Investment overview

I give a buy rating for Rollins, Inc. (NYSE:ROL) as the organic growth outlook is very positive and is higher than pre-covid levels. This, along with cost savings initiatives, pave the way for ROL to continue expanding adj EBITDA margins at 50bps/year. Given this performance outlook, I expect forward EBITDA multiples to trade up to 30x.

Business description

ROL is a leading provider of pest control services with a variety of leading brands, most notably Orkin. The company provides essential pest and wildlife control services and protection against termite damage, rodents, and insects to residential and commercial customers. The primary business units (segments) are Residential (46% of FY23 revenue); Commercial (33%); Termite & Ancillary Services (20%) (the remaining 1% is from franchises and others). Breaking down revenue by geography, ~93% is from the United States.

2Q24 earnings (announced on 24th July 2024)

ROL reported total 2Q24 revenue of $891.9 million. This was 8.7% y/y growth that fell below the streets’ expectation of 9.1%. Putting aside relative performance, organically, ROL did accelerate revenue growth by 20bps from 7.5% in 1Q24 to 7.7% in 2Q24. By segments, Residential grew 6.3% y/y on a reported basis and 5.4% organically; Commercial grew 9.9% reportedly and 8.6% organically; Termite & ancillary [TNA] grew 11.8% reportedly and 11.1% organically. The business saw an EBITDA margin expansion of 140 bps y/y to 23.6%, coming above street’s expectation of 22.9%. Combined, adj. EPS of $2.07 came in above consensus estimates of $0.26.

HSD organic growth is doable

The acceleration in organic growth seen in 2Q24 was driven by various strategies that, I believe, can support high-single-digit organic growth ahead. To be specific, ROL saw success with its revised go-to-market [GTM] strategy, where it expanded its commercial sales force, adopted a door-to-door sales strategy, and increased cross-selling of newer ancillary products with existing customers. I particularly like the door-to-door sales strategy, as it widens ROL reach and increases the number of customer touchpoints (which helps in cross-selling new products).

Strong organic growth trends in the commercial segment also make high-single-digit organic growth plausible. I see this organic growth strength as sustainable, given that the strategy to separate commercial from Orkin residential and commercial branches is showing positive results (historical has done well when ROL implemented such separation). The idea was that separating them apart would enable ROL to better allocate sales resources (i.e., where to increase sales) and allow for better leadership focus and penetration of targeted verticals. This makes absolute sense because of the different customer bases (commercial and residential), which require different GTM strategies, pricing, and services. Seeing that organic growth continues to trend in high single-digits (8.6%) vs. pre-covid of low-to-mid single-digits, this strategy is clearly working.

As such, I believe this will support the outlook for high-single-digit organic growth vs. pre-covid levels of mid-single-digit organic growth.

If we can separate these branches, make them smaller, we oftentimes see more robust growth. So, we’re following a consistent approach with the commercial business, and we’re seeing good results. 2024 Wells Fargo Industrials Conference

Lastly, ROL continues to be able to command strong pricing power. Recall that in FY23, management raised prices by 3-4% and noted it was going to raise prices in 1Q24 at a similar rate to FY23. In the latest call, management noted they continued to “execute their pricing strategy,” which suggests that price increases continue to trend in the 3-4% range. This is a step up from the low single-digit percentage increase seen during pre-covid. This tells me that ROL services are providing a strong value proposition to consumers, as they are willing to pay for more (despite the current macro environment).

So as we had talked about previously, Jason, we had passed along a 3% to 4% price increase in the prior year. We followed that on again this year with a similar price increase here in the first quarter ahead of our heavier pest market season which starts here later in the first quarter. So we’re pretty — in terms of what we’re seeing on the customer side, we monitor that, we assess that, we look at churn, we look at cancellations, we look at rollbacks, we look at a number of different metrics, and we feel like the level that we’re passing along is at a very healthy level and is representative of the value of our services. Company 4Q23 earnings

So retention definitely a positive for us. We continue to add new customers and our pricing has probably stayed relatively intact with what we’ve seen in previous quarters somewhere between that 1% and 2% range. Company 3Q18 earnings

With organic growth expected to trend in the high single-digits, reported growth could come close to 10% for the foreseeable future. The growth contribution from M&A was 100bps in 2Q24, and management expects the full-year contribution to be 200bps. Given that ROL’s balance sheet remains extremely solid (0.3x leverage ratio), the constraint to M&A-led growth is the number of deals. This doesn’t seem to be a problem, as ROL continues to have a robust acquisition pipeline.

Path to more margin expansion

Margin performance was fabulous in the quarter as ROL continues to achieve operating efficiencies. The 140 bps y/y increase in EBITDA margin was attributed to continuous improvement initiatives and tech modernization efforts. These efforts included optimizing procurement through scale and vendor relationships, investing in platform technology, and centralizing back-office services. Looking ahead, as ROL continues to print high-single-digit organic growth and with 1-year adj EBITDA incremental margin trending at ~30% in 2Q24, I expect ROL to continue expanding margins like it did over the past few years (~50bps/year since FY20 to FY23).

Incremental EBITDA margins were over 30% for the first half of the year and approached 40% in the second quarter, ahead of the metrics we discussed in our recent Investor Day, driven by strong leverage throughout the P&L. Company 2Q24 earnings

Valuation

May Investing Ideas

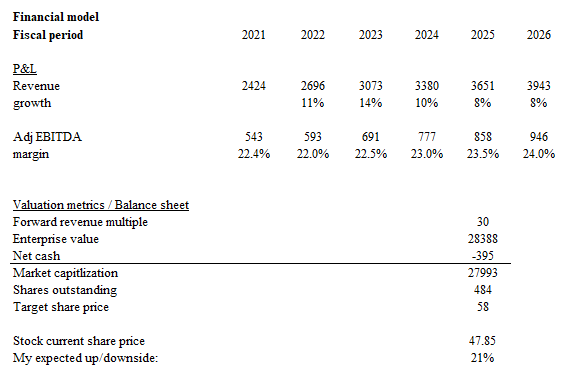

Based on my research and analysis, my expected target price for ROL is $58.

- Revenue should grow 10% in FY24 (8% organic + 200 bps M&A contribution), followed by 8% for FY25/26 assuming no M&A contribution (hence, there is upside potential here).

- EBITDA should reach $946 million in FY26 as the margin expands by 50bps a year from FY23.

- Stock should minimally trade at 30x forward EBITDA multiple, the past 5-year average, as organic growth is higher than pre-covid levels and the outlook for margin expansion is much clearer (given the cost savings achieved and better growth).

Risk

I think the risk lies in whether ROL can continue to sustain that 3-4% price increase when wage inflation starts to ease as the macroeconomy gets better. The current narrative is that ROL improved service has enabled it to sustain that higher price increase vs. pre-covid levels, but if that turns out to be false and pricing reverts back to low single-digit levels, organic growth may not sustain at high single-digit levels. This will cause consensus to revise their estimates downward (growth expectations for FY25/26/27 are 8.2%, 7.4%, and 8.4%).

Conclusion

I give a buy rating for ROL as I am positive about the strong organic growth and EBITDA margins expansion outlook. Organic growth should be well supported by ROL’s revised go-to-market strategies, commercial segment separation, and pricing power. As for EBITDA margins, high incremental margins coupled with ongoing efficiency gains should make 50bps/year expansion very possible.

Read the full article here