Investment Thesis

Restaurant Brands International (NYSE:QSR) is now under pressure due to a weakening consumer and the outlook will not improve without a rate cut. Through its subsidiary Tim Horton’s, Restaurant Brands International is making a very significant push into the Canadian market, which will be one of the main drivers of organic growth. On the other hand, the company is not doing well in China and I think Popeyes’ expansion into European markets will be fraught with challenges. The company is a good fit for investors looking for dividend stability and share buybacks. I think the company’s stock is cheap today.

About QSR

Restaurant Brands International is one of the largest franchisors and operators of fast food restaurants. QSR owns brands such as Tim Horton’s, Burger King, Popeyes and Redhouse Subs. The company operates in the U.S., Canada and the International segment, which includes the operation of Tim Hortons franchises in South Korea and China, Burger King and Popeyes franchises in Europe and the Asia Pacific region. Firehouse subs then entered the MENA region markets. The source of Restaurant Brands International’s revenue is then from the operation of its own restaurants and the sale of products in the ancillary Tim Horton’s franchises, royalties from franchisees, revenue generated from real estate and advertising revenue paid by franchisees to QSR as a contribution to advertising campaigns.

Macro Environment

The current economic situation in the US, Canada and China is playing heavily against quick service restaurants. Low-income consumers, who are predominantly targeted by this type of restaurants, are weakening due to high credit card debt and also due to the high delinquency rate, which reached 29% in 1Q2024 for delinquencies 90 days or more past due. Credit card providers reduced requirements for new applicants at the beginning of the year, which has reignited demand for high-interest debt. In addition to the loss of excess savings, the high debt load of Americans, and the pressure to reduce spending in the discretionary sector, the significant price increases in fast food restaurants are a major concern.

I believe that the second half of this year will see a more significant weakening of consumer spending, which will put pressure on discretionary and staples going forward. However, part of this assumption is already priced into the stock. Consumers are looking for “value” now more than ever, which is putting pressure on fast food restaurants and in turn supporting the types of businesses that didn’t fare so well before, such as Chipotle Mexican Grill and Domino’s Pizza. I think the pressure on fast food chains will continue, so one way to win over the competition is to work with loyalty programs and brand positioning in general.

Tight consumer budgets have been instrumental in sparking a price war among fast food chains. While Burger King will now offer a discounted menu for $5 for an extended period of time, McDonald’s will only offer a similar menu with the same price tag in the summer time to not wake up demand.

Tim Horton’s

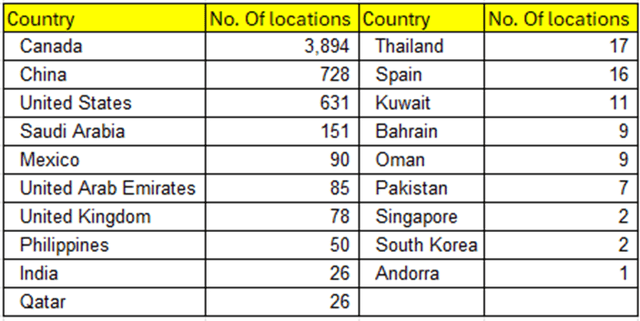

Tim Horton’s operates 3,900 locations in Canada, while TH has about 600 locations in the US. Tim Horton’s is a restaurant that focuses mainly on selling coffee and donuts. A survey of consumers found that Tim Horton’s is most popular with Generation Z in Canada compared to its competitors. This gives the company an excellent base for ad targeting as young Canadians, like other young people, use online channels in large volumes. I think the strong position with Gen Z is also a positive for QSR because this is the generation that is interested in a comfortable life, which often leads to well thought out purchases that the company can capitalize on. In addition, more than a third of the company’s clientele comes from affluent groups, which can help the company outperform the market at a time of pricing pressures on consumers. Tim Horton’s has about 3,900 locations in Canada, while Starbucks only has over 1,400. Tim Horton’s currently has no plans to expand its branch network in Canada, relying only on organic growth of its existing client base as well as population growth in Canada.

