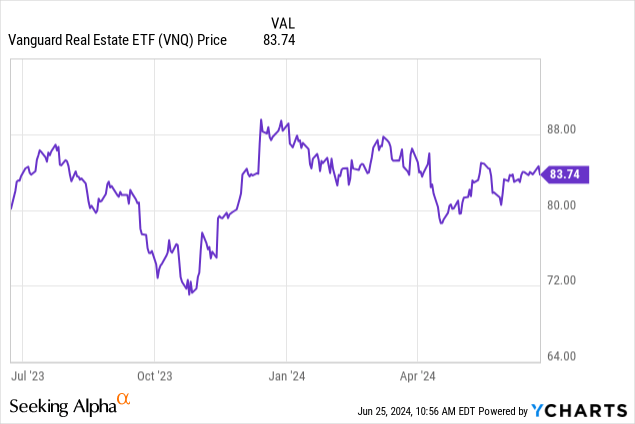

The REIT rebound is in full swing. At this time, rate cuts appear all but certain in the next six months. As optimism around rate cuts began to dwindle, investor fervor around the real estate sector faltered during the first half of the year. Following a powerful rebound in the fourth quarter of 2023, REITs and real estate (VNQ) were virtually flat through the first quarter. The second quarter started tempestuously as investors had their hopes dashed around potential rate cuts before the arrival of summer.

The June Federal Reserve meeting proved an inflection point in interest rate sentiment. REITs and similar income producing assets are directly impacted by movements in interest rates. At the June meeting, the Federal Reserve announced the decision to hold the federal funds rate steady as expected by most investors. The decision is unsurprising coming from a Federal Reserve who has repeatedly announced their intent to stick to an inflation-based rate policy.

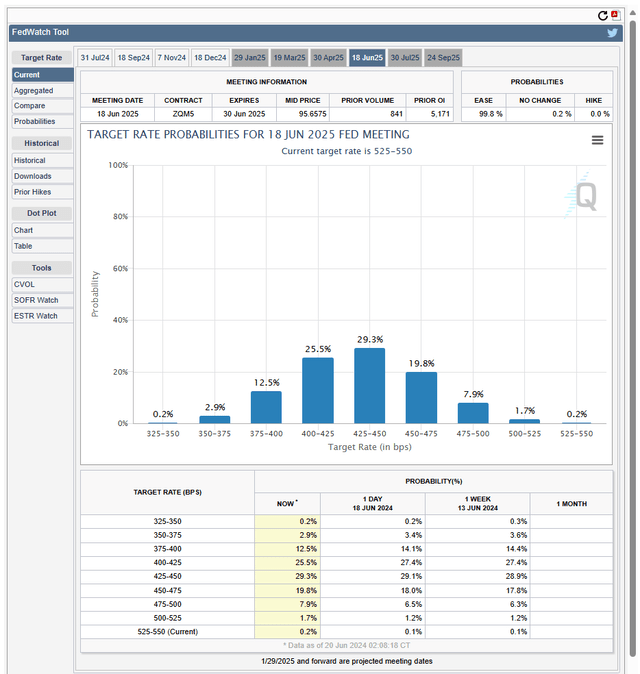

Investors are left gauging the likelihood of rate cuts coming by year end. A stark change compared to previous sentiment that rate cuts would assuredly arrive before Summer. Inflation remains above the Federal Reserve’s target rate meaning near term rate cuts were optimistic at best. Luckily, data shows significant improvement in the likelihood of rate cuts.

CME FedWatch provides forecasts for the federal funds target range over the next several years. The tool forecasts a 90% chance that rates will not change at the July meeting. However, odds improve as the year progresses. The data predicts a 95% chance that rates will come down by year end. The consensus arrived at a 50bps reduction to the target rate. Fast forward one year, the overwhelming odds point to lower borrowing costs. The likelihood of rates coming down over the next twelve months is nearly 100% according to the tool.

