory hurdles, its $2B valuation and market response to similar drugs suggest high growth potential. I noted that investors should keenly watch the upcoming Phase 2b/3 izokibep trial results to recalibrate their investment strategy.

Recent Developments: Izokibep’s trial for moderate-to-severe HS showed mixed results. Initial statistical significance was impacted by early patient dropouts and rising placebo rates. However, sensitivity analyses revealed promising efficacy. Safety profile remained consistent.

The following article analyzes Acelyrin’s financial position, recent clinical trial results for izokibep, and future prospects. It shifts the investment recommendation from “Buy” to “Hold” due to mixed trial outcomes and market volatility.

Q2 Earnings Report

Looking at Acelyrin’s most recent earnings report, the company had a cash position of $823M, expected to fund operations through key milestones across all three clinical programs. R&D expenses rose sharply to $30M, mainly due to expansion of the izokibep program and the addition of two new clinical-stage programs. G&A expenses also increased to $12.7M, driven by organizational expansion. The net loss for Q2 2023 was $26M, up from $14.5M in Q2 2022.

Cash Runway & Liquidity

Turning to Acelyrin’s balance sheet, the total for cash and cash equivalents, and marketable securities is $556.2M and $266.8M, respectively, totaling $823M in liquidity. The “Net cash used in operating activities” for the six months ending June 30, 2023, is $56.9M, equating to a monthly cash burn of approximately $9.5M. With these numbers, the company’s cash runway is estimated to be around 87 months. It’s essential to note that these values are based on past data and may not be indicative of future performance.

Acelyrin appears to be in a strong liquidity position, with no mention of debt on the balance sheet. Considering the substantial liquidity and low monthly cash burn rate, the company seems to be well-equipped to fund its operations for an extended period. Moreover, Acelyrin’s relatively stable financial standing could make it a candidate for additional financing if needed. These are my personal observations, and other analysts might interpret the data differently.

Capital Structure, Growth, & Momentum

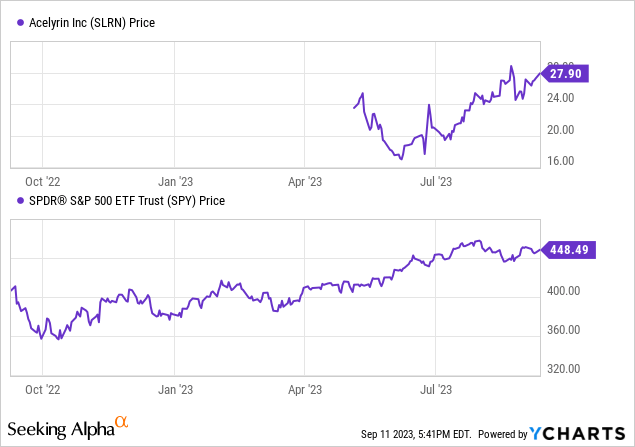

According to Seeking Alpha data, Acelyrin’s capital structure is solid, boasting substantial cash reserves relative to its $1B market cap (in after-hours trading) and no mention of debt. Growth is in a clinical-stage phase, yet to realize revenue, and the EPS shows fluctuating trends. Prior to today’s news, stock momentum was strong, outperforming the S&P 500 over a 3M period.

Reading Between the Lines of Izokibep’s Mixed Bag

The izokibep study for moderate-to-severe HS showed mixed results. Initially, using NRI analysis, the drug didn’t show significant effectiveness compared to the placebo. However, a different statistical method, LOCF, revealed that the weekly dosing did reach significance for the primary endpoint of HiSCR75 at week 16. Furthermore, an interim analysis suggested izokibep was performing well before an unexpected increase in placebo rates occurred.

A modified-NRI approach indicated that discontinuations among responders, mostly not due to adverse events, were affecting the outcomes. This alternate analysis showed a high level of statistical significance, especially for the weekly dosing regimen. In terms of safety, izokibep was consistent with its drug class, with no alarming adverse events.

The data is layered, requiring cautious interpretation. The rise in placebo responses is puzzling and could either be a statistical blip or point to trial design flaws. Discontinuation rates also appear to skew results, suggesting the modified-NRI might provide a more accurate measure of the drug’s efficacy. While izokibep shows promise, particularly in weekly doses, these nuances could impact its eventual market acceptance and success.

Upon listening to Acelyrin’s latest conference call, I discerned that the company admitted to issues with high dropout and placebo rates in their data. They remain committed to izokibep’s development for HS, noting dose-dependent efficacy. Plans are in place to revise their ongoing Phase 3 HS trial, which is currently “recruiting”, addressing the flaws observed in the Phase 2b/3 study. In my opinion, while the reported issues do raise concerns about izokibep’s efficacy for HS, the drug’s development is still worth watching.

Strategic Diversification Elevates Market Opportunities

Outside of HS, the company still has several avenues:

-

In Psoriatic Arthritis (PsA), izokibep showed strong 46-week Phase 2 results, with the Phase 2b/3 trial’s top-line results expected earlier than initially planned.

-

In uveitis, izokibep is being tested in a Phase 2b/3 trial, targeting a condition with significant unmet medical need.

-

Ankylosing Spondylitis (AxSpA) is another target for izokibep, with a Phase 3 trial planned for 2024. Previous data suggests potential for significant patient benefits.

-

Lonigutamab is being developed for thyroid eye disease, offering potential safety and convenience advantages over existing treatments.

-

SLRN-517 is in early-stage trials for chronic urticaria and could have applications in other mast cell-driven disorders.

Despite setbacks in the HS space, the company has a diversified pipeline that could offer multiple market opportunities, especially given the strong momentum in PsA and strategic forays into high-need areas like uveitis and AxSpA.

My Analysis & Recommendation

The alarming 60% stock drop in after-hours trading following the disappointing HS data on izokibep might appear to some as the market writing an epitaph for Acelyrin. However, this knee-jerk reaction seems to be an overcorrection, fueled more by sentiment than by a sober assessment of fundamentals.

Firstly, it’s essential to remember that the HS trial outcomes weren’t entirely disheartening. While the early dropout and heightened placebo rates were setbacks, pre-planned secondary analyses still showed promise. The company’s commitment to addressing these issues in an amended Phase 3 trial adds a layer of confidence in izokibep’s potential.

Furthermore, Acelyrin’s liquidity position is robust, with an $823M war chest expected to last approximately 87 months at the current burn rate. Such financial health allows the company flexibility to redirect focus and resources if HS becomes an intractable problem. In addition, the pipeline beyond HS—ranging from PsA to uveitis and AxSpA—still offers multiple shots on goal. Therefore, despite the HS stumble, the diversified strategy serves as a cushion against total failure.

Investors should be vigilant about upcoming milestones, particularly any adjustments made to the HS trial and the Phase 2b/3 results for PsA. Additionally, any signs of debt accumulation or changes in the cash burn rate should be red flags, considering these could drastically alter the company’s comfortable liquidity situation.

In light of the mixed bag of HS trial results, market volatility, and yet considerable long-term potential, I am downgrading my investment recommendation from “Buy” to “Hold.” At this point, the stock seems more like a high-risk, high-reward bet that existing investors might consider retaining but new investors should approach with caution. Izokibep’s story isn’t over, but it’s definitely time to recalibrate expectations and strategies.

Read the full article here