About ReNew Energy

ReNew Energy Global Plc (NASDAQ:RNW) is a UK-based firm, incorporated in 2011, that has made its mark in India with a strong focus on harnessing non-traditional, eco-friendly energy sources. They’ve neatly divided their operations into two main segments: Wind Power and Solar Power. Adding to their core operations, they’ve ventured into ancillary services including engineering, procurement, and construction, operations and maintenance, as well as consultancy services.

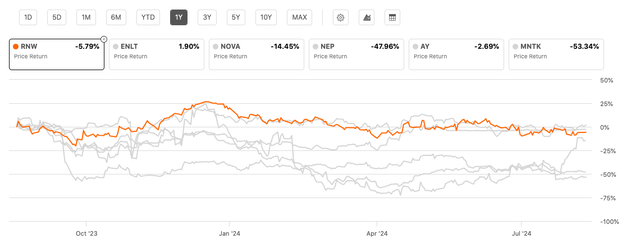

RNW Peer Performance

Seeking Alpha

Although RNW’s 1-year price return is down 6%, it’s holding its own in a peer space of losses across the board, most notably MNTK and NEP, both down around 50%.

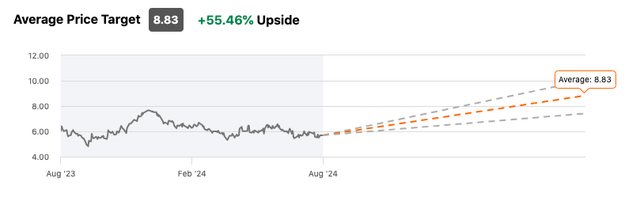

RNW Ratings

Seeking Alpha

Both Seeking Alpha analysts and Wall Street have an average weighted ‘Buy’ rating on the stocks. Wall Street, in particular, is very bullish on the price target, with a general price target consensus roughly 50% higher from here.

Thesis

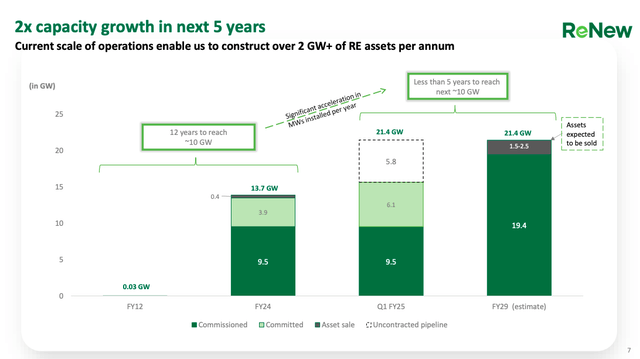

Back in June 2023, I examined the stock in “ReNew Energy: Leverage Concerns Cloud Strong Financial Performance” in the context of the renewable energy market, noting both the company’s strengths and potential risks. Last year, the portfolio included 10.69 GW of wind, solar, hydro, and firm power projects, with 7.57 GW already commissioned and 3.12 GW pledged. Currently, the total operational capacity stands at approximately 9.5 GW, consisting of 4.7 GW each in wind and solar, and 0.1 GW in hydro, with a total income for FY24 of USD $1,158 million.

ReNew Energy Investor Presentation

In my research, in the bullish corner, I noted that RNW had solid financials, especially EV/EBITDA and Price/Cash Flow, which demonstrated efficient cash-flow management and that it benefitted from India’s aggressive push for renewable energy. This, I reasoned, put ReNew in a position to leverage future market opportunities.

However, I also noted that the company had an extremely high leverage and considerable debt on its books, which would be a potential risk in the event of rising interest rates. Further, I pointed out the high EV/Sales, which might lead to overvaluation of the stock. These signaled that while ReNew Energy had the potential to grow, it also faced numerous headwinds.

