This article was co-produced with Wolf Report

We’ve written about Rexford Industrial (NYSE:REXR) a few times.

The question that best describes the company and the appeal here is:

“How high is a premium justified for a great REIT?”

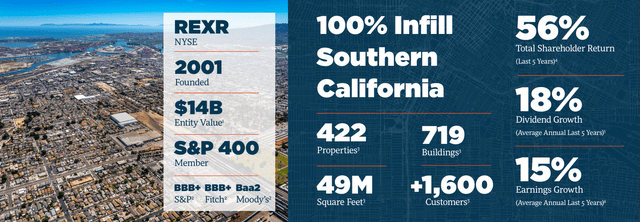

This is a great REIT – it’s a BBB+ rating, 3.7% yielding (wait for it), high-quality industrial player with an incredible asset base and asset portfolio that currently is in disfavor due to significantly negative macro sentiment in the Californian region (though this also seems to be turning around a bit).

We mean at this point in June 2024 to update our thesis for Rexford, an industrial REIT with what we view to be a rather significant upside if you’re willing to premiumize the company a bit.

As it stands, we’re willing to do that at this time.

REXR, with a market cap of over $11B, has a triple-digit total shareholder return over the past five years and a 19% annual dividend growth, making it a standout in the industrial REIT sector.

The company has what we view as an incredible overall upside, and despite being in the aforementioned Cali geography, the sheer scarcity of attractive land and tenant diversification makes this company a “shoe-in” for a conservative investment portfolio.

It might be an unpopular thing, investing in quality value REITs during this age of AI and “unending growth” and 100+x P/E multiples in some of these tech businesses – but this is how we invest, and how we like to invest.

So let’s update on REXR and let us show you what you can get at this time.

Rexford – the upside, if you accept a premium, is significant, and the company is qualitative

Aside from the low yield, there aren’t many negatives that you can point to with this company.

As we’ve mentioned before, the less growth you’re likely to have, the higher yield we should get.

The lower the yield we see, the more growth we expect.

There’s also a contextual component to this equation, meaning that we expect more yield in times characterized by higher interest rates – such as the one we’re currently in.

Because rates have gone down, the savings rate we’re able to get is now down to 3.75% risk-free.

That means that a company like REXR, with a yield of 3.7% is now suddenly quite a bit more interesting – not because of the company’s massive yield, but the combined upside with capital appreciation at a lower valuation and the yield combined.

Our portfolio position is down a considerable amount at this time, but we don’t expect this to be a problem in the long term.

We first bought shares during the fall of 2023 – not perfect timing, but decent.

So we’re still at a fairly good “upside” here. We started paying closer attention again when the company dropped below $55/share – and we’re paying a lot more attention at this time.

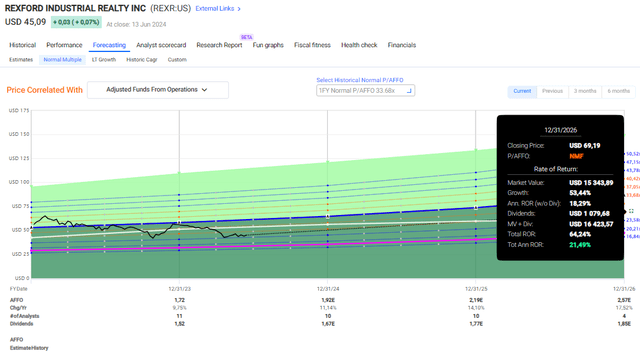

The company is now trading hands at $45/share, which represents less than 25x P/AFFO, which when you consider that the 5-year average is over 43x, could be cause for some pause and really look closely at the upside here.

One of the core questions is – is the growth thesis broken?

By this, we mean does the company still have the potential to grow at double digits on a forward basis, or is it now far less than this?

As we see things now, the company still has this potential.

The latest set of results for REXR, we are still the 1Q, came during April. The net income dropped – but the share of core FFO increased by 20.3%, consolidated NOI increased by almost 15%, same-store property NOI was up 5.5% and Cash NOI was up 8.5%.

So growth, not double digits everywhere, but still impressive growth – and with an occupancy of almost 97% for an industrial REIT.

The company also blows any notion out of the water that California would be dropping in terms of rent levels, by presenting a comparable rent increase of 17.3% YoY, and 13.2% on a cash basis at renewals and new leases.

Any bears on this company or doubting the average premium should first square with this set of forward expectations.

The company also delivered on $1.1B worth of acquisitions going forward.

Management commentary was in the vein of as positive as previously, and despite a somewhat slower growth rate, expectations for the forward double-digit growth rate are not in any way impacted or moderated here.

This also goes for debt, which remains at very low levels at a net debt/EV of 20.9%.

REXR IR

While peer averages are not slow in growing either, the 15% CAGR the company offers is a meaningful and non-trivial change from the peer average 11% CAGR – and this translates into higher consolidated NOI growth, and dividend growth.

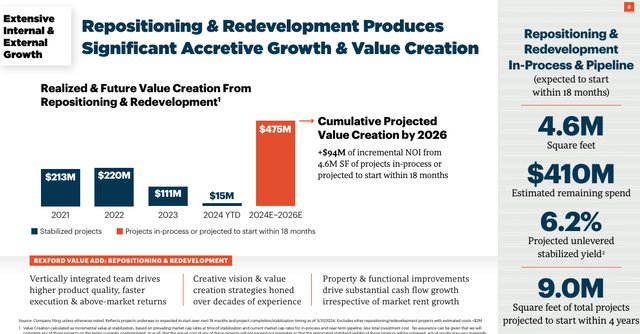

Rexford is set to grow both internally and externally.

