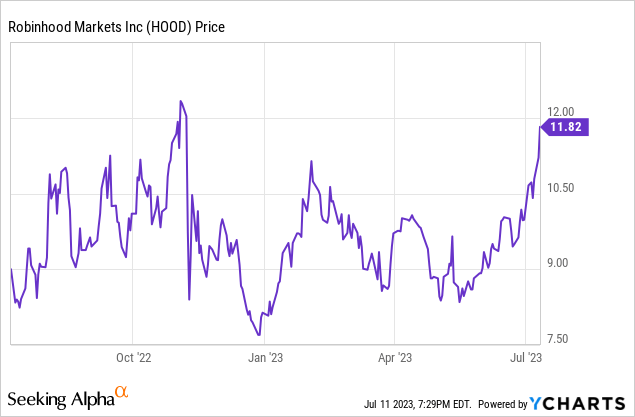

After initially being left out of the broader tech rally, Robinhood (NASDAQ:HOOD) has bounced strongly off lows. The rising interest rate environment initially wreaked havoc on the stock price, as a slowdown in crypto trading coincided with steep multiple compression. But HOOD has been a surprise beneficiary of rising interest rates as it has been able to substantially grow interest income, helping to boost its cash flow generation. HOOD still trades at reasonable valuations even before accounting for the large cash hoard. The price is right to bet on a successful turnaround, though of course the stakes remain high in the ever-competitive brokerage market.

HOOD Stock Price

HOOD had initially been one of the few laggards in the tech sector, but the last several months have seen the stock take off.

I last covered HOOD in April where I discussed the potentially over-exaggerated impact of canceling $500 million in RSUs but still rated the stock a buy on account of net cash making up 70% of the market cap. The stock is up double-digits since then and HOOD appears to be generating cash on a consistent basis. While the turnaround story is not yet fully in motion, the valuation remains cheap for those still looking to get onboard.

HOOD Stock Key Metrics

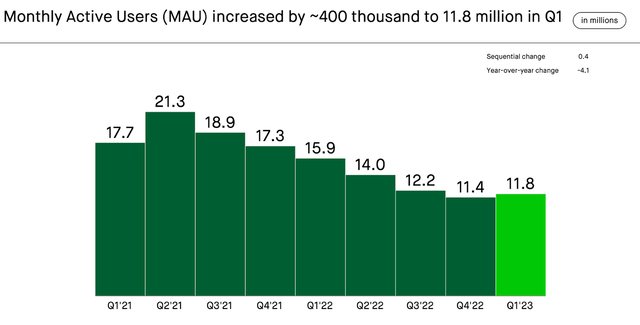

The most important metric in my view of the latest quarter was that of monthly active users (‘MAUs’), which saw its first quarter with sequential growth since 2021. Sure, MAUs have declined by nearly half sense then, but this is a potential sign that stabilization is near.

2023 Q1 Presentation

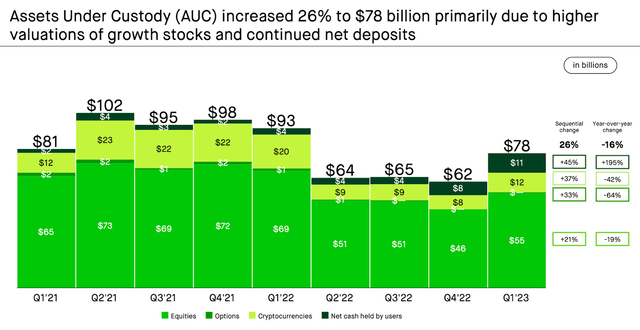

HOOD also saw assets under custody grow due to both a recovery in asset valuations as well as growth in net deposits. During a period in which many regional banks are seeing unprecedented risk due to “cash sorting,” HOOD is one of the beneficiaries of such times given that it has historically competed aggressively on deposit rates.

