Investment Thesis

Rent the Runway (NASDAQ:RENT) delivers a very compelling and tightly woven narrative of how the second half of fiscal 2023 will be substantially better.

Management discusses some of its strategies, including its willingness to reduce the discounting of its product.

However, with an overleveraged balance sheet plus its cash burn still very much in negative territory, I question the appeal of investing in this business right now.

I recognize that the stock is down a lot from its IPO, but I’m not sure if this is a viable business. Indeed, if we were to consider SBC as an actual expense, this business is truly quite unprofitable.

Why Rent the Runway? Why Now?

Rent the Runway is an online fashion rental service. It allows customers to rent high-end fashion items for a period of time.

Refreshingly, you’ll be astounded to read, AI was only noted once in the press statement and not even at the top of the press release, but hidden away in the middle. Perhaps if they’d been more proactive with sprinkling a few more AI mentions, the stock would be up premarket?

Moving on, in an interesting maneuver, Rent the Runway has decided that despite the tough macro environment, this is the time to cut back on being over-promotional. Here’s the quote from the earnings call,

[…] we are experimenting with being less promotional with our new customer offer pricing. We think this will improve retention and allow us to invest in improving the customer experience.

We do expect these experiments to reduce acquisitions in the short term, especially in our lower priced programs. As a result, we expect lower ending active subscribers in Q2 versus Q1. We think these are the right decisions for our customers and have factored these changes into our full year guidance of 25%-plus subscriber growth.

I understand what Rent the Runway is attempting to do. Rent the Runway is attempting to strengthen its brand, and deliver a higher quality experience, rather than fighting for the lowest price point.

I don’t know how this will ultimately work out, but it’s an interesting strategic move that warrants one following this business closely in the coming quarters.

That being said, Rent the Runway declares that despite cutting back on discounted items, it still expects to see its active customers growing by 25% in this fiscal year.

That being said, consider this, ending active subscribers was only up 8% y/y. How will ending active subscribers end up growing 25% y/y in fiscal 2023, particularly as Rent the Runway themselves are guiding for active subscribers to fall in fiscal Q2 2023 relative to fiscal Q1 2023?

When asked for more information on the call, this is what Rent the Runway’s management stated,

So, I’m not going to sit there and guide necessarily to what Q4 is going to look like relative to Q3, except to say that we’ve already provided confidents — a confident outlook in terms of plus-25% subscriber growth. So, we’ll leave it at that.

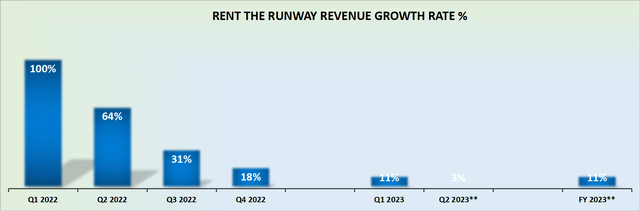

Revenue Growth Rates Set to Improve

RENT revenue growth rates

Management made a huge deal on the earnings call that Rent the Runway’s revenue growth rates are set to improve in the second half of fiscal 2023.

Given that Rent the Runway’s revenue growth rates have been rapidly decelerating with each passing quarter, the comparables with the prior year have become substantially easier, particularly fiscal Q4 2023.

However, we can now be sure of one thing, Rent the Runway is no longer a growth business. Next, we’ll turn to discuss the highlight of the quarter.

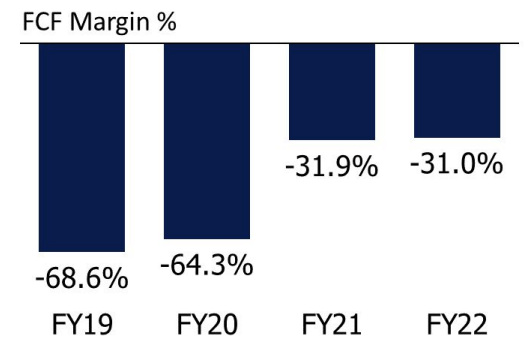

Profitability Profile in Focus

RENT Q1 2023

Rent the Runway guides its fiscal 2023 free cash flow margin reaching approximately negative 12%, or slightly better.

This would be a significant improvement relative to the past several years, where the improvement in its cash burn has been relatively muted.

However, the time for ”profitless prosperity” has come and gone. I’m not sure that investors are going to be overly enthused to back a company with lackluster growth, that’s burning through significant cash flows.

I recognize that Rent the Runway holds approximately $140 million of cash and equivalents. But that cash has approximately $280 million of debt against it.

The Bottom Line

There are few blemishes here, for one, the company’s overleveraged balance sheet. But on top of that, there’s the ongoing cash burn.

Ultimately, I question the viability the business.

Rent the Runway aims for subscriber growth despite expecting a decrease in active subscribers in the short term.

The company anticipates improved revenue growth rates in the second half of fiscal 2023. However, for now, we can be sure that Rent the Runway is no longer a growth business.

Overall, I hold a cautious view of Rent the Runway’s near-term prospects.

Read the full article here