We previously covered SoundHound AI, Inc. (NASDAQ:SOUN) in March 2024, discussing the sudden rise in its stock prices then, thanks to Nvidia’s (NVDA) stake disclosure and the growing demand for voice AI technology with Large-Language Model integration as a proprietary SaaS in both cloud-native and hardware-embedded platforms.

However, with the company still unprofitable with deteriorating balance sheet and the stock massively shorted, we believed that there might be near-term volatility, triggering our Hold (Neutral) rating then.

Since then, SOUN has already pulled back drastically by -52% since the March 2024 peaks, well underperforming the wider market. Even so, we are not certain if it will be wise to recommend a Buy here, with the stock still trading at a notable premium compared to its generative AI SaaS peers.

Combined with its nascent start-up stage, penchant for equity dilution, and impacted FQ1’24 profit margins from the recent acquisition, we believe that it may be more prudent to wait and observe its execution for a little longer.

SOUN Continues To Report Robust SaaS Growth

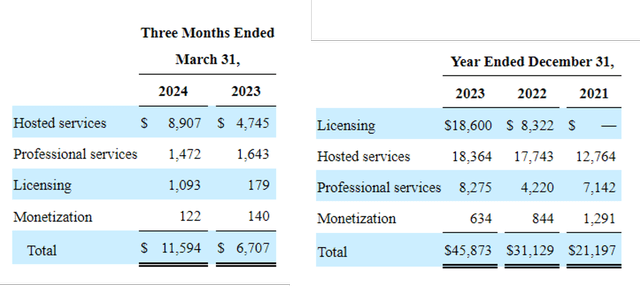

SOUN’s Revenue Segment

Seeking Alpha

For now, SOUN has reported a double beat FQ1’24 earnings call in May 09, 2024, with revenues of $11.59M (-32.4% QoQ/ +72.9% YoY) and adj EPS of -$0.07 (inline QoQ/ +46.1% YoY).

Much of its top-line tailwinds are attributed to the accelerating growth observed in the Hosted Services segment to $8.9M (+58.6% QoQ/ +87.7% YoY), attributed to the revenue recognition from either per usage and/ or fixed fee subscriptions, further highlighting the stickiness of its voice AI SaaS platform.

However, despite the robust growth in SOUN’s top-line, readers must also note that its gross profit margins underwhelm at 65.5% (-11.5 points QoQ/ -6.8 YoY), along with its adj EBITDA margins at -132% (-111 points QoQ/ -90 YoY) in the latest quarter.

Much of the bottom-line headwinds are attributed to the lower margin call center agent business, thanks to the recent completed SYNQ3 Restaurant Solutions acquisition.

Even, so we believe that things may improve in the intermediate term, given the accretive impact on SOUN’s automated voice AI technology solutions and the diversification into the restaurant (including customer service/ drive through) and fitness businesses.

This builds upon the SaaS company’s existing presence in the automotive, broadcasting, and telecommunication platforms across TVs, smart devices, and IoT devices.

And this is why SOUN has reported an excellent expansion in its multi-year cumulative subscriptions and bookings backlog to $682M (+3.1% QoQ/ +80% YoY) in the latest quarter, providing insights into its long-term top/ bottom lines.

This is on top of the moderately raised FY2024 revenue guidance from the original midpoint of $70M (+52.5% YoY) to $71M (+54.6% YoY).

Unfortunately, here is where the good news end.

SOUN’s High Customer Concentration Poses Risk To Its Future Prospects – Readers To Monitor

After a closer inspection, it is apparent that two core customers (highlighted as A and C) accounts for 48% of SOUN’s FQ1’24 revenues (+12 points YoY), with the high customer concentration being highly risky in the event of non-contract renewal in an intensifying market competition and/ or margin dilution in the event of preferential contract rates.

While the recent capital raise worth $137M has contributed to the improvement in its balance sheet with a cash/ equivalents of $211.74M (+122.2% QoQ/ +357% YoY), it has naturally resulted in the growing share count to 286.59M (+13.37M QoQ/ +81.51M YoY), partly also attributed to the new stocks issued for the SYNQ3 acquisition.

The erosion in SOUN’s shareholder equity has played out as discussed in our previous article with more dilution likely in the intermediate term, due to the inherent lack of positive Free Cash Flow thus far, with -$22.05M reported in the latest quarter (-58.2% QoQ/ -51.4% YoY).

At the same time, its stock-based compensation expenses have also risen drastically to $6.97M (+7.5% QoQ/ +16.3% YoY), as insiders continue to unlock $2.6M of gains in Q1’24 (+432% QoQ/ +253% YoY).

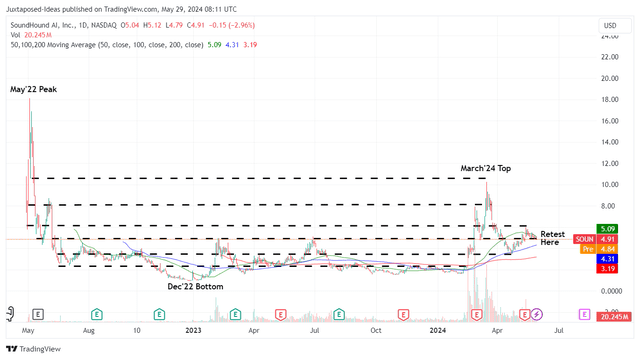

So, Is SOUN Stock A Buy, Sell, or Hold?

SOUN 2Y Stock Price

Trading View

For now, SOUN has returned most of its gains after the recent FQ1’24 earnings call, with the stock appearing to retest its previous support levels of $4.90s.

Even so, we are not certain if it is wise to add here.

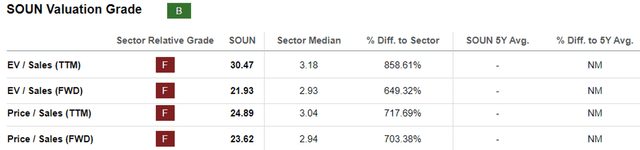

SOUN Valuations

Seeking Alpha

With SOUN still firmly in the cash-burn startup stage with negative EPS expected through FY2025, the only few metrics we may use to value the stock is the FWD EV/ Sales of 21.93x, which is notably expensive compared to the 2023 mean of 10.62x and the sector median of 2.93x.

This is especially since the SaaS company needs to consistently report high double digit growths over the next few years to warrant the premium EV/ Sales valuation.

Even if we are to compare SOUN’s valuations to other generative AI SaaS stocks, such as C3.ai (AI) at FWD EV/ Sales of 7.21x, BigBear.ai Holdings, Inc. (BBAI) at 2.61x, and Palantir (PLTR) at 16.05x, it is apparent that SOUN is overstretched here, offering interested investors with a minimal margin of safety.

At the same time, SOUN continues to record elevated short interest of 23.9%, higher than the previous levels of 14.6% in March 2024, implying further volatility in the near-term.

Moving forward, anyone still holding here should also remain (extremely) patient, since it remains to be seen when the company may achieve operating profitability and whether the stock may be well supported at current levels.

With more uncertainty ahead, it goes without saying that the stock is only suitable for those with higher risk tolerance.

Reiterate Hold (Neutral) here.

Read the full article here