2023 Q1 Presentation

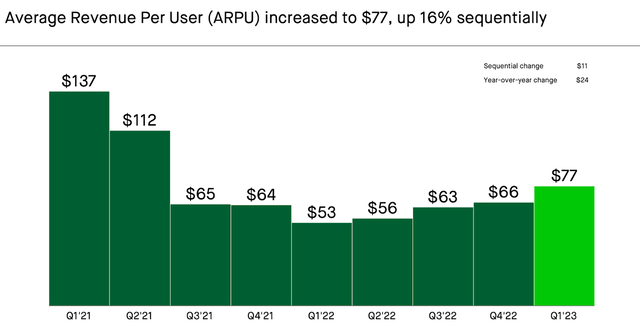

HOOD also saw continued strength in average revenue per user (‘ARPU’). I have previously highlighted the stabilizing ARPU as a sign that the bottom was near, and that looks to be vindicated given the ongoing recovery as well as the aforementioned sequential growth in MAUs.

2023 Q1 Presentation

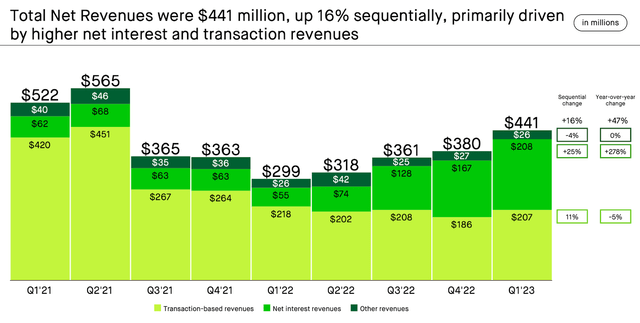

Those factors helped lead to stabilization in transaction-based revenues on a YOY basis, a development which was overshadowed by the stunning growth in net interest revenues.

2023 Q1 Presentation

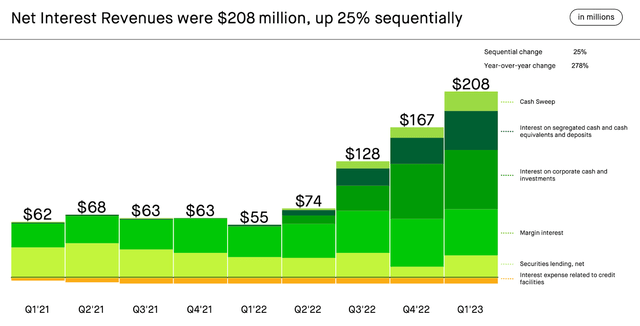

Just highlighting that last point, HOOD has benefitted handsomely from the rising interest rate environment, with net interest revenues quadrupling over the past 12 months.

2023 Q1 Presentation

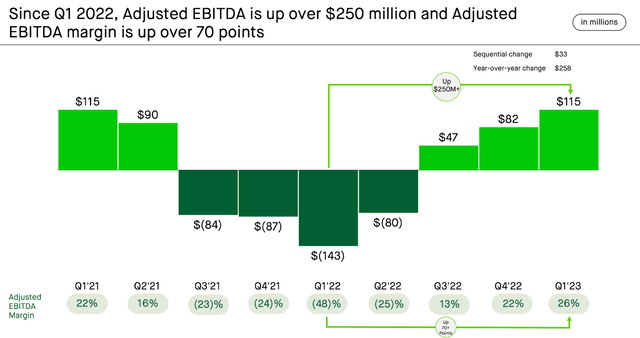

It is ironic that while the higher interest rate environment was arguably a significant catalyst in causing the multiple compression seen in the stock price, it also has helped HOOD return to adjusted EBITDA profitability. It should be noted that adjusted EBITDA does include interest earned from cash on the balance sheet.