CME FedWatch

The data is significant for REIT investors who desperately need rate cuts to alleviate the difficult performance over the past several years. For REITs, declining interest rates work as a substantial tailwind, pushing performance for the sector at large. There are a variety of reasons for this including lower borrowing costs and declining valuation capitalization rates, both of which affect the fundamentals of the business. At the share level, REITs become more attractive on a relative basis as bond yields begin to drop. This means that REIT yields are likely to follow.

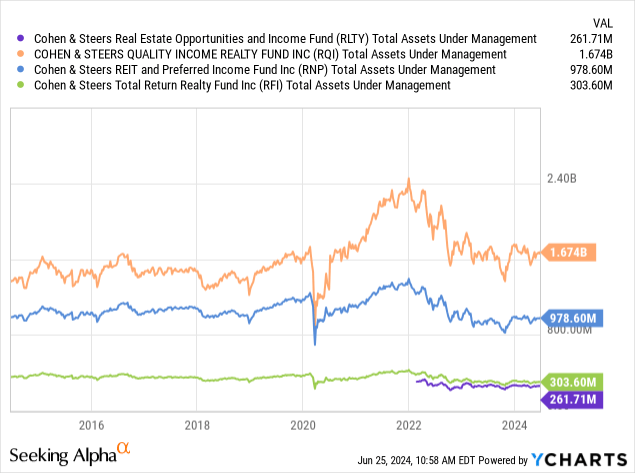

Cohen & Steers (CNS) is one of the largest managers of closed end funds. Focusing mostly on REITs and Infrastructure, CNS manages one of the largest and most successful platforms of REIT specific closed end funds. Their lineup is extensive, with four closed end funds focusing on REITs alone. Each of the funds is unique with subtle but impactful differences.

- Cohen & Steers Quality Income Realty Fund (RQI)

- Cohen & Steers REIT & Preferred Income Fund (RNP)

- Cohen & Steers Total Return Realty (RFI)

- Cohen & Steers Real Estate Opportunities and Income Fund (NYSE:RLTY)

Of the four funds in the lineup, three are leveraged. RFI is the oldest fund in the lineup and the only fund managed without leverage. Of the three leveraged funds from CNS, RQI and RNP are well established amassing billions under management over the course of decades. However, CNS launched RLTY in 2022.

Today, we will dive into RLTY for the first time. We will provide an overview and explore critical differences comparing the new fund against the existing lineup.

Fund Overview

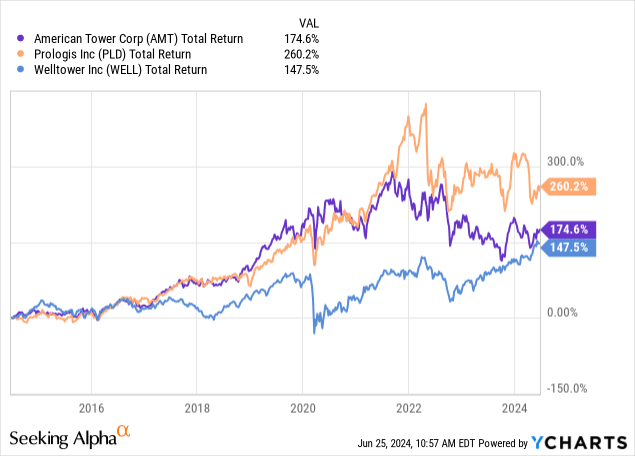

RLTY is an actively managed closed-end fund that invests predominately in high-quality REITs. Broadly speaking, the fund invests in large blue chip REITs including some of the largest landlords in the world. Like the other funds across the lineup, RLTY invests in REITs like American Tower Corporation (AMT), Prologis (PLD), and Welltower (WELL).

These three REITs accounted for more than 15% of RLTY’s portfolio as of March 31. Beneath the largest names, we’ll find a diverse portfolio of REIT equity with a smaller portion of the portfolio allocated to preferred stock and fixed income investments. In the top ten are two data center REITs, Digital Realty Trust (DLR) and Equinix (EQIX), showing RLTY is capitalizing on the AI gold rush. Additionally, RLTY invests in options.