Source: Company data

Tim Horton’s operates more than 900 locations in China under TH International Ltd (THCH), of which approximately one-third are franchises. THCH stock is down more than 55% since the beginning of the year, even as Tim Hortons continues to expand its branches in China. The biggest problem for Tim Hortons in China is competition from Starbucks, Luckin Coffee and other locals. In addition, companies selling coffee are forced to specifically customize their offerings because coffee consumption in China is only 5 cups per person per year, while in the U.S. it is 240, so companies must adapt their business model to these trends.

Thus, Tim Horton’s starting position into the post-covid recovery of the Chinese economy is not entirely good. Although conditions for organic growth are not good in China, Tim Horton’s is looking to expand into as yet unpenetrated locations in northwest China such as Yinchuan. I think there is less potential in the northwestern Chinese provinces than in central China due to the generally lower wealth of the population and also migration to the southern regions of China.

Burger King

Burger King currently has just under 6,800 locations in the US, which is about ⅓ of all BK locations. In the US, Burger King competes mainly with the McDonald’s chain for market leadership. Currently, the market penetration is more favorable for McDonald’s as it has almost twice as many branches in the US compared to BK. Burger King is facing a change in the US. After buying the branches from franchisee Carrols Restaurant, the existing branches are being rebranded and remodeled and will be handed over to new local franchisees. I think BK’s rebranding could be successful.

Especially since BK is known for its bold advertising campaigns when trying to differentiate itself from competitors. On the other hand, Burger King is less profitable in this marketing. While McDonald’s marketing and sales expenses have been a steady 10% of total sales, in the case of Burger King (USA&CANADA&International), marketing expenses have been 25-28% of Burger King’s revenues over the past five years. I expect higher marketing costs to continue across the industry as companies have to convince consumers to return to restaurants, plus they are fighting “value” wars against each other.

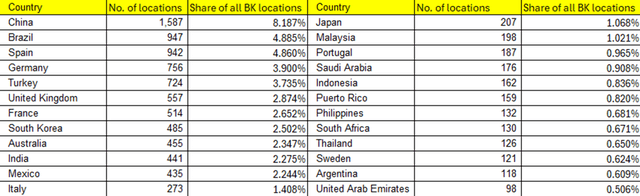

Burger King has most of its locations in the International division, about 12,000 locations. The table below shows the countries with the highest number of branches (more than 0.5% of the total) and the share of the total number of Burger King branches (including USA&Canada).

Source: Company data

The Chinese market is the most important international market for Burger King. China is specific for fast food chains selling beef. Chinese people prefer chicken to beef, while pork is at the very top. Hamburgers are popular in China and customers there like the Western style of eating along with elements of Asian cuisine. Local fast food restaurants selling burgers to lower income groups are popular in China.

Burger King has adjusted its menu on the assumption that Chinese people prefer chicken to beef, which has not met with much success. In addition, BK is facing significant pressure from McDonald’s, which has strengthened its position in China after buying a 28% stake in the joint venture from Carlyle and now holds 48% in the franchising partnership and 52% from Chinese company CITIC. I think McDonald’s is seen more as an established fast food brand in the Chinese market. Burger King is then compared to competitors of conventional fast food restaurants in the local market. BK is trying to improve its market position by expanding branches, but it will not have an easy competitive fight against the popular KFC and McDonald’s.

