Rithm: Solid Recovery Over The Past Few Weeks

Rithm Capital Corp. (NYSE:RITM) investors have witnessed a solid recovery as RITM broke to a new recent high last week. As a result, investors experienced four consecutive weeks of recovery before selling pressure emerged this week. The leading mREIT has continued to diversify its business beyond its core MSR business. As a result, the company attempts to transition into other business segments that could improve its valuation multiples over time. Based on Rithm’s assessment, it anticipates a further valuation re-rating, suggesting the market has likely not priced in the prospects in its new growth vectors.

I last updated investors in a bullish RITM article in May 2024. I emphasized the growth prospects in its asset management business. Its timely decision to position against a more dovish Fed allowed it to capitalize on the recent market dynamics.

Rithm Diversifies Into Less Cyclical Segments

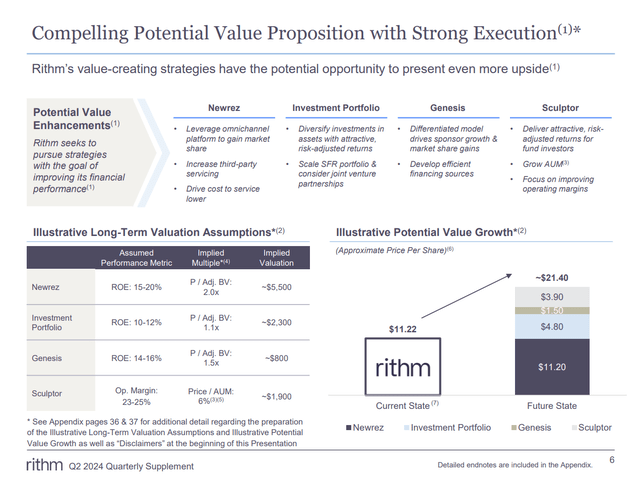

Rithm’s enhanced value proposition (Rithm filings)

Accordingly, Rithm has made notable progress in its business diversification, as seen above. Its decision to move further into Newrez’s omnichannel platform has strengthened its ability to gain more market share. Investors should note that Rithm has expanded its scale significantly. Accordingly, the mREIT underscores that it’s now the second-largest nonbank servicer and the fifth-largest lender in the industry. As a result, it’s expected to improve its ability to drive origination growth, supporting its core business further.

The Fed has also afforded more clarity on reducing interest rates from September 2024. As a result, the anticipated steepening of the yield curve should improve Rithm’s spread and costs of financing. In addition, rates are still expected to remain relatively high, potentially helping to curtail prepayment speeds (96% of its MSRs are in-the-money as of Q2). Hence, Rithm’s forward earnings available for distribution aren’t likely to be significantly impacted, even as it navigates a material shift in interest rate dynamics. As the mREIT expands its scale through its core lending business, it could lead to more robust growth if underlying demand remains strong.

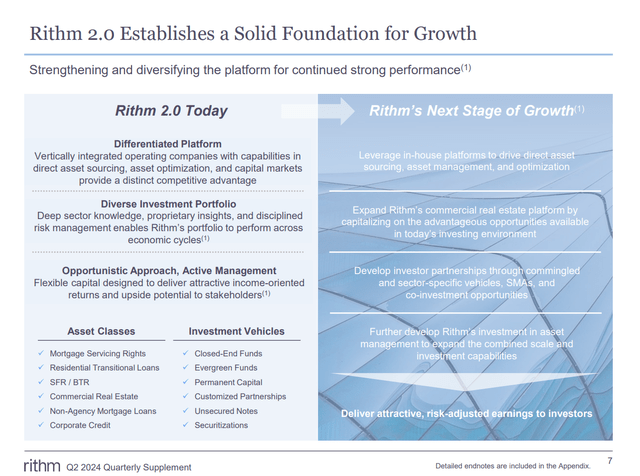

Rithm 2.0 business model (Rithm filings)

As a result, it should strengthen its bullish thesis in its transformation to its Rithm 2.0 business model unless macroeconomic conditions weaken significantly. Given the inherent cyclicality of its core mREIT business, I assess that the market will unlikely re-rate its valuation substantially in the near term. Therefore, Rithm’s ability to execute robustly in its new growth vectors will likely be scrutinized as it looks to “deliver attractive, risk-adjusted earnings to investors.”

