Investment Thesis

Roper Technologies, Inc. (NASDAQ:ROP) is well-positioned to deliver good growth moving forward. The company’s revenue growth should benefit from the company’s focus on consistently developing offerings in the generative AI space to capitalize on secular demand trends from emerging generative AI adoption. In addition, the company’s revenue growth should also benefit from strength within the company’s water end-markets due to a high backlog and pent-up demand for water management products. Further, the company’s diversified portfolio and its bolt-on M&A strategy should also contribute to revenue growth in the years ahead.

On the margin front, the company should benefit from AI monetization, high-margin M&As, good cost synergies from acquisitions, and cost-saving initiatives. In terms of valuation, while the stock is trading in line with historical averages, I see upside and a potential for re-rating given the company’s AI exposure. When I last covered the stock, I liked the company’s growth prospects but I rated it neutral as the valuation was in line with historical levels. However, with generative AI applications continuing to gain traction, most of the industrial stocks linked to this theme have re-rated higher than their historical averages. There is a potential for ROP stock to see a similar re-rating. Hence I am upgrading it to a buy.

Roper’s Revenue Analysis and Outlook

In my previous article, I discussed the company’s good track record of growth and expected further growth driven by exposure to secular demand trends, a strong base of recurring revenue, and a bolt-on M&A strategy. The company has posted strong growth since then.

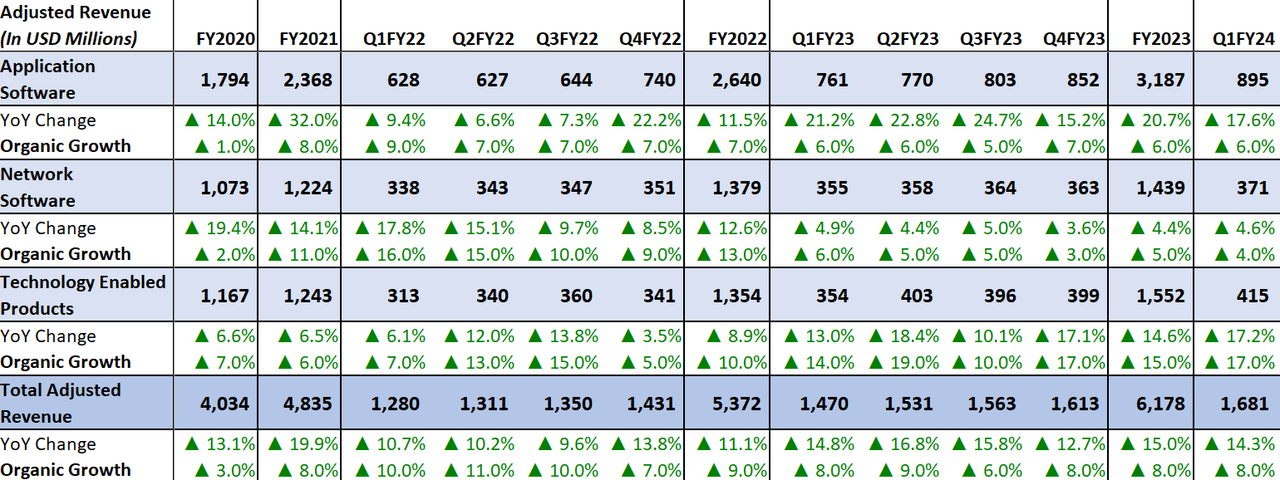

In the first quarter of 2024, the company’s revenue growth continued to benefit from good growth of 15.8% Y/Y from recurring software revenue as well as a good customer retention rate driven by increasing traction towards generative AI software products and services. In addition, the company’s revenue also benefited from healthy demand in the water and healthcare end markets. Revenue growth was further fueled by inorganic contributions from bolt-on M&As. This resulted in a 14.3% Y/Y growth in revenue to $1.68 billion. Excluding a 6 percentage point benefit from acquisitions, organic growth increased by 8% Y/Y.

On a segment basis, the Application Software segment delivered 17.6% Y/Y revenue growth benefiting from Syntellis and Procare acquisitions growth. In addition, high customer retention and increasing recurring revenue due to good demand for generative AI software also supported revenue growth. Excluding the benefit from acquisitions, organic growth increased 6% Y/Y for this segment. In the Network Software segment, the company delivered 4% organic growth benefiting from good demand within alternate site healthcare, insurance, and financial service sectors. This was partially offset by a weak freight market and actors strike within the entertainment sector. Lastly, the Technology Enabled Products segment delivered a 17% Y/Y organic growth due to healthy demand for ultrasonic meters and the adoption of meter data management software as well as good demand in the healthcare end markets.

ROP’s Historical Revenue (Company Data, GS Analytics Research)

Looking forward, I believe the company should continue to deliver sales growth benefiting from secular demand trends from emerging generative AI adoption, pent-up demand for water management products, and bolt-on M&A strategy.