Popeyes

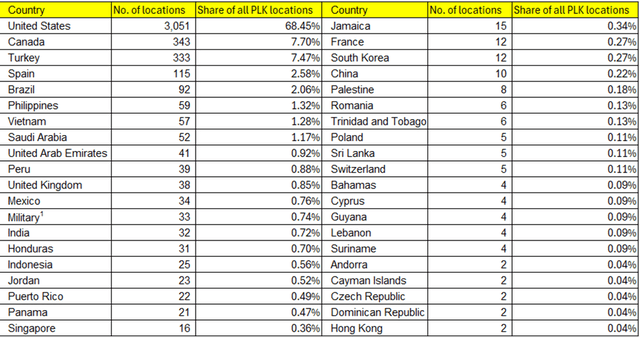

The chicken-centric fast food concept is so far mainly available in the US, Canada, Turkey and Spain. Restaurant Brands International is preparing a major expansion into Europe, where it plans to start expanding its presence in Spain and Italy. The expansion into the Czech Republic has opened doors for the company into other countries in the CEE region.

Source: Company data

Popeyes will open its first branch in Italy by the end of 2024. For markets where Popeyes does not yet operate, KFC’s performance is a leading indicator, as the two chains’ offerings are very similar. Italy is a very specific market for fast food chains selling chicken, as the strong culture of Italian cuisine limits the potential of fast food chains in that market. I see the potential for Popeyes in tourist-oriented cities where people will be more likely to look for fast food at a reasonable price. I see very similar future developments in Spain and am generally sceptical about expansion into southern Europe.

FireHouse Subs

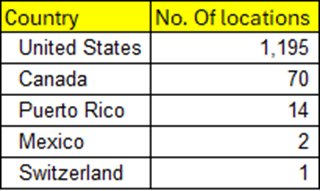

Firehouse Subs is a chain of casual restaurants specialising in sandwiches. This division is the smallest within QSR, and for now, management’s goal is to make it 100% digital before 2028, by which time a total of 2,000 locations are to be launched. Firehouse subs is a small format site that can be counted on to have a lower nominal cost of investment. With its focus on digital environment, there is scope for growth in operating margin. In my DCF model, I assume an operating margin of 58% for this division in 2028.

Source: Company data

Financials

Assets Structure

Restaurant Brands International has an asset-light business model, as 25,900 of its more than 31,000 restaurants are owned or leased directly by franchisees, and the company owns only 226 properties. In addition, QSR leases and subleases properties to its franchisees, which allows it to keep costs down for the company itself. On the other hand, the company is not able to profit from leasing properties to franchisees. The business model differs significantly from McDonald’s. In comparison, McDonald’s owns real estate on its own land valued at about 50% of all properties, with leased land buildings accounting for over 30%. Thus, QSR’s earnings have the potential for greater volatility, as lease fee income tends to be more stable than, for example, sales revenue, which is more dependent on the business cycle and the consumer.

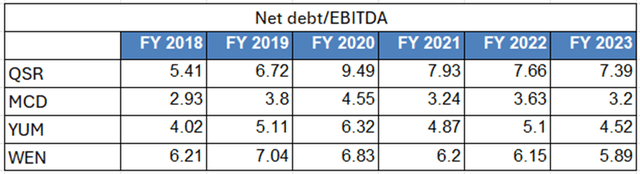

Debt Structure

Despite the capital-light nature of QSR’s business model, the company’s debt is the highest compared to its competitors; on the other hand, unlike Yum! Brands or McDonald’s, the company has positive equity. The high level of debt was mainly accumulated in 2014 and 2017 when the company acquired TIM Horton’s and Popeyes respectively.

Source: Bloomberg Finance L.P.

