Overview of Q3 Earnings

RTX Corporation (NYSE:RTX), previously known as Raytheon, is one of the largest stocks in the defense sector, with multiple business segments that supply missiles, aircraft radar systems, and other defense-systems primarily to the federal government. RTX also services all these systems, which affords them steady and predictable baseline cash flows.

The Q3 earnings conference announced that the financial impact of Pratt & Whitney engine recalls, driven by impure powdered metal manufacturing, is slightly better than expected at $5.4 billion compared to the corporate estimated $6-7 billion. This charge hit EPS by ($1.53), though adjusted EPS remains strong at $1.25. Additionally, RTX does “not expect any significant incremental financial impact as a result of those fleet management plans.”

This is an excellent showing of management’s control of the situation and should serve RTX well. There were concerns that the Pratt & Whitney powder metal impurities were suggestive of poor-quality standards across the board, potentially leading to more manufacturing errors and recalls in other products. Additionally, it was unclear whether management estimates of the financial impact were accurate, with many analysts slashing earnings forecasts substantially. Those uncertainties have been, in our view, largely resolved and we perceive stock-specific risk to now be aligned with peers in the sector.

There were numerous other bullish results from the Q3 earnings announcement:

- RTX announced a $10 billion share repurchase.

- Free cash flow for Q3 rose to $2.8 billion, up from $263 million in Q3 last year and $193 million last quarter.

- The backlog of orders rose to $190 billion from $185 billion last quarter.

Reaction to Israel-Hamas Conflict

RTX rose just under 5%, in line with the defense sector, in reaction to the Israel-Hamas conflict. This kneejerk reaction to bid up defense stocks amidst conflict is common, though the typical investor rally following war announcements is rushing the process and is typically misguided.

There are a couple of fundamental reasons for this, hinging on the unintuitive fact that defense stocks prefer peacetime to war:

- Price hikes are easier to pass in peace times,

- Defense contracts remain very steady and predictable drivers of free cash flow,

- And governments typically force research and production of certain products during war, which can often restrict more profitable endeavors.

This is echoed by Richard Lewinsohn’s commonly cited analysis from the early twentieth century: “In any case, there is no room for reasonable doubt: the armament industry does not desire war, at all events unless it is in some distant country. What it wants is well-armed peace and permanent tension. Too cloudless a peace is a misfortune – but so maybe a war. The constant threat of war: that is what is most promising for this particular business” (Lewinsohn, 1936, p. 150).

The other argument against the immediate flock to defense stocks is that military stockpiles are prepared long in advance and tend to be replenished steadily. Political, strategic, and logistical constraints cause significant lag in the realization of positive financial impacts. This delays the impact on earnings for multiple quarters. It is not trivial, and often unnecessary, for defense contractors to ramp up current production, especially as newer technology is prioritized and transitioned to.

Research Question and Previous Literature

We believe the fundamental reasoning mentioned above is sound, though also understand that sound fundamental reasoning does not necessarily correlate to actual stock price movement. We were interested in exploring how this rationale manifests itself in share price following a conflict announcement. Does the data suggest the availability of significant returns for the reactive investor?

Previous work on this subject is largely concentrated on either a handful of macro events or a narrow time window around conflicts. Broadening both the number of analyzed conflict announcements and the time window should allow for a more comprehensive, accessible, and actionable conclusion.

Defense spending, as argued by McDonald and Kendall in a journal article, is strongly correlated to stock returns. They found a minimal relationship between stock returns and the political party in control. Our research did not investigate defense spending and there is certainly more room for research in this space.

A paper that looked at data similar to ours (Gurdgiev 2017), suggested that positive three-month returns were typically erased in the subsequent three months. Our analysis did not reject this tendency for defense stocks to give up some of the initial gains, though we had some key differences in our approach and models. For instance, we did not differentiate between direct and indirect conflicts ex-post – which runs the possibility of analyzing data with future information that was available at that moment – and we did not control for a first or second term of the presidency. Regardless of the differences, both performance analyses confirm the hypothesis that the bid-up of defense stocks after a conflict announcement is irrational, and that these returns tend to be short-lived.