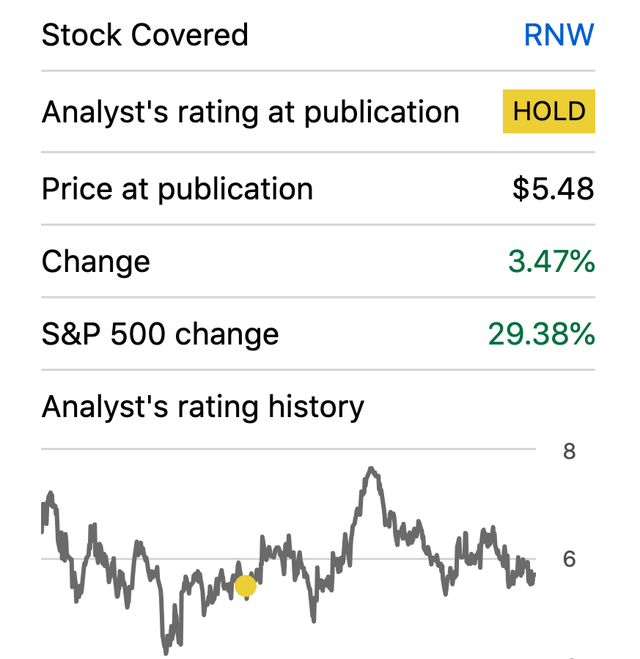

Based on my concerns, I gave the stock a “Hold” rating, it didn’t see any significant movement in price, but did show promise just before and after its Q2 results. However, that momentum quickly faded, even after signing an MoU (Memorandum of Understanding) for up to $1 billion over three years to support financing and development of ReNew’s global energy transition projects, including solar, wind, green hydrogen, and energy storage.

Grassroots Trading RNW “Hold” call performance

Since my call to hold, RNW is only slightly positive during that time frame, up around 4% vs. the S&P 500’s (SP500) 30% gain.

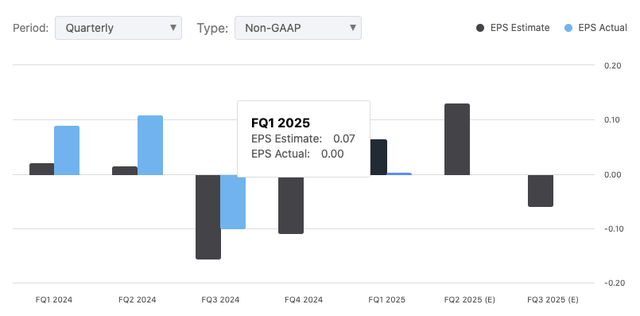

Today, I revisited ReNew Energy Global after recently dropping their Q1 2025 earnings. EPS came in at $0.00, missing by $0.06.

Seeking Alpha

Revenue? $271.69 million, which was missed by $34.28 million and is down 9.42% year-over-year. In my analysis, I argue that despite strong growth potential fueled by India’s push for renewable energy, I see red flags. High debt, weather risks, and overvaluation are also real concerns.

Green Hydrogen: India’s Big Move in Clean Energy

As I noted, ReNew Energy is a big player in the renewable energy industry, especially in India. By 2024, the company has secured agreements to produce about 15.6 gigawatts (GW) of energy, which is a huge amount, and most of this energy is generated within India. This makes ReNew one of the top independent producers of clean energy in that country. So while they are beginning to expand their business internationally, their main focus remains on India.

India is setting big goals and making large investments to transform how it generates energy, and one of the main goals is to reach 500 gigawatts of renewable energy by 2030. To put this into perspective, India is planning to spend a lot more money on renewable energy-about 83% more by the end of 2024, bringing the total to $16.5 billion. And most of this money will go into solar and wind energy, especially solar, where India added a huge amount of capacity (10 GW) in just the first few months of 2024, which is five times more than the previous year.