Most of the portfolio is invested in the United States, however roughly 30% of assets are international. Of the international assets, most are in North America, including Canada and Mexico representing 21% of the portfolio. Europe and Asia receive the smallest portions at 9% and 1%, respectively.

RLTY is the newest fund in the CNS lineup. Accordingly, managed assets are considerably smaller than RQI and RNP, the largest funds from CNS. RLTY’s managed assets are more aligned with RFI, one of the smallest funds from the manager. The smaller fund presents a risk or possibility that it could be merged into a larger fund such as RQI. However, RLTY is new and growing with a unique value proposition, making this scenario unlikely.

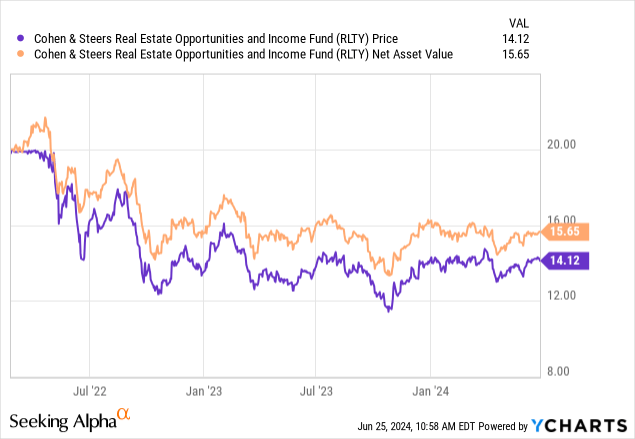

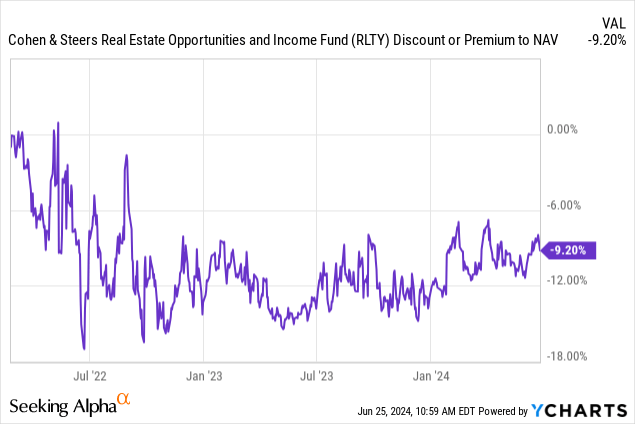

Since launch, RLTY has traded at a consistent discount to net asset value. Common shares of closed end funds trade independently of their net asset value or NAV. This means shares can diverge from their book value significantly. For some funds, share prices rise to a meaningful premium. However, for funds in struggling sectors, this often means a deep selloff below the value of underlying assets.

This generally comes as a negative impact, especially for new funds like RLTY. RLTY launched in 2022 at net asset value. Since, shares have declined as the fund’s NAV declined, however the damage has been exacerbated as the selloff went beyond the fund’s NAV.

For RLTY, this meant performance was worse than underlying assets, leaving new shareholders frustrated that the fund may have launched at the least opportune moment.

However, CNS’s management team came to the rescue with a share repurchase program. In September 2023, CNS announced that RLTY could repurchase up to 10% of outstanding shares during the next calendar year. CNS provided additional commentary on the program.

Cohen & Steers believes that the repurchase program will benefit shareholders as it enables the Fund to acquire its own shares at a favorable discount. In addition, the share repurchase program may benefit existing shareholders by reducing the discount to net asset value (“NAV”) at which the Fund’s shares are currently trading. The Fund’s portfolio managers intend to prudently manage the leverage levels of the Fund in concert with this activity.

Since the announcement of the program, RLTY’s discount to NAV has closed by around 50%, reaching the current discount to NAV of approximately 8%.