Data and Method for Regression Analysis

We took significant conflict announcements in the last 4 decades – including conflict announcements that were significant at the time, though ended up de-escalating rapidly – and compiled share price returns for five of the largest defense sector stocks as well as the NYSE Composite Index (NYA). There were 22 events deemed significant, based on market reaction, news sources, and Z-scores.

Data was recorded starting a month before the conflict announcement and ending one year afterward. Share price returns were adjusted for dividends and recorded on a percentage basis to account for the general price increase in equities over the period. Returns, where noted, were normalized to NYA to account for broad market trends and measure defense sector outperformance.

The political party of the president and majority congress control were data scrubbed for the period to analyze political party effects on the share price. Other instruments, such as recession dummy variables and valuation metrics (P/E, forward P/E, and price/cash flow) were experimented with, though found to be statistically insignificant across the data set.

The legend of our data abbreviations is as follows.

|

NoneM |

Previous 30 days |

|

NoneW |

Previous week |

|

Day |

Trading day immediately after conflict |

|

M |

One month return |

|

twoM |

Two-month return |

|

ThreeM |

Three-month return |

|

SixM |

Six-month return |

|

Y |

One year return |

|

Rpres |

Dummy variable, 1 for Republican President |

|

Rcongress |

Dummy variable, 1 for Republican congress |

|

Runified |

Rpres*Rcongress, 1 for unified Republican |

(Legend for Author’s Regression)

Econometric Analysis: Nominal Returns

Defense sector returns in the three and six months following a conflict outbreak are highly dependent on the president and congress political control. R-squared error is a little low, though relatively in line with previous papers analyzing market returns. There is some element of ‘random walk’ within stock returns that tends to add more error into regressions than one would expect with other economic datasets.

Econometric Analysis (A Guaragno)

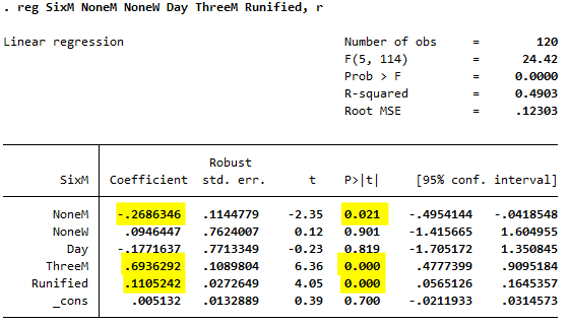

According to the regression analysis of conflicts over the last 4 decades, unified Republican governments add ~5% to post-conflict three-month returns and ~11% to six-month returns. The regression for six-month returns is displayed above, where the variable for a Republican unified government (Runified) is .11 and statistically significant.

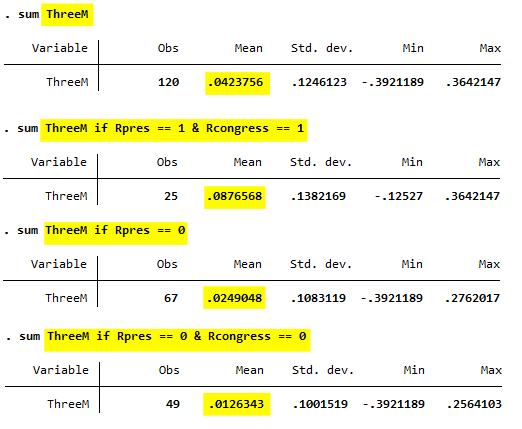

The statistically significant three-month return variable (ThreeM) at .69 confirms Gurdgiev’s results from his paper mentioned above. Where Gurdgiev found an approximately equal decline in the subsequent quarter, our data suggests defense stocks would give up about a third of their three-month returns in the subsequent three-month period. According to the 95% confidence interval and about 4% average three-month return from the table below, an investor can expect defense stocks to be moderately flat to down in that period.

The variable for returns in the prior month (NoneM) is also statistically significant at -.27. This suggests stronger share price rallies if the stock was beaten down in the prior month and weaker rallies if the stock had already run up prior to the conflict announcement. This is the factor we expected to control for with our valuation metric instruments, but the error associated with these instruments was too large. We suspect that there were no substantial conclusions to be drawn from typical valuation metrics since stocks can be under or overvalued for long periods of time without any reaction to the share price. Our relatively short window of price analysis did not allow these instruments to influence returns.