India is also focusing on a new technology called green hydrogen. Green hydrogen is produced through electrolysis, using renewable energy, primarily wind or solar, to split water into hydrogen and oxygen, without producing carbon dioxide, a greenhouse gas. Apparently, according to the World Economic Forum (WEF) green hydrogen is one of the cleanest alternatives to the current fossil-fuel-based industry. The government began a program called the National Green Hydrogen Mission by investing around $2.5 billion to make India a leader in this field. The aim was to produce 5 million metric tonnes of that green hydrogen by the end of this decade.

One of the key philosophical driving forces behind these initiatives is the WEF. To make all of this happen, the Indian government is offering various incentives and support measures (like with RNW), such as encouraging local companies to produce advanced energy technologies like batteries and equipment needed for green hydrogen. They are also investing in improving the power grid to handle more renewable energy.

RNW Q1 2025 Earnings Highlights

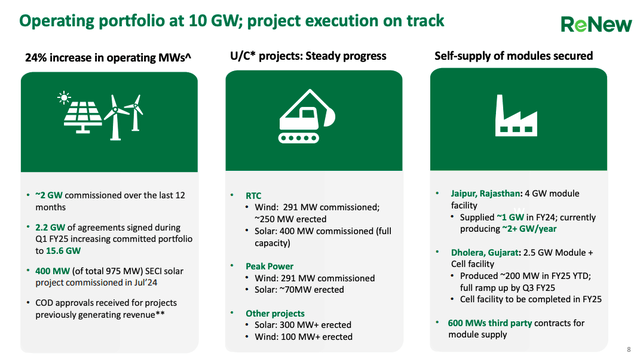

Looking over ReNew Energy’s most recent Q1 2025 transcripts, they appear to be on a strong growth path with a focus on expansion and efficiency, with aims to double its operating portfolio by 2029. For instance, RNW recently secured over 8 gigawatts of capacity in auctions, with 2.2 GW already locked into Power Purchase Agreements (PPAs). Add to this, a drive backed by the successful launch of nearly 500 megawatts (MW) of capacity this financial year, along with ongoing construction projects. In the past year, ReNew delivered 2 GW of capacity and is set to add another 1.9 to 2.4 GW next year.

ReNew Q1 2025 Investor Presentation

In terms of growth, ReNew’s management says the company’s on track to boost its financial returns and recent auction wins should bring in higher returns than before, thanks to lower module prices and a solid supply chain. The company’s manufacturing investments also give it an edge: the Jaipur facility, for example, is set to produce over 2 GW of modules this year, with the Gujarat facility expected to ramp up production by year-end.

ReNew also locked in external sales contracts for about 600 MW of module supply, making the most of its extra capacity. The company’s smart move on transmission connectivity, securing 22 GW for current and future projects, should boost profitability as these projects go live.

ReNew has shown steady financial growth. Operating capacity jumped 24%, even after selling 400 MW during the year. Revenue grew by INR 3.9 billion, and adjusted EBITDA rose by about INR 400 million, despite missing last year’s late payment surcharges. The company also outperformed in the merchant market, with higher returns from Round-The-Clock (RTC) and peak power projects boosting EBITDA. ReNew kept its leverage below 6x, showing solid capital discipline, and its access to diverse capital sources sets it apart. A positive way to view this is to acknowledge the company’s financial flexibility to recycle assets for capital.

Before diving into the risks & headwinds, on the surface, ReNew is showing strong capital discipline, keeping leverage below its 6x threshold and standing out with access to diverse capital sources. And finally, with a new solar cell plant set to go live later this year, ReNew management expects its plans are going to meet internal demand and tap into growing international markets.

