Introduction

Ripple (XRP-USD), a pioneering blockchain network, has seen its native coin XRP rise to become the fifth-largest cryptocurrency by market cap. Investor sentiment towards Ripple has shifted since the latest ruling in the long-standing SEC-Ripple case. Following the announcement of the ruling, Ripple’s native coin XRP resumed trading on certain crypto exchanges that had previously delisted XRP trading pairs because of the SEC litigation. Institutional investors, who were once hesitant to engage with investment products centered around XRP, have now shown renewed interest in this digital asset.

Crypto ETP platform, CoinShares, released a recent report that highlights digital asset fund flows. The report reveals that digital asset investment products saw inflows totaling $29 million this past week. The new wave of inflows was preceded by a three-week streak of outflows totaling $144 million. Bitcoin had the highest amount of inflows, totaling $27 million.

According to the report, XRP saw inflows of $0.5 million and is on a 16-week inflows streak, representing 12% of assets under management (AuM). XRP’s AuM has risen 127% YTD. And the XRP ledger has witnessed an increase in the number of daily transactions, averaging 1.2 million daily transactions since the start of this month.

XRP Real-World Adoption

The utility of a blockchain network is directly tied to its practical applications in the real world. Ripple is focused on cross-border payments, and I think this is one of the use cases that could drive the mass adoption of blockchain technology and cryptocurrencies. Ripple has built a suite of products aimed at solving the problems the present cross-border payment network face. Over the years, Ripple has actively engaged in partnerships and collaborations with payment networks, banks, and government financial entities to integrate or explore the use of blockchain technology. Some of Ripple’s recent partnerships and collabs include:

-

MasterCard CBDC Partner Program: MasterCard (NYSE:MA) announced a new partner program which the company says is “designed to foster collaboration with key players in the [digital asset] space so they can drive innovation and efficiencies.” Ripple is on the list of the first set of partners, which include Consensys, Fluency, Idemia, Consult Hyperion, Giesecke+Devrient, and Fireblocks. MasterCard says the partner program will explore central bank digital currency (OTC:CBDC) design, interoperability, and the advantages and limitations of CBDCs. Ripple has been the favorite blockchain network for pilot CBDC projects. In May, Ripple launched a blockchain network, powered by Ripple’s XRP Ledger (XRPL), dedicated to the development of stablecoins and CBDCs. The launch of this CBDC platform has caught the attention of central banks and has encouraged them to explore how they can use XRPL for their own CBDC projects. In July, the Pacific Island Nation of Palau started a pilot CBDC on the Ripple network. Banco de la República, Colombia’s central bank, has also tapped Ripple for its CBDC project pilot.

-

Real Estate Asset Tokenization in Hong Kong: The Hong Kong Monetary Authority (HKMA) initiated an e-HKD (its CBDC) pilot program in which Ripple is one of the 16 chosen pilot participants. Fubon Bank (another pilot participant) and Ripple are to examine the use of the e-HKD in the realm of residential mortgage loans, which make up a substantial portion of the local banking sector’s loan portfolio. The project revolves around the transformation of property title deeds into blockchain-based digital tokens, ensuring a singular and reliable source of information integrated into the loan approval process. Ripple’s involvement in the partnership centers on its expertise in blockchain technology, contributing to the creation of a seamless experience for potential homebuyers by enabling e-HKD loans to be accessible through both online and offline platforms within an e-wallet.

I expect Ripple to forge numerous new partnerships, integrations, and MoUs in the coming months, propelled by Judge Analisa Torres’ ruling affirming XRP’s non-security status in the long-drawn battle with the SEC.