Dividend

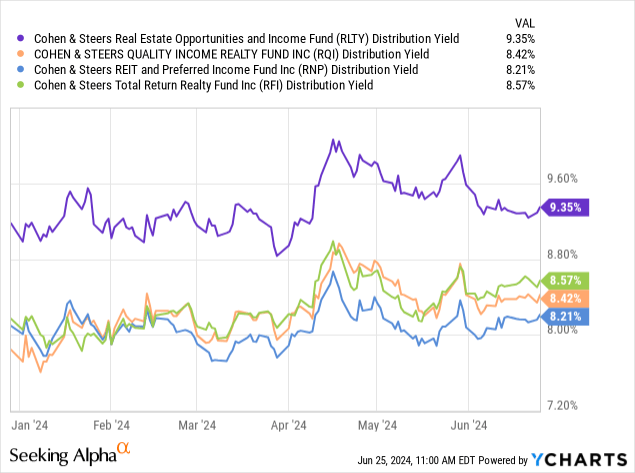

One of the most attractive aspects of RLTY and similar funds is the level of monthly distribution. RLTY and similar investments operate under a managed distribution policy. This means the fund distributes a level payment regardless of internal investment performance. This means the dividend can be sourced from income, capital gains, or the fund’s basis.

RLTY’s monthly dividend of $0.11 per share per month corresponds to a dividend yield of 9.24%. Given the fund’s larger discount to NAV, the yield is relatively high compared to other funds from CNS. One of the benefits of this distribution structure is predictable income. RLTY and similar funds feel like an ideal real estate investment, delivering cash flow rain or shine. This is attractive for investors seeking stable income such as retirees.

While RLTY is new, other funds from CNS have well established dividend histories. Over the past decade, the funds have maintained or increased their monthly dividend distributions.