Internal growth is set to come from significant repositioning and redevelopment, to the tune of $94M higher in quarterly projected NOI for 2027 and beyond.

Aside from that, there is accretion, rent steps, mark-to-market adjustment and the like. All of this together is expected to grow quarterly NOI by 47% until 2027. This is what this repositioning and redevelopment pipeline currently looks like.

REXR IR

The REIT is also likely to continue to acquire properties at attractive rates and attractive fundamentals – since the IPO, the company has grown on average 22% annually by square footage, and there is little reason why the company should not continue to do this.

Over 85% of its acquisitions are made off or in very lightly marketed transactions, which are the “best” to work with here. REXR also continues to forecast a 5% projected initial unlevered yield on a cash basis.

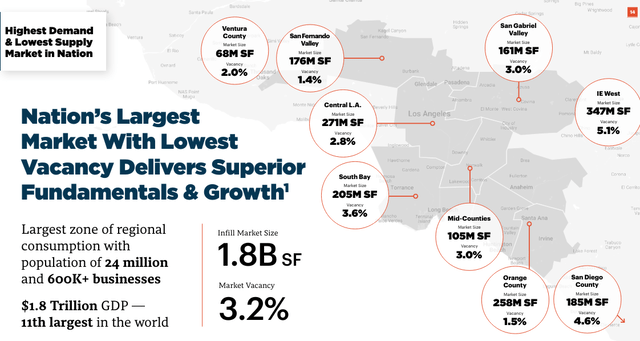

And, of course, Infil SoCal is the 4th largest industrial market in the entire world, with some of the highest demand and lowest supply markets in the entire nation, despite what media is portraying the area as currently.

REXR IR

By the way, we’re not saying that what is being said in the media regarding SoCal of California issues is wrong – the state is going through a bit of troubled times.

But it’s worth remembering that troubled times usually, especially for an area like this, do pass. We belong to the group that does not expect the market here to truly “crash” down for the long term or in any permanent manner.

If you, on the other hand, as an investor do consider this likely, then Rexford probably isn’t right for you.

For the rest of us, here is what the company’s valuation currently dictates to us.

Rexford – Valuation upside exists, and is now significant at an intact premium

As we’ve said in previous articles, our inclination to premiumize high-growth companies is, at best, hesitant or light.

Since our last article, REXR has seen a meaningful drop in valuation due to somewhat moderated forecast estimates for the coming years.

The current AFFO expectations are for double-digit growth – 11-18% for 2024-2026E per year, respectively. This, with a 22% beat, a 66% hit, and only an 11% miss ratio, is good (Paywalled FAST Graphs Link).

We would want to forecast the company at closer to 27-28x P/E, which is lower than the company has ever traded on a 1-20-year average. The lowest we can find at any one time period is 33.7x. So I forecast only at 27-29x P/AFFO – but even that offers significant investment upside.

FAST Graphs

This is the lowest, conservative upside we would consider valid – but you can also see here that even forecasting as low as 20x based on this growth estimate, you still wouldn’t see negative RoR for your investment.

At close to 30x P/AFFO, the company would generate annualized rates of return of almost 27% per year – a very solid profit for anyone looking for a good investment.

So you can see that both on the bearish and the bullish side, this company’s forecasts are extremely well protected, and in a way where we would say that it makes up for the low yield that we’re getting here. That yield is also, obviously, expected to increase.

A few days during 2014 was the lowest valuation we ever saw for REXR, and this valuation was at 17x P/AFFO is the lowest this company has ever come close to in the last decade.

While we expect the road to be rocky, we do not expect it to be as negative as that – otherwise, we’d probably wait before we put money to work here.

Analysts expect the company to grow going forward – though the price targets reflect a far more modest forward expectation than we put forth.

A mix of 13 analysts comes in at a range starting at $45 on the low side to $70 on the high side. The negative adjustments in forecast expectations for 2024 also mean that we’re cutting our price target for the company – but to $75, not below.

We believe the market and analysts are underestimating the stickiness of the company and its model, as well as the underlying strength of the entire SoCal geography.

The current average target for the company is still a $54/share, which might not be close to our target at $75/share, but we consider the analysts underestimating REXR here.

We maintain a price target for REXR as of this particular article, which brings us to almost 20% upside, and the company is trading at around 0.83x to NAV, where we’re at least expect the company to trade at a full 1x.

The trends in the company’s portfolio justify such a premium, and the low risk of oversupply in the geography is major downside protection here, as we see it. Only in places like Detroit is the risk of oversupply less (and for entirely different reasons than here).

For that reason, we consider the company attractive with the following upside and thesis as of June 2024.

Thesis

- REXR is perhaps one of the highest-quality industrial REITs out there. Its fundamentals and overall safety are remarkable, with one of the lowest leverage out of any REIT we’ve researched. This goes some way to make up for the yield that’s currently below a savings account interest rate.

- The upside here is coupled in reversal, yield, and growth. That upside is massive – and because of this, this investment is far better than any savings account. We give the company a conservative PT of $75/share, a downward adjustment due to a cut in estimates, representing a conservatively adjusted 2025E 27-29x P/FFO level.

- Based on this, we consider this company an impressive “BUY” here, and like with apartment REITs such as AVB or ESS (we’re choosing to take the contrarian view of California here and go “BUY”. For June 2024, we don’t see a whole lot of companies that do “better” here.

Remember, we’re all about :

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, we harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, we buy more as time allows.

4. We reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are our criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

We won’t call REXR cheap at 24.9x P/FFO, but we will call it “BUY”able. It’s time to load up, and we’re adding more REXR in the near term.

Read the full article here