Investment overview

I wrote about Ross Stores (NASDAQ:ROST) previously (19 December 2024) with a hold rating as I had concerns about the valuation that the stock was trading at, despite my positive view on the business growth momentum. I am upgrading my rating from hold to buy as the valuation has gotten better, but I am not advocating a big position as the upside is not very exciting. That said, I should note that my expected upside of 10% does not include share buybacks and dividends, which, if included, should push total returns to a low-teen percentage. Fundamentally, ROST performed very well, and I expected current SSSG performance to sustain moving forward, which should also drive EBIT margin expansion.

1Q24 earnings (announced on 23rd May 2024)

ROST reported adjusted EPS of $1.46, above consensus estimates of $1.35. Driving the big beat is same-store-sales growth [SSSG] of 3%, led by positive traffic. This SSSG performance drove total sales to $4.858 billion, modestly beating consensus expectations for $4.823 billion. ROST 1Q24 margin performance was spectacular as gross margin expanded by 140bps to 28.1%, driven by better distribution costs as a result of higher productivity and favorable freight expenses. Below the gross profit line, shrewd execution on cost management can be seen too, as SG&A expense as a percentage of sales fell by 60bps from 1Q23, which led to an EBIT margin of 12.2% in the quarter.

Strong demand momentum

ROST continues to benefit from the inflationary environment, as can be seen from the strong demand momentum. The notable aspect of this quarter’s 3% SSSG performance, which came in at the high end of management guidance, was that it was driven mainly by traffic and an increase in the average basket (pricing growth). This is fantastic because it shows that ROST’s merchandising strategy (increasing the quality of brands by offering highly recognizable brands) has been working very well, such that it is able to effectively “rise prices” even in this environment.

May Investing Ideas

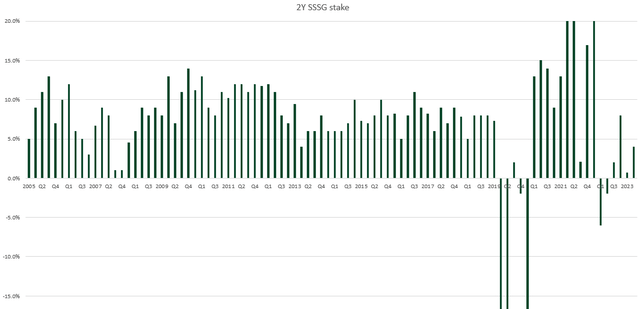

My sense is that this strategy has continued to work well for ROST in 2Q24, and ROST should continue to print healthy SSSG performance in the coming quarter. I inferred this from management 2Q24 guidance, which expects 2% to 3% SSSG vs. 2Q23. On the surface, it seems like there is no improvement vs. 1Q24; however, this guide implies that SSSG is going to accelerate strongly on a 2-year stack basis, from 4% in 1Q24 to 8% in 2Q24 (this is close to the historical average). The reason for using a 2-year stack is that it smooths the impact of seasonality and any one-off benefits in the fiscal quarter (for example, bad weather, a shift in Easter calendar day, etc.). For management to have confidence in issuing this guidance, it must be because they continue to see positive SSSG trends in the 2Q24 quarter-to-date (~3 weeks). In my opinion, this shows that the ROST merchandising strategy continues to work well so far, and given that management is extremely focused on ramping up this strategy, as noted in the earnings call, I think the SSSG outlook is very positive.