In recent years, the demand for Artificial Intelligence (‘AI’) and Generative AI has seen a continuous rise. This is driven by industries looking for ways to improve their productivity and profitability due to persistent inflation and changes in working culture, and hence upgrading their digital infrastructure with AI automation and generative AI solutions. The company has taken good steps to position itself to benefit from this secular trend. Last year, Roper started developing generative AI-equipped software tools to help its customers with their productivity improvement needs. Before Q2 2023 the company hardly had offerings in the generative AI space. However, since Q2 2023 the company has launched various tools equipped with generative AI and many of its leading businesses now have multiple softwares offering generative AI solutions which are gaining good traction from customers as well as helping in increasing the value of its products. This is supporting the company’s recurring revenue base and improving customer retention.

The company is focused on further developing new and custom software that meets the increasing needs of its customers within the generative AI space to fulfill their productivity requirements. This should continue to help the company to capitalize on emerging AI trends. The company is still in the early stages of rolling out and monetizing its AI offerings. As the monetization of these offerings improves in the coming years, it can meaningfully add to the company’s medium to long-term growth. On the first quarter 2024 earnings call, while addressing a question on generative AI strategy, CEO Neil Hunn commented,

As it relates more directly to your question around products and the market and monetization. This is going to be a slow and steady race about how do you use these tools to create incremental value for our customers. Again, you know we compete on intimacy. That intimacy leads us to know very specific problems and very specific questions that need to be addressed. We have a new technology set to be able to do that. Companies that have products in the market today using GenAI, Aderant, Deltek, DAT, ConstructConnect and Foundry by our account, there may be a few others. Two quarters ago, I think that the count was 0. And so we like the momentum in that regard. In terms of monetization, it’s still early days. Our belief — like for the moment at least, we’re monetizing the GenAI investments by having — by adding that toolset and capability to our existing products in unique ways and then that is creating more value in the products, which is driving in almost all cases, bookings acceleration with those products, and in some cases, higher price points because of the value that’s achieved through the tools.”

Overall, I expect AI to be a big growth driver for the company in the coming years.

In addition to good demand for its software solutions, the company’s Technology Enabled Product segment is also poised to support the company’s organic revenue moving forward. The strength in this segment is led by its Neptune business, which offers meters used to measure water usage. The business has a high level of backlog fueled by unfulfilled orders and pent-up demand. During the pandemic, the company saw delays in water maintenance work as many meters were inside the customers’ homes which stalled the maintenance work as workers were not allowed within their homes. This created pent-up demand for water maintenance meters and increased Neptune’s backlog as soon as the pandemic situation improved. According to management, this 1 to 1.5-year slow maintenance schedule is leading to 5 or 5.5 years of demand squeezed into 4 years and they expect this dynamic to play well into the coming year as well. The company is also launching new water meters equipped with advanced technologies which is also gaining traction among customers and should continue to support the organic growth along with high backlog levels.

Lastly, the company also has a good track record of growing revenue through bolt-on M&As, acquiring businesses having leadership positions in their respective markets. This M&A strategy helped the company add 7 percentage points of sales growth inorganically for the full year 2023 and 6 percentage points in the first quarter of 2024. The company acquired Syntellis in August 2023 which is a top provider of cloud-based performance management software and data solutions related to healthcare, financial institutions, and higher education sectors. This acquisition is expected to contribute $185 million in FY24. Further in Q1 2024, the company completed the acquisition of Procare, a top provider of cloud-based software used in managing early childhood education centers. This acquisition is expected to contribute ~$260 million in revenue for the 12 months ending March 31st, 2025. The company plans to remain active in 2024 on the M&A front, which bodes well for the overall revenue growth. At a recent Jefferies Software Conference, CFO Janson Conley highlighted the company’s $2 billion FCF generation potential this year which combined with a reasonable 2.9x leverage, gives it ample firepower for M&As over the next 12 months.

So, I expect the company to continue to benefit from both organic and inorganic growth and I remain optimistic about Roper’s revenue growth prospects ahead.

Roper’s Margin Analysis and Outlook

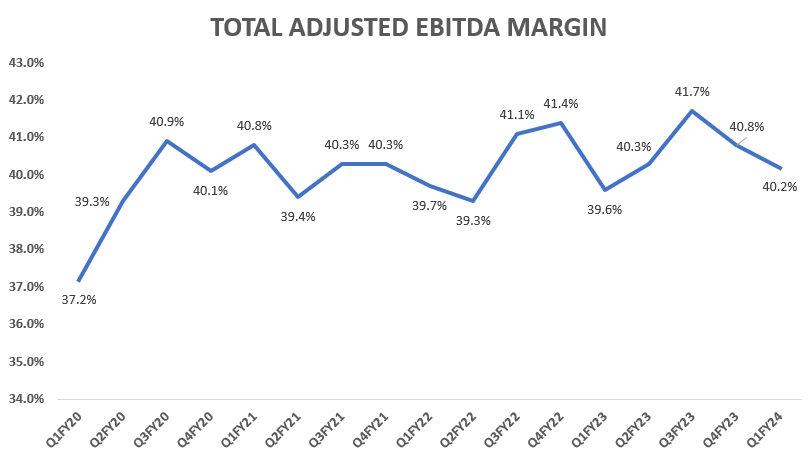

In the first quarter of 2024, the company’s margins benefited from an increasing high-margin business mix, good operating leverage, acquisition synergies, lower SG&A as a percentage of sales as compared to the previous year’s quarter, and cost-saving measures. This resulted in a 60 bps YoY increase in total adjusted EBITDA margin to 40.2%.