2023 Q1 Presentation

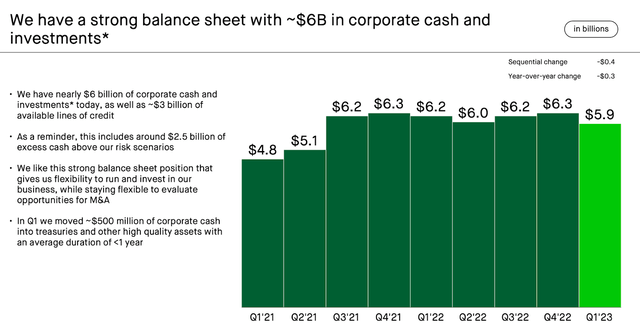

HOOD ended the quarter with nearly $6 billion in cash versus no corporate debt. The fact that the stock price is still 80% below all time highs may imply a high degree of risk, but the reality is that this is a cash flowing name with a sizable cash hoard. Management notes that their cash hoard represents an excess of $2.5 billion above their risk scenarios.

2023 Q1 Presentation

That net cash is very significant considering that the stock recently traded hands at around a $10 billion market cap.

Looking forward, HOOD has guided for net interest revenues to grow sequentially by about $15 million, and reduced guidance for full-year expenses by $30 million to $2.485 billion at the high end.

On the conference call, management appeared to show a strong commitment to cost rationalization, reiterating their commitment to “becoming profitable on a GAAP basis.” Again, it bears repeating that investors must be careful to avoid viewing this stock as the same cash guzzling, meme-driven name that it was during the pandemic – valuations have been reset and it is now all about the cash. Management continues to expect to purchase “most or all” of the 55 million shares owned by Emergent Fidelity Technologies following the fall out of Sam Bankman-Fried. I wouldn’t mind a small share repurchase given the valuation and large cash hoard.

Some readers might find it potentially troubling that management gave indications for a preference to use its cash for M&A, with the CEO stating “my mind goes to the M&A front when I think about use of capital,” but noting that the private markets have been slower to correct in terms of valuations. That commentary means that investors should be careful in accounting for net cash in calculations of valuation as there is some likelihood that the company may end up using the cash for acquisitions, which may or may not be accretive for shareholders.

Is HOOD Stock A Buy, Sell, or Hold?

Despite the great turmoil of recent years, HOOD is arguably still one of the more innovative brokerage firms in the market today. HOOD has come a long way from just being known as the only brokerage firm offering commission-free trades.

2023 Q1 Presentation

Its most recent innovations include enabling 24-hour individual stock trading on select stocks as well as offering up to $2 million in FDIC insurance starting in June. Unlike traditional banks which have historically offered little to no interest on deposits, HOOD offers one of the more competitive yields in the market with a 4.65% yield for its Gold members. Moving forward, management is excited about rolling out a personal advisory service to the masses, utilizing artificial intelligence to make the fees lower than the typical 1% annual fee.

As of recent prices, HOOD was trading at just 5.5x sales.

Seeking Alpha

Based on a return to 20% forward growth, my estimate for 30% long term net margins, and a 1.5x price to earnings growth ratio (‘PEG ratio’) I could see shares trading at around 9x sales, implying substantial upside even before factoring in the net cash on the balance sheet worth 60% of the market cap. In my view, there are certain binary outcome characteristics at play here, as one can make the argument that HOOD either returns to being a secular growth story growing at a 20+% rate or returns to bleeding users in what has historically been a commoditized market.

What are the key risks? A big issue is that brokerage services are arguably commoditized services. At the end of the day, I struggle to believe that consumers will not just seek the lowest cost provider, though HOOD has differentiated itself through its technology and attractive user interface, and one can make an argument that switching costs may delay the negative effects of price competition. Yet just as many brokerage firms moved to eliminate commission fees in response to Robinhood, I expect many competitors to also uptake the numerous “innovations” that HOOD is rolling out. The “first mover advantage” might not be so important here given how easy it is to transfer assets in this digital age. Ironically a big risk may be declining interest rates as that may lead to a reversal of the gains in net interest income as well as an exit of users to other more trusted brokerage competitors. It is not easy to determine if HOOD can continue growing MAUs in spite of the sequential growth shown in this past quarter, we may need to see several quarters before we can make such a judgment. I am of the view that HOOD continues to prioritize innovation and is differentiating itself from legacy peers among millennial investors, a secular trend which may accelerate over time. While I admit that we may be early here, the valuation is undemanding to wait for further progress on the turnaround – I reiterate my buy rating.

Read the full article here