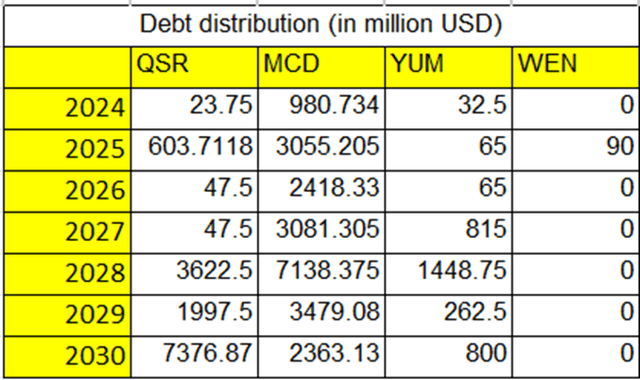

Debt Distribution

QSR will only be repaying most of its debt from 2028 onwards. In the meantime, it will have smaller maturities that it will be able to pay from free cash flow. However, the maturities in 2028, 2029 and 2030 will already have to be covered by new debt or by repayments from cash flow from previous years, as the present value of the FCF in 2028 will be, according to my conservative estimate, at USD 2,081 million, in 2027 at about USD 2,048 million and in 2026 at about USD 1,999 million.

Source: Bloomberg Finance L.P.

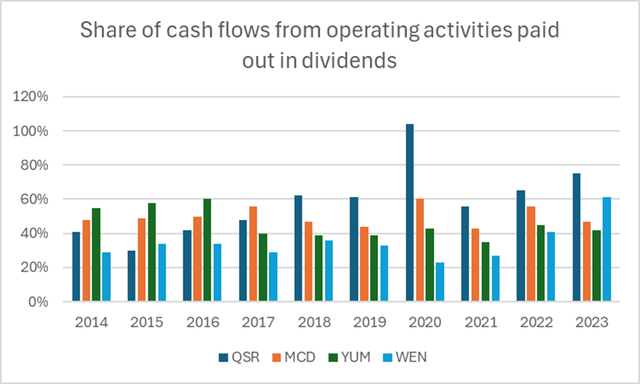

Cash Distribution

In the case of QSR, the largest component of cash flow distribution from operating activities is to dividends. The current dividend yield is 3.3% and the payout ratio on last year’s net income is just under 62%. Compared to peers, cash distribution through dividends is at its highest level in the long term, which attracts dividend investors. I believe QSR’s dividend policy is sustainable over the long term.

Source: Bloomberg Finance L.P.

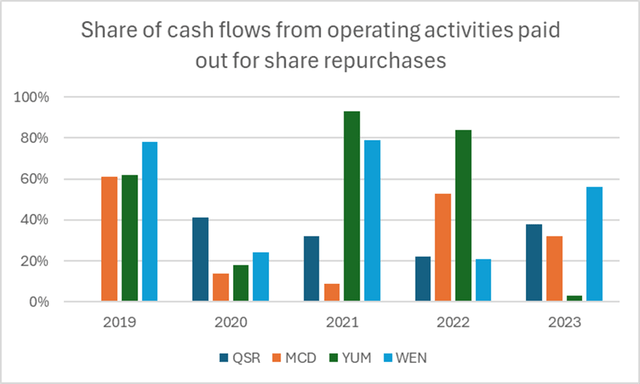

Restaurant Brands international has been making share buybacks on a regular basis since 2020 at a similar level to cash flow from operating activities as McDonald’s. QSR is prepared to conduct opportunistic share buybacks, which I view very positively. Given the current stock valuation, I expect activity in the current buyback program to continue.

Source: Bloomberg Finance L.P.