I believe concerns about its execution in these opportunities are justified. The company could be extending itself too thinly even as it looks to gain a foothold in asset management. In addition, while expanding exposure in CRE and RTL seems like a more “natural” extension to its MSR business, they are also exposed to underlying real estate risks. As a result, it could temper Rithm’s diversification into asset management, impacting the market’s assessment of its valuation multiples.

RITM Stock: Still Relatively Attractive

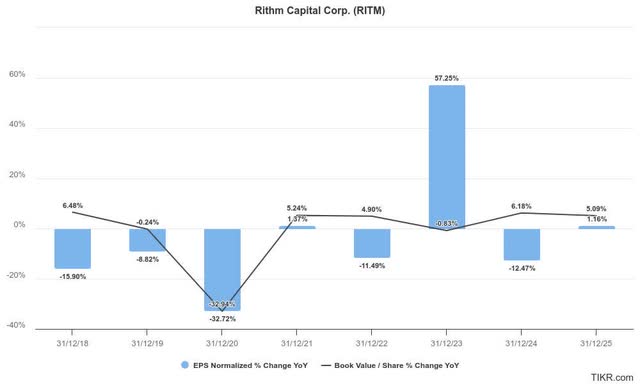

Rithm estimates (TIKR)

Rithm’s ability to diversify into less cyclical businesses will be critical to its forward EAD and book value per share metrics. As seen above, the cyclicality in its core MSR business affected its EAD markedly, leading to substantial volatility.

Despite that, the company remains confident that its diversification should spur a valuation re-rating as it demonstrates its ability to execute the growth drivers. Bolstered by a less hawkish Fed and a potential soft landing in the US economy, RITM income investors should remain vested, given its assessed undervaluation compared to its historical averages.

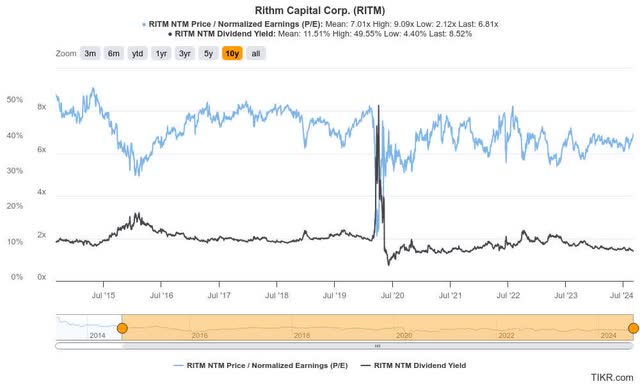

RITM forward valuation (TIKR)

RITM’s EAD multiple of 6.8x is still below its 10Y average of 7x. Its forward dividend yield of 8.5% is still markedly higher than the lowered 2Y (US2Y), which last printed at 3.76%. Therefore, I assess that the market has not significantly re-rated RITM’s business diversification, likely reflecting higher execution risks.

Is RITM Stock A Buy, Sell, Or Hold?

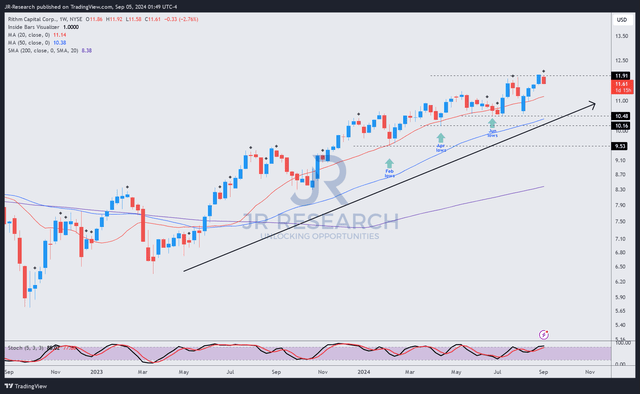

RITM price chart (weekly, medium-term, adjusted for dividends) (TradingView)

In addition, RITM’s price action (adjusted for dividends) corroborates my optimism that the market doesn’t think it’s due for a steeper pullback that could hurt its continuing uptrend thesis.

Dip-buyers have consistently defended its upward bias, demonstrating the market’s conviction in its ongoing recovery. While the market has likely baked in a more dovish Fed, its relatively attractive valuation and high dividend yields should lend credence to its bullish proposition.

I assessed that near-term consolidation could occur as it re-tests a critical resistance zone under the $12 level. However, it’s not expected to lead to a decisive reversal in its momentum, suggesting pullbacks could offer robust buying opportunities for income investors.

Rating: Maintain Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Consider this article as supplementing your required research. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing, unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here