I would say it’s our best assessment of where the business is and the merchandising plans we have to further increase the branded bargains we offer as we progress through the year. Company 1Q24 earnings

EBIT margin to continue expanding if growth sustains

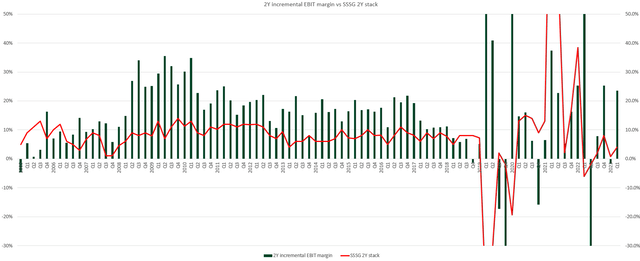

The strong SSSG outlook has a big impact on EBIT margin given the inherent operating leverage that ROST businesses have, and we can already see the impact of this in 1Q24, where ROST reported 12.2% (210bps expansion vs. 1Q23) in EBIT margin after growing topline by 8.1% (430bps above 1Q23) on the back of a 2Y SSSG growth stack of 4%. Plotting the 2Y incremental EBIT margin vs. 2Y stack SSSG shows that whenever ROST sees 2Y SSSG stack in the range of high single digits, 2Y incremental EBIT margin trends in the mid-teens to >20% range (pre-covid). If management guidance is accurate (I should note that management revenue guidance has been very accurate so far, only missing 3 times over the past 10 years), then SSSG on a 2Y stack basis is going to trend in the high single-digit range over the next few quarters, which means EBIT margin can expand further (incremental margin > 1Q24 EBIT margin, which means there is still room for expansion).

May Investing Ideas

Valuation

May Investing Ideas

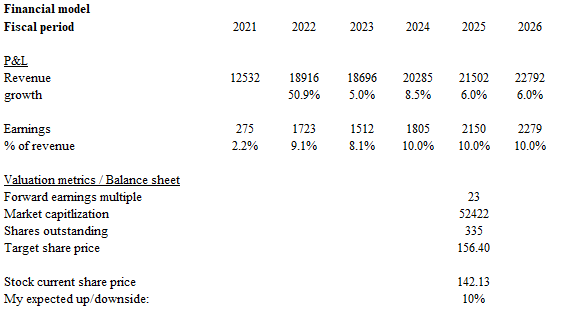

Based on my research and analysis, my expected target price for ROST is $156.40.

- I raised my revenue growth outlook by 150bps in FY24 to 8.5% to reflect the strength seen in 1Q24, which I expect to sustain through FY24 as ROST continues to benefit from the inflationary backdrop and its merchandising strategy. I also believe that the merchandising strategy will have lasting structural impacts on ROST P&L; hence, I upgrade my growth forecast for FY25/26 to be above historical mid-single-digits by 100 bps.

- I have also turned more positive on ROST’s earnings margin outlook, as 1Q24 EBIT margin was outstanding, and based on historical incremental EBIT margin analysis, it suggests further room for EBIT margin to expand. Using 1Q24 net margin as a baseline (10%), I assumed FY24 to FY26 will see at least margins of this level.

- Stocks should trade at a 23x forward PE multiple, which is in line with where peers (The TJX Companies (TJX) and Burlington Stores (BURL)) are trading today. From a historical perspective, at 23x, ROST is just trading slightly above its 10-year average, and I think it is justified given the growth and EBIT margin outlook.

Risk

ROST merchandising strategy may not yield the expected results as consumers taste my change towards independent brands rather than the well-known brands that ROST is focusing on. That would be a very bad situation for ROST, as they most probably need to run promotions to clear these inventories to prepare themselves for the next season after summer (fall or winter), and this will hurt gross margins.

Conclusion

I give a buy rating for Ross Stores due to improved valuation and positive business momentum. While the upside potential isn’t substantial, factoring in share buybacks and dividends could push total returns to a low-teen percentage. ROST delivered a strong first quarter with EPS exceeding expectations and impressive SSSG driven by both traffic and increased basket size. Their merchandising strategy of offering more recognizable brands appears successful, allowing them to raise prices in an inflationary environment. The key risk lies in the potential failure of ROST’s brand-focused strategy. If consumers reject the shift and demand for established brands weakens, ROST might be forced to discount excess inventory, impacting margins.

Read the full article here