ROP’s Historical Total Adjusted EBITDA Margin (Company Data, GS Analytics Research)

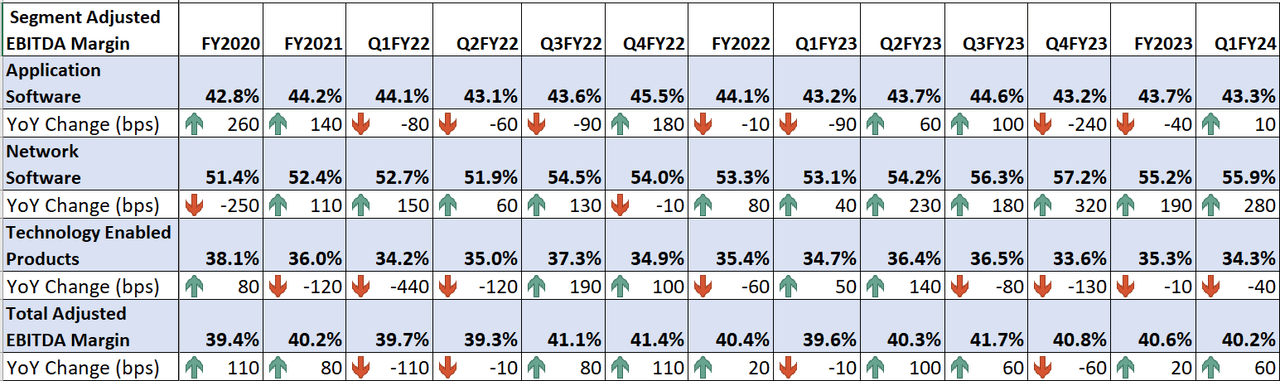

On a segment basis, the Application Software segment delivered a 10 bps Y/Y increase in adjusted EBITDA margin benefiting from a high-margin business mix, operating leverage, and acquisition cost synergies. The Network Software segment delivered a 280 bps Y/Y increase in adjusted EBITDA margin due to cost-saving measures and high margin business mix. Lastly, the Technology Enabled Products segment’s adjusted EBITDA margin declined 40 bps due to lower D&A as a percentage of sales as compared to the previous year’s quarter which more than offset the benefits of volume leverage.

ROP’s Historical Segment-wise Adjusted EBITDA Margin (Company Data, GS Analytics Research)

Looking forward, I am optimistic about the company’s margin growth prospects. As the company improves monetization of its AI offering, it should see pricing benefits in the coming years. AI should also help improve internal productivity for Roper itself. Further, while there are not many pockets of weakness for the company, in some areas where growth isn’t that strong (e.g., Freight end markets), the company has done a good job aligning the cost base with volumes, which should also help margins. In addition, the company’s focus on acquiring high-margin businesses and its good track record of synergy realization should also help margins in the coming quarter.

Valuation and Rating

Roper Technologies is currently trading at a 30.40x FY24 consensus EPS estimate of $18.19 and a 27.81x FY25 consensus EPS estimate of $19.89. Over the past 5 years, the company has traded at a 29.56x forward P/E on average. The company’s valuation on FY24 consensus EPS is at a slight premium to its historical levels. While on FY25 consensus EPS, it is at a slight discount. On the next 12-month basis, the valuation is essentially in line.

Roper has always traded at premium valuations to industrial peers given its strong execution history both in terms of organic growth and bolt-on M&As. However, I see some potential for further re-rating given the company’s exposure to the AI trend which can accelerate its growth in the coming years. If we look at industrial companies that are directly/indirectly benefiting from AI demand, their P/E multiple has re-rated much higher than the historical levels. For example, Eaton (ETN) which is benefitting from increased data center spending due to AI adoption, is trading over 31x FY24 P/E compared to its historical 5-year average of 22.59x. As Roper Technologies starts taking steps to monetize its AI offering much more effectively and roll out more offerings, I believe the market should start noticing Roper’s AI potential resulting in a valuation premium versus the historical average. This coupled with the company’s good earnings growth prospects can result in a good upside. Hence, I am upgrading my rating to a buy.

Risks

-

While the management remains active in the M&A space, if they fail to deliver in executing their M&A strategy in the coming quarters, the company’s revenue growth may come in slower than investor expectations

-

Any delays in the monetization of new AI tools could impact both revenue and margin performance

Read the full article here