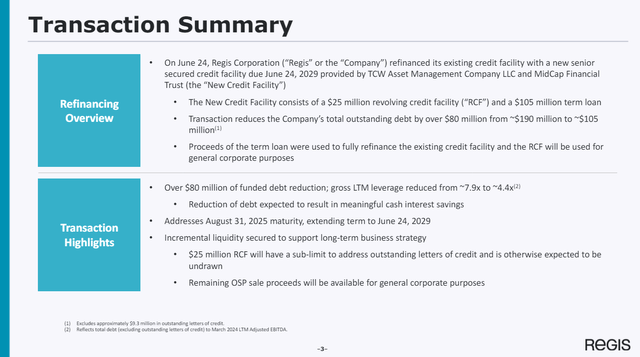

News broke this morning that Regis Corporation (NASDAQ:RGS) had refinanced their outstanding indebtedness. The key terms are as follows:

Regis Transaction Terms (RGS Investor Deck) Regis Transaction Terms (RGS Investor Deck)

As I noted in my March piece,

I think Regis is at an interesting inflection point, and I expect the conclusion of their efforts to address their debt maturities will give an all-clear signal to the markets to own the equity. Then, investors can get back to tracking Management’s efforts to stabilize the business and steer Regis to a profitable future. If not, investors are likely to lose some or all their investment. An investment in Regis carries plenty of risk, and much potential reward.

This outcome exceeded my most optimistic assumptions, and I want to break down why.

Why The Deal Is Good

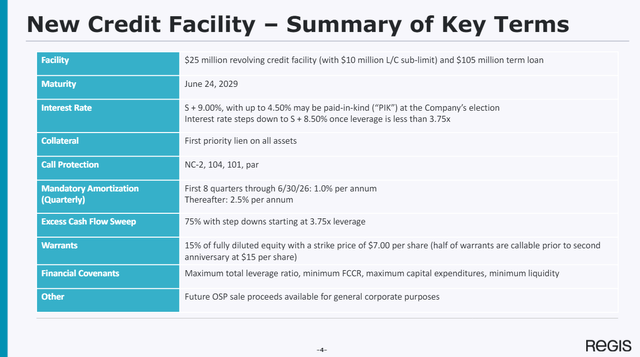

- Bank of America (BAC) took a haircut. Per the transaction 8-K, “In connection with the refinancing, the parties to the Existing Credit Agreement elected to terminate the Existing Credit Agreement (pursuant to the terms therein), whereby the lenders under the Existing Credit Agreement accepted a payment of $94 million in satisfaction of the roughly $190 million of principal and accrued interest outstanding. The Company incurred no breakage costs as a result of the termination.” As a result, Regis significantly reduced their total debt outstanding at no cost to their shareholders.

-

The new deal significantly reduces leverage (7.9x to 4.4x on a TTM basis). While the interest rate is still high (~14%), gross interest payments are lower, allowing Regis to delever via free cash flow. This was the key outcome I was looking for in my last article because previous interest expense was consuming all cash generated from operations.

-

This refinancing does not include the Zenoti payment expected later this year. Regis noted in their 10-Q the payment will not be as significant as previously expected but should still result in material deleveraging upon receipt. One estimate places this payment value at $15m.

-

Dilution from this transaction is minimal. The new lenders receive 15% of the fully diluted shares as warrants with a $7 strike, with Regis retaining the right to take out half the warrants at $15. Assuming a fully diluted share count at 3m shares (2.28m outstanding as of last 10-Q and a couple of hundred thousand outstanding employee awards) places this at 450k warrants. Compared to recent situations like Barnes and Noble Education (BNED), which I warned about in my October piece, Regis has taken care of common holders with this transaction.

What’s Next?

I previously noted:

Reading between the lines, I think Regis will normalize around 4,500 locations and generate $75m of annual franchising revenue against $40-45m of run-rate SG&A. $30-35m of EBITDA.

I want to revise this based on the most recent earnings report, and would now expect them to normalize closer to 4,000 locations, $70m of revenue, and $35-40m of SG&A. The continued rate of closures has been discouraging, but I am encouraged by the progress on SG&A cuts. Ultimately, this should still allow them to achieve $30m of EBITDA in the near term. With interest payments now under $15m a year, de minimis CapEx, and NOLs available to continue offsetting taxes, this allows for meaningful deleveraging on top of the Zenoti paydown.

Valuation

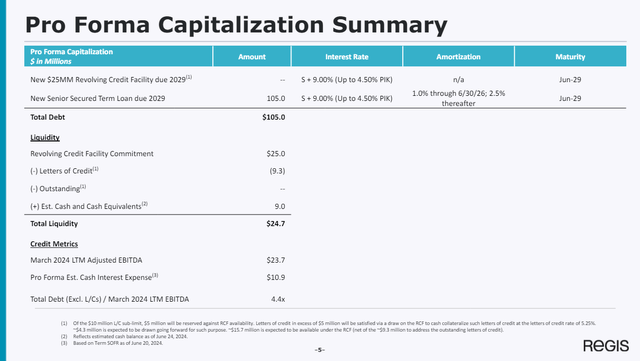

The pro forma cap structure is as follows:

Regis Capital Structure (RGS Investor Deck)

Regis now sits with $96m of net debt, and a ~$45m fully diluted market capitalization at $15/share (assuming 3m share count as above). This is 141/23.7m = 5.95x TTM EV/EBITDA and 141/30m = 4.7x my EBITDA estimate. The company should be able to reduce debt to ~$80m by YE25 if EBITDA is closer to TTM run-rate, or $60-70m if $30m is the right number. In both cases, I don’t think 5-6x EBITDA will remain the appropriate price, and I believe this transaction has given the company tremendous breathing room to focus on the business. I think a mature, stable franchising business should command at least a 7-8x EBITDA multiple, what could that look like?

- 30m EBITDA * 7.5x – 65m debt = $160m/3m shares = $53.33/share

Leverage is great when it works.

Risks

- Yes, leverage is great when it works. That said, if the business deteriorates faster than it can deleverage, it will be very painful. Regis needs to delever debt faster than earnings decline, which will get harder as the store base gets smaller. A return to growth would solve this.

- The Zenoti milestone payment could disappoint investors given the number of closed salons since the deal was announced. Since the company hasn’t guided to a specific number recently, I tried to avoid giving it much weight in my calculations above.

- Bank of America took a massive discount to get out of their loan. In situations like this where the debt was likely already marked down significantly on their books, I understand why a workout team would take this deal, but investors will certainly view this skeptically until the dust settles. “Did they know something” rumors are bound to swirl. I expect they weren’t interested in owning the company and might have gotten run over by a DIP lender in a refinancing situation.

- Regis took an expensive deal from their new lender, which suggests the business isn’t out of the woods. The company had to be distressed to get BofA to take a discount, I can’t have it both ways.

Conclusion

Regis Corporation is an early contender for “refinancing of the year,” having taken out a significant portion of their debt at a steep discount and refinancing with a clear path to further deleveraging. It’s not often you see a micro-cap management team navigate a situation like this and do right by shareholders, so they are due special recognition. Your equity holders thank you, and your stock’s performance today reflects the fruits of your labor.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here