Performance

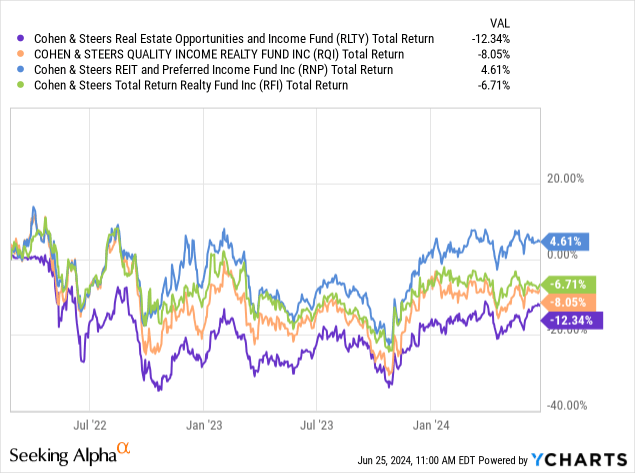

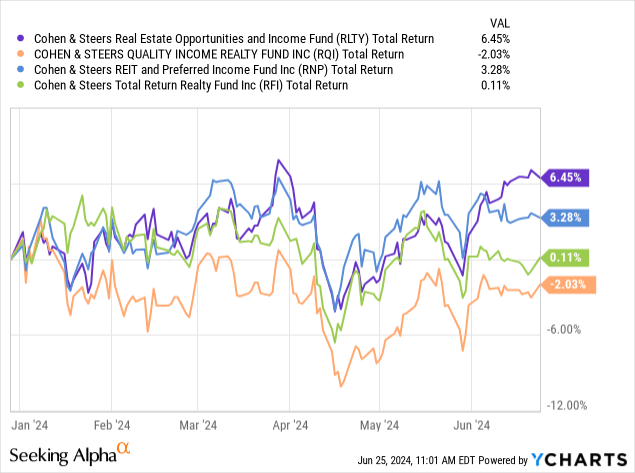

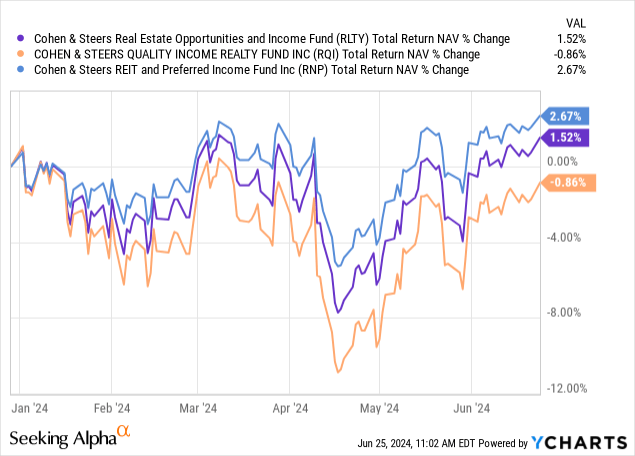

As the newest member of the lineup, RLTY has a limited performance history as compared to other members of the family. Since inception, RLTY has underperformed the lineup due to a combination of factors.

First and foremost, RLTY launched when borrowing costs had bottomed. As a result, these new funds were hit hardest as skeptical investors were quick to withdraw their money at the smell of trouble. For RLTY, this materialized as a dive to a discounted valuation faster than other funds within the lineup.

Unfortunately, this also means RLTY shareholders were left underperforming other funds. This largely changed with the announcement of RLTY’s share repurchase program. As an accretive turning point for the fund, the buybacks have served as a large driver of improved performance for RLTY. Over the past six months, RLTY’s relative performance has improved significantly compared to the other funds.

The Difference

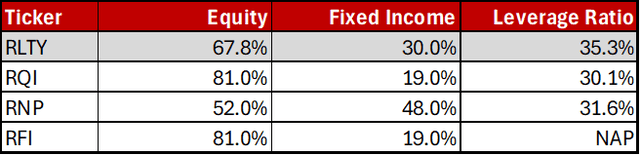

CNS manages four funds within their real estate specific lineup of closed end funds. The most significant differentiator is leverage. RQI, RNP, and RLTY, are leveraged, each with a leverage ratio between 30%-40% of assets. The funds use interest rate swaps to manage short term interest rate volatility. RFI is the only unlevered member of the family. The portfolio mirrors RQI in construction, so investors may find that an attractive point of comparison. Recently, we wrote an article covering RFI and why the lack of leverage has been a benefit over the past twelve months.

However, the difference between the three remaining funds is more subtle. From the surface, these funds are similar, investing mostly in high quality REITs with smaller portions invested in other income producing assets. Looking at the names of the funds is of little help, with a repeating word soup of “Quality”, “Income”, and “Realty.” Let’s open the hood of each fund and explore the key differentiating factors.

There are two primary differentiators between the three levered funds in the family. First, each fund has a different leverage ratio, which changes over time as the funds operate. Each fund is restricted by their ability to borrow, but generally floats in the range of 30%-40%. Second, the asset allocation between equity and fixed income is the most pronounced differentiator. Each fund is a combination of REIT common equity, REIT & non-REIT preferred equity, other fixed income, and derivatives. The derivatives are mostly covered call and cash secured put options. Note that CNS categorizes preferred stock as “fixed income” on their asset allocations.

Below is an illustrative table of each fund’s asset allocation and leverage ratio. Note that percentages do not add up to 100% due to rounding and cash/derivative holdings.

REITer’s Digest, Data from CNS

RLTY was launched as a fund designed to split the difference between RNP and RQI. Offering a blend of two thirds REIT equity and one third preferreds and fixed income, RLTY is a blend of two portfolios with a similar leverage ratio. This also explains why the performance of RLTY has been between RQI and RNP since inception.

Conclusion

RLTY is the newest fund amongst the lineup from CNS. With a portfolio that walks the line between RQI and RNP, RLTY delivers bottom line performance between the two funds. Combined with the share repurchase program from CNS, RLTY is poised to perform well against an accommodating macroeconomic backdrop.

As the likelihood of rate cuts continues to increase, RLTY and similar funds are positioned to perform well with supercharged portfolios of high quality assets. As we initiate coverage on RLTY, the fund earns a “Buy” rating with an attractive portfolio and proven management team.

Read the full article here