Divided and Democrat unified governments are perceived to be much worse for defense stocks. Below is a breakdown of three-month returns following a conflict announcement, segmented out based on the dummy variables for Republican President (Rpres) and Republican congress control (Rcongress). In the case of a Democrat unified government, average three-month share price returns were a meager 1.3%, significantly lower than the Republican unified government’s 8.8% returns. Note that the standard deviation on these values is large, though the relative averages retain comparative significance and are reinforced in more robust regressions.

A Guaragno

Econometric Analysis: NYA Normalized Returns

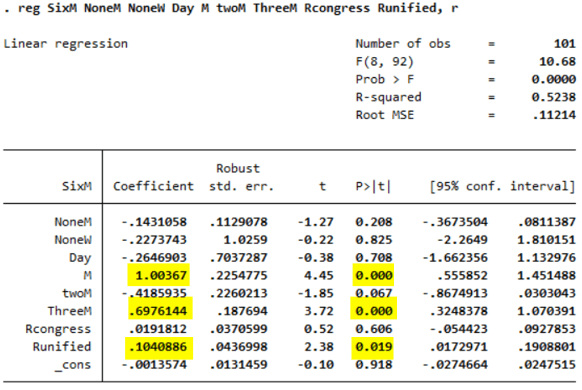

Normalizing returns to the index and comparing relative outperformance yields similar results. Unified Republican control remains beneficial for share price and returns remain concentrated in the timeframe immediately following a conflict announcement. The R-squared error term is slightly better, though very similar to the nominal regression above.

A Guaragno

The statistical significance of one-month returns (M) and three-month returns (ThreeM) at 1.00 and .70 respectively are in line with the nominal regression though offer additional insights. Because these returns are normalized to the NYA, they suggest that the majority of defense sector outperformance occurs in the immediate month following the conflict announcement. The coefficient for a three-month return is comparable to the nominal regression as expected.

Also consistent with the nominal regression, conflict announcements under a Republican unified government offer ~10% more gain than under a Democrat or divided government.

Defense Sector Regression Analysis as it Relates to RTX

Just having a Republican in office during the war is, historically, perceived as beneficial for defense stocks. Republicans are generally more hawkish and quick to increase military spending, though Democrats tend to expand the defense budget when humanitarian concerns or acts of terrorism arise. Thus, it is no surprise that President Biden is planning a ~$100B defense bill, benefitting primarily Ukraine and Israel.

Recall that defense spending is strongly correlated to stock returns, as defense stocks reap the rewards of increased demand for their products. This defense bill should allow the market to perceive more tailwinds for the defense sector than predicted by the regression analysis. Despite the historically subpar returns associated with our current non-Republican unified government, the high standard deviations and error terms in our regression suggest it would not be unreasonable to see continued positive returns for RTX.

The other relevant aspect to consider is the negative correlation to returns one month before the conflict announcement. From a purely historical perspective, investors should consider the recent decline as beneficial to future returns given the timing of the Israel-Hamas conflict. The 18% drop in the prior month suggests an additional upside in the following six months.

We mentioned before that defense stocks generally have multiple quarters of lag before they truly reap the benefits of conflict in their financials, and we are only a few quarters behind that timeframe when considering the Russia-Ukraine conflict. In fact, in the year following conflict announcements, returns in excess of the NYA average of 8.6%. Thus, any negative expected impact on price from the irrational purchasing after the Israel-Hamas conflict should be offset by recognized earnings from the conflict in Ukraine.

Risks

All expectations are based on our research, fundamental understanding, and the citations made throughout this article. Investors should understand that prices need not follow fundamental or historical reasoning. Regression analysis is based on historical price patterns that are not guaranteed to predict the future.

It should also be noted that there is heightened volatility risk associated with defense stocks in wartime. Defense stocks will be the first to move based on any war-related news, whether up or down. Large standard errors in the regression confirmed the inconsistency and spontaneity of share price movement surrounding conflict announcements.

