It was the weaker-than-expected jobs report for July that sent stocks cascading and bond yields plunging two weeks ago over concerns that the economy was on the cusp of a recession. That “growth scare” came to an end with yesterday’s retail sales report, serving as the exclamation point on what has been a six-day rally of more than 6% for the S&P 500 (SP500). We have not had a comparable surge in the index since the beginning of the bull market in November 2022.

Following that jobs report, I asserted that the economy was a lot stronger than it suggested, and that it was adversely impacted by Hurricane Beryl. That appears to be the case, given that initial jobless claims have fallen sharply over the past two weeks from a peak of 250,000 to 227,000. Sales and claims data led to a surge in the major market averages yesterday, with the Russell 2000 small-cap index (RTY) leading the way to a gain of 2.6%.

Finviz

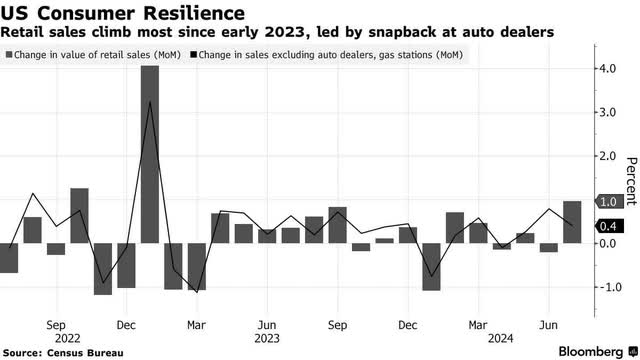

Retail sales rose 1% in July compared to expectations for a 0.4% increase, with ten out of the 14 categories tracked by the Census Bureau showing an improvement over June. The increase was led by autos, which were held back in the previous month by a cyberattack at dealerships, but even when we strip out autos, sales rose 0.4% to beat the consensus estimate of 0.1%. This report was far from robust, but it shouldn’t be, given that consumers have exhausted excess savings and wage growth has slowed from its peak two years ago. Still, it does reflect steady growth in the US economy.

Bloomberg

Further confirmation of consumer resilience came in yesterday’s second-quarter earnings report from Walmart (WMT). The company exceeded estimates and raised guidance for its fiscal year. Same-store sales rose 4.2% from a year ago, and online revenue soared 22%. Management indicated it was not seeing any softness in business so far in August. CFO John Rainey asserted, “we are not projecting a recession.”

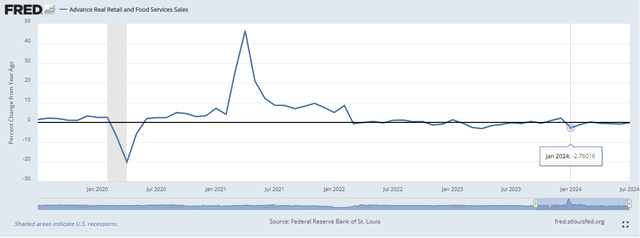

I wasn’t expecting one, either, even though retail sales have declined year-over-year on an inflation adjusted basis several times over the past two years. Normally, that would be a major red flag for me, but consumers have focused their dollars on services in this post-pandemic expansion to an unprecedented degree. Otherwise, the 2.7% year-over-year decline we saw in January of this year in real retail sales would have forced me to position more defensively.

FRED

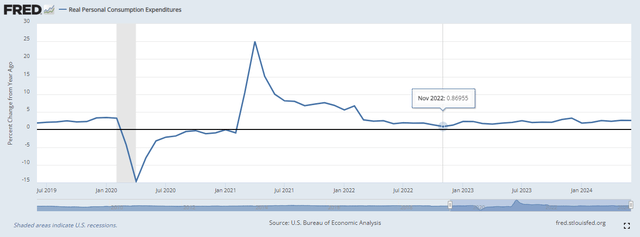

Given the emphasis on services, I have focused on the real year-over-year change in personal spending, which includes goods and services, as my primary leading indicator. On that front, the coast has consistently been clear with the low point in spending coming in November 2022, which was one month after the bull market began.

FRED

The reason inflation-adjusted consumer spending continues to grow on an annualized basis, fueling the expansion, is because we still have real income growth. As I shared yesterday, the increase in inflation-adjusted weekly income for production and non-supervisory workers in July’s Real Earnings report was 0.6% over the past year. That is down from 1.5% a year ago, but it continues to increase. When it starts to decline, I will be looking for additional signs that the economy is starting to falter, but that will be the most important one of them all.

Read the full article here