Valuation

Discounted Cash Flow Model

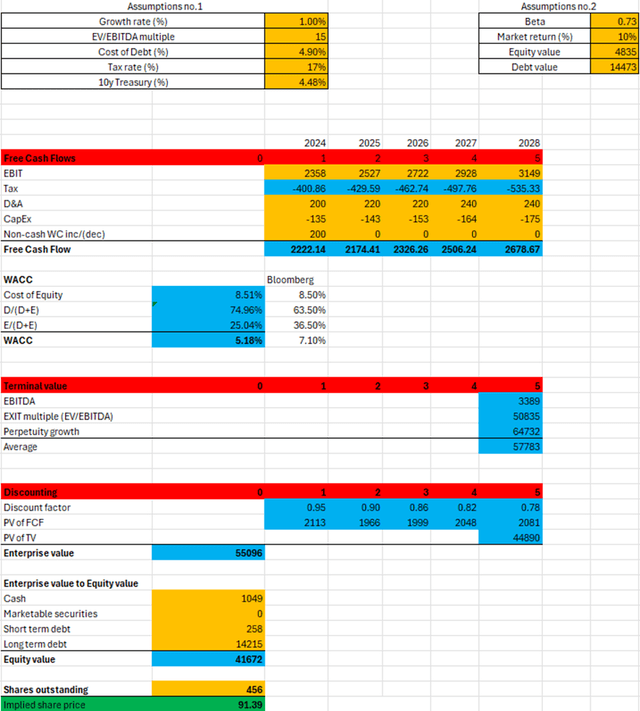

For the discounted cash flow model, I used a more conservative outlook for sales growth. For the TIM Hortons’ division, I assume 7.5% YoY growth through 2028, 4.5% YoY through 2028 for Burger King, 5.5% YoY for Popeyes under the same assumptions, 5.0% YoY for FireHouse Subs, and 7% YoY for the International segment starting in 2025.

My estimate is that operating margins could stabilize between 31% and 32% in the coming years due to a resurgence in demand and lower cost pressures. Further, the calculation assumes a cost of external capital of 4.9%, which could potentially increase over future years if interest rates remain stable, which is unlikely. The cost of equity is then 8.51%, giving a WACC used as a discount factor of 5.18%. The output of the DCF model is an implied price of $91.39 per share, this corresponds to about 31% upside relative to today’s share price. This estimate is within the market consensus range.

Source: Own calculation

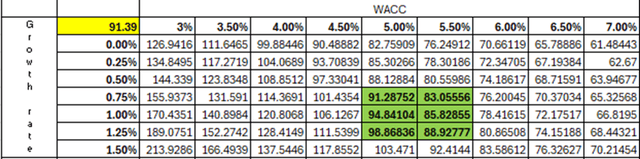

Sensitivity Analysis

Source: Own calculation

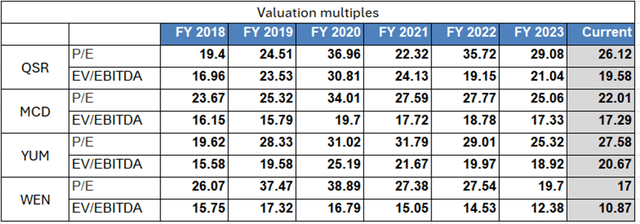

Valuation Multiples

Despite QSR’s higher debt levels compared to its competitors, the stock trades at a premium to its peers. I think investors are taking a positive view not only on the transformation of Burger King’s U.S. locations, but more importantly on the stability of the dividend and the prospect of continued buybacks as the stock trades at a discount to its historical average.

Source: Bloomberg Finance L.P.

Risks

Currently, the biggest risk for QSR and the entire fast-food chain sector is the search for value in the fast-food sector by consumers. This macro sentiment risk should subside as interest rates fall given that the inflationary wave has subsided. I see other significant risks in Popeyes’ expansion into Europe, with strong local cultures making it difficult for Popeyes to establish itself in southern European countries. The risk from competition in new markets for Restaurant Brands International is not insignificant, and I believe that if it materializes, the Popeye’s division will grow at a lower rate, depending mostly on the strength of tourists in the locations. I also see QSR’s presence in China under the Popeyes brand as problematic, as it is a direct competitor to KFC, which has a strong market presence there.

Conclusion

I think QSR has great potential to accelerate organic growth once consumer conditions ease. The macroeconomic situation has taken the stock to interesting levels. On the other hand, Popeyes’ expansion into southern European countries and its current presence in the Chinese market, where it plans to add 1,500 branches by 2028, are key to stronger growth. I view QSR as a company that can deliver value to shareholders through dividends and share buybacks, but I don’t think there will be much market share gain.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here