Expected Impact on Six-Month Returns

The table below summarizes all the factors that we believe to be significantly impacting share prices in the next six months. Percentages based on current price levels are inherently not perfectly precise, though they approximate our view of the general impact of each factor.

|

Factors |

Bear Case |

Base Case |

Bull Case |

|

P&W Engine Updates |

5% |

5% |

6% |

|

Other Bullish Q3 Results |

1% |

2% |

3% |

|

Russia-Ukraine Earnings Lag |

4% |

5% |

6% |

|

Overblown Israel-Hamas Impact |

-6% |

-5% |

-2% |

|

Implied Gains from Weak Prior Month |

0% |

1% |

3% |

|

Government Defense Budget |

1% |

3% |

5% |

|

Expected Total Percentage |

5% |

11% |

21% |

|

Expected Resulting Share Price |

~$82 |

~$87 |

~$95 |

Our Bear Case assumes that either most of the benefits surrounding the two large geopolitical conflicts are largely priced in or new developments will negatively impact returns. These values attempt to be realistic bottom ranges on how much each factor’s impact is currently priced into the share price. Details and brief arguments for each factors’ Base Case values are as follows:

The progress that management has made on the Pratt & Whitney powder metal matter has already been partially priced in by the 7.5% jump. However, we consider the reduction in further tail risks, as well as the benefit of forward-looking sentiment, to not be fully priced into RTX. We believe the Pratt & Whitney powder metal issue to be a short-term setback that can be largely overlooked moving forward. Over the next six months, we expect returns to trickle in due to this factor as RTX continues to service engines and reestablish shareholder confidence.

Immediate reactions from earnings announcements (particularly positive reactions) tend to carry momentum over into subsequent trading. This is certainly not always the case, but with much to love about RTX’s Q3 earnings announcement, we consider it reasonably likely that there is further upside attributable to momentum from the share buybacks, high free cash flow, etc.

It is difficult to accurately assess how much the Russia-Ukraine conflict has impacted RTX earnings and share price, though our base case is that the US will continue to offer Ukraine military support through at least the next six months. This will continue to bolster expectations for RTX revenue growth and consistency. In the year following the Russia-Ukraine conflict announcement, RTX overperformed the NYA by about 10%, which is just above average.

We expect headwinds from the statistical likelihood of declines after the Israel-Hamas conflict announcement rally to largely offset gains associated with the ongoing Russia-Ukraine war. The assigned percentage values are based on the bounds for the 95% confidence interval and regression coefficient from our data, assuming a roughly 13% first period gain. In the long term, data analysis and fundamental reasoning would suggest positive impacts on earnings and share price from the US involvement in the Middle East, though this is not factored into our six-month assessment.

Implied gains from the weak prior month are reflective of our regression analysis coefficients, though we have partially offset them with our expectations of gains due to the Pratt & Whitney engine updates. In our regression, we attribute the negative coefficient on prior one-month returns to gains associated with an undervalued stock being driven back to fair value by the catalyst of war. However, we recognize that the catalyst behind the declines this September was the Pratt & Whitney engine recall, so to expect equal contribution from both factors would be double counting similar factors. For that reason, the regression-expected Base Case estimate of 6% due to the weak prior month has been reduced to 1%, reflecting the gains we expect to see from the first factor.

The $100B defense bill in the works from President Biden, in our Base Case, accounts for a modest additional upside to RTX. The message to Wall Street that the White House is open to raising defense spending for these geopolitical conflicts is bullish for defense stocks and should drive expectations of revenue growth. Percentages are based on the 95% confidence interval from our regression analysis.

Conclusion

RTX posted excellent Q3 results, demonstrating a solid grasp on the Pratt & Whitney powder metal matter, a strong commitment to shareholders, and continued strength of their business model. Operating cash flow is expected to be steady from a growing $190B backlog of orders and adjusted EPS remains strong at 1.25.

Despite the sizeable rally off the bottom in early October, we believe RTX is an attractive investment at current levels. Based on our analysis, there is a likelihood of 11% returns in the following six months, with prolonged conflicts setting up further bullish tailwinds in the longer term as well.

We would like to thank Andrew Guaragno for this piece.

Read the full article here