Ripple’s Role in the Future of Payment

statista

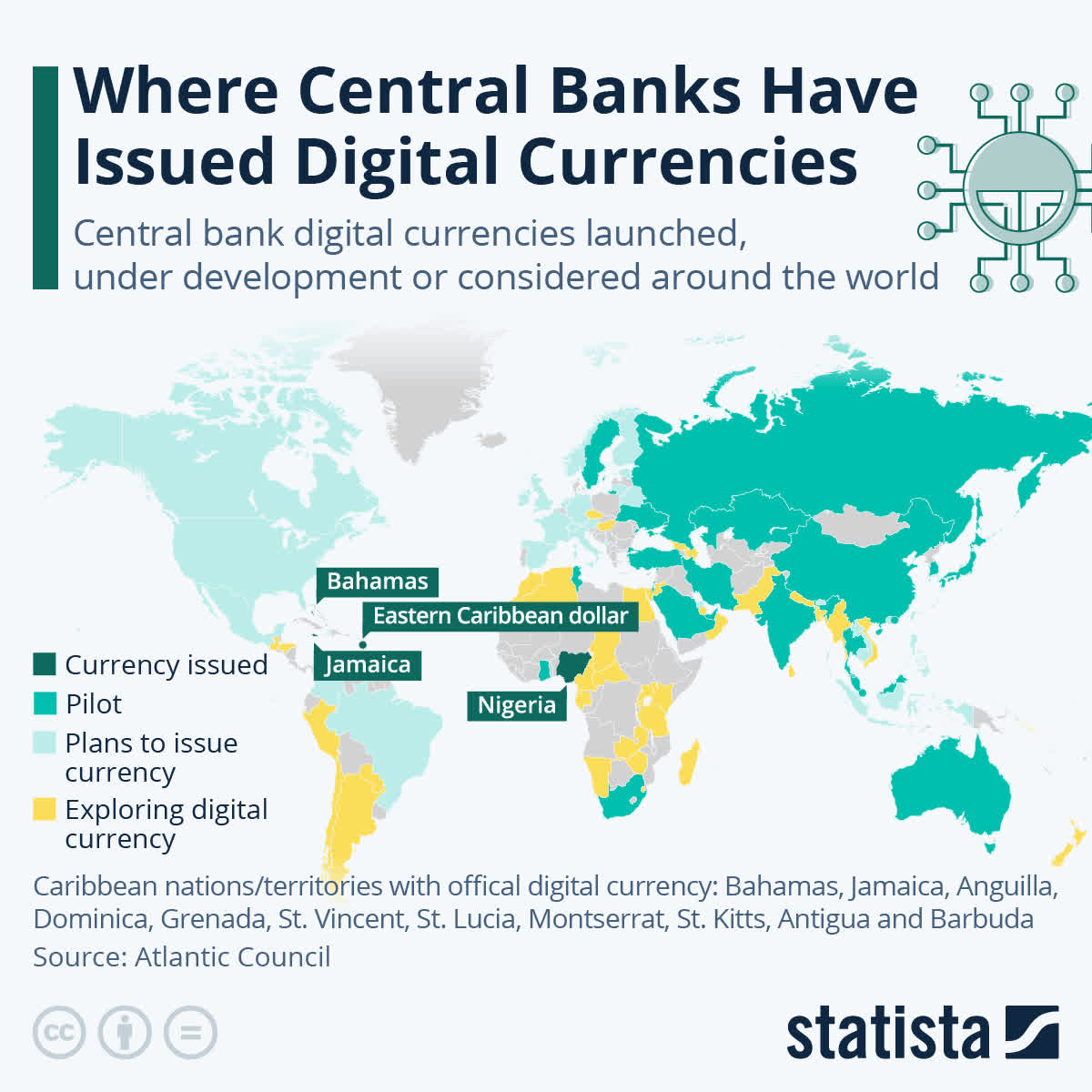

Central banks around the world are actively exploring the development of CBDCs. I believe that the current legacy payment rails are counting their last days and the introduction of a new global payment system is imminent. From the Bank of England to remote islands in the Caribbean, efforts to explore and create government-backed digital currencies are underway. Ripple, with its range of products, is strategically positioned to play a key role in these upcoming global payment innovations. Ripple’s On-Demand Liquidity (ODL), for example, which helps facilitate cross-border transfers without the need for pre-funding has been integrated by some payment providers, like the Malaysian-based cross-border payment hub Tranglo and the Japanese financial services provider SBI Remit.

Beyond offering a suite of payment-focused products that gives it a footing in the trillion-dollar cross-border payment market, Ripple actively seeks to make its technology and products compliant with industry and regulatory standards. This is evident in the fact that Ripple is one of the first enterprise blockchain networks to become ISO 20022 compliant. ISO 20022 is an emerging global standard for financial information and is set to become the international standard language for cross-border payments worldwide, and will allow richer and more data to be shared among financial institutions. Global payment network SWIFT has adopted the ISO 20022 standard. Ripple, alongside Stellar Lumens (XLM-USD), Quant (QNT-USD), Algorand (ALGO-USD), Hedera Hashgraph (HBAR-USD), IOTA (IOTA-USD), and the XDC Network are the crypto projects currently on the list of ISO 20022 complaint crypto projects.

Risk

Despite Ripple’s promising prospects for success and prominence in cross-border payments, there are still certain risks that have the potential to impede Ripple’s growth and journey toward achieving prominence.

Regulation

As witnessed in the long-lasting legal brawl with the SEC, regulatory constraints can severely limit the progress of Ripple. Though Ripple strives to be standard and regulatory-compliant in its product offerings, the ever-changing world of cryptocurrency means regulations can be hard to predict. New rules might come in the future that could adversely affect the operations of Ripple.

Emergence of Proprietary CBDC Networks

Some central banks are more interested in running their own private distributed ledger network (DLT) for their CBDCs. This poses a potential risk to Ripple’s adoption, as these central banks might prioritize their systems over utilizing another for cross-border payments. This scenario could limit Ripple’s market reach and slow down its efforts to establish a global standard for efficient cross-border transactions.

Competing Blockchain Networks

Although Ripple is highly focused on cross-border payment and has a network dedicated to the development of CBDCs, we have seen instances of central banks choosing to use other blockchain networks for their CBDC projects instead of Ripple’s much-touted CBDC platform. Norges Bank, Norway’s central bank, uses the Ethereum (ETH-USD) blockchain for its CBDC project. Another scenario arises where some central banks might decide not to implement blockchain technology for its CBDC but opt for a more centralized network infrastructure or another form of DLT; for instance, the Bank of England is exploring options for its CBDC and says it might not be built on a blockchain network, and the Bank of Italy chose Algorand as the blockchain network for its digital guarantees platform.

Uncertainty of Partnership Conversion

Many of Ripple’s heralded partnerships are based on MoUs, which are agreements that lack binding obligations. While central banks may initially pilot their CBDCs on the Ripple network, there is some possibility that they might opt not to proceed with building their official digital payment systems on Ripple after the pilot phase. This situation could potentially lead to challenges in translating successful pilots into long-term collaborations, impacting Ripple’s efforts to solidify its role in the evolution of digital payments infrastructure.

Conclusion

In conclusion, Ripple’s focus on cross-border payments shows big possibilities. Now that the long-awaited verdict of the non-security status of XRP has been delivered, this verdict creates an even more favorable playing field for Ripple to harness its expertise and gain prominence in cross-border global payment.

XRP price surged following the verdict in its case with the SEC, jumping by 75% and trading for around $0.82. XRP has, however, retraced to the $0.5 range – its “pre-verdict” price level. I don’t see any new catalysts to push up the price of XRP for now, therefore I wouldn’t recommend a buy. It is, however, worth a hold for investors who have XRP in their portfolio.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here