RNW Valuation

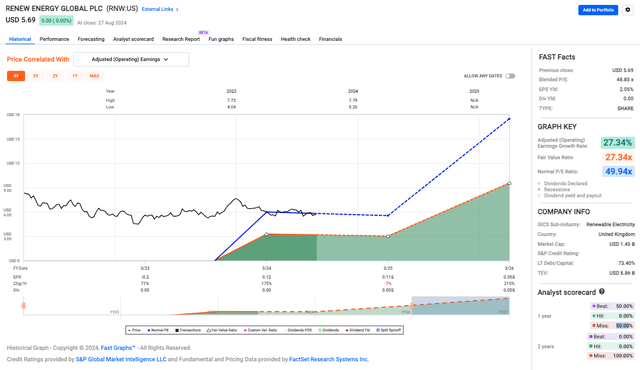

Renew Energy’s high blended P/E ratio of 48.85x shows that the market still expects big things from this company. And from the looks of it, an earnings growth rate of 27.34%, those expectations might be justified if the company continues to grow at this pace. So, for those willing to take on some risk and wait it out, the company’s growth potential in renewable energy could pay off.

FAST Graphs

But there are some red flags, I always need to mention for income seekers, RNW has no dividend yield, which means the company is putting all its money back into the business – typical for growth companies. The debt-to-capital ratio is a hefty 73.40%. And finally, the fair value ratio of 27.34x is lower than the normal P/E of 49.94x, which hints at overvaluation. That is, if the company doesn’t hit its growth targets, the stock price could take a hit.

Risks & Headwinds

Returning to Q1 2025, the positive outlook comes with a few bumps. For starters, adjusted EBITDA went up a bit, but it didn’t keep pace with big revenue gains. This was mainly because there were no late payment surcharges and less project income after selling 400 MW. The company’s revenue also dropped by about INR 1.3 billion due to a lower Plant Load Factor (PLF) in Q1, showing how weather-dependent it is. Wind projects didn’t do as well, once again, because of the weather, leading to more cautious future predictions and underscoring the risks of wind energy investments. While new wind turbine tech might increase PLFs by 10-15%, the recent performance is a subtle reminder to investors that returns can still be unpredictable.

From a glass-half-full perspective, ReNew’s leverage I mentioned in the highlights sits high at 5.7x, just under the 6x threshold, which could be a problem if market conditions worsen or unexpected financial issues arise. Furthermore, this leverage number doesn’t include under-construction projects or some business segments, possibly hiding another financial risk. Keep in mind, ReNew’s big focus on wind energy adds more challenges. This is because wind projects need almost twice the capital expenditure of solar, raising execution risks and the company’s success also depends on outside factors like module availability and supply chain security, which could affect its growth plans.

Speaking of weather volatility – it’s gonna always be a big risk in this space, as shown by its impact in Q1, and it could keep impacting future performance. Despite a weather-related setback, this quarter, CFO Kailash Vaswani sounded more optimistic. He noted:

I just wanted to end by reemphasizing that there has never been a better time to be an Indian renewable from a market opportunity, returns and capital deployment perspective. Coming to our guidance, while we had around INR1.3 billion impact from the weather this quarter, we saw the trend reverse in July and makes us confident that we will deliver on our annual EBITDA guidance. Hence, we are reaffirming our megawatts and lockdown guidance as well. Do note that historically our Q2 numbers have been about 10% to 15% higher than Q1 and we should see a similar trend in Q2 subject to weather conditions and adjustments related to LPS and project sold.

Also, worth noting is that wind turbine performance is not the issue here.

Finally, the company’s aggressive plan to double its portfolio by 2029 looks promising but comes with serious execution risks, especially with scaling up wind projects and managing a growing portfolio. The competitive auction market might squeeze margins over time, making it harder for ReNew to land projects with good risk-return profiles. The lack of pricing and margin details on the 600 MW external module sales could raise uncertainty, potentially impacting how the market views the company’s financial stability and growth prospects.

RNW Rating

I would mark the stock as “Hold.” ReNew Energy Global Plc has a strong growth outlook, which can be further driven by India’s determined attempt to increase its renewable energy capacity and its sound financials. However, the substantial leveraging, reliance on weather, and the fact that it might be overvalued – as indicated by a high P/E – pose commensurately substantial risks. The company is well-prepared for long-term growth, which is a highly positive point to bear in mind. However, in my analysis, the execution and, to a certain extent, market-specific risks mean that, for now, it’s probably best to hang back and observe further.

Read the full article here