The Tomahawk Cruise Missile – Raytheon (RTX) Missile and Defense Systems

As global forces have entered the stage of direct confrontation (by trade/cold/hot war), the best way for “Western Alliance” members to avoid an all-out war in the East, is by investing in the right weapon systems. Especially since ramping up production capacity often takes years.

Cruise Missile of Choice

The Tomahawk missile has many “code names”, depending on the medium used to launch it or its intended target. In summary, it is a sub-sonic, nuclear capable, long range cruise missile.

It used to have the capability to be fired from land as well – via the BGM-109G Gryphon Transporter Erector Launcher, which was utilized to deploy the missile close to the Soviet Union’s border in Europe. It was later put in storage when the INF Treaty was signed. But now that the treaty is no longer in effect, the US Marine Corps are developing the means for “dry launches“.

It has been fielded in many wars by the US and Britain, with the latter being the only non-US nation that has the missile system (up to this day). In the past, Israel had asked for it, but never got the green light – which in way served it well, as it prompted the nation’s military to develop its own capabilities.

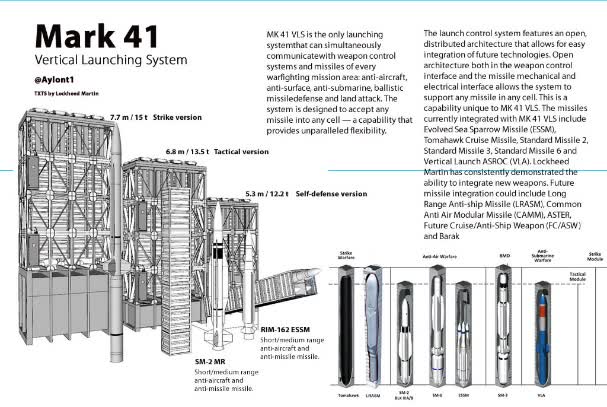

It is currently the US’s main and only operational cruise missile and is well suited for deterring nations like China in the Sea of Japan, as well as in the East & South China Seas. Although subsonic, it has a top of the art navigation system, ‘sells’ relatively cheap and works well in combination with a wide range of missiles. The supersonic all-purpose SM-6 missile is one such example, which like the Tomahawk, also uses the same Mark 41 VLS (Vertical Launching System).

The Mark 41 VLS is the US navy’s primary launching system and is “suitable” for a variety of missiles. (Lockheed Martin)

A lot could change when hypersonic missiles are introduced to the navy, as they most likely won’t be compatible with the Mark 41 VLS, due to distinctive engine characteristics. This could in turn prompt the military to stop buying new Tomahawk missiles. VLS developments for the navy can be used to gauge when hypersonic missiles are ready to be widely utilized. Luckily for RTX (Raytheon (NYSE:RTX)), it produces or co-produces both the SM-6 and the latest hypersonic test missile.

Tomahawk’s exceptional capabilities

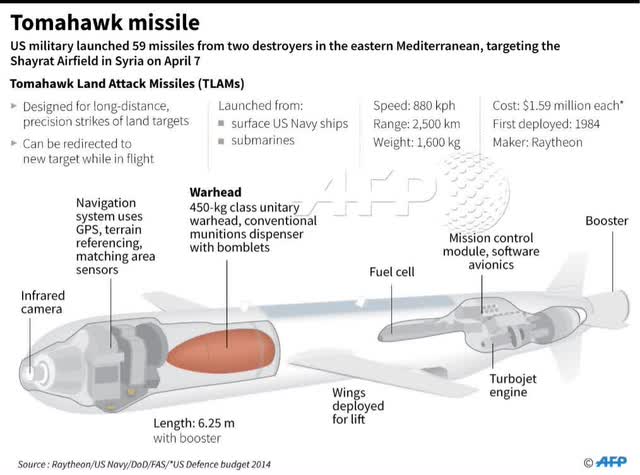

The Tomahawk missile “runs” on a Turbofan engine, similar to that of a regular commercial aircraft. And this is why on average its speed is only 800 km/h (500 mph). But as a result, the missile burns fuel more efficiently and can thus travel up to 2,500 km (1,600 miles).

Added to the above, the latest block version allows for capabilities such as loitering and in-flight re-targeting. This means that the missile can also be utilized as a single-usage reconnaissance drone: It can fly towards a region of interest, loiter and send back data (via its satcom-based two way data link), receive new target “orders” (re-targeting capability) and finally engage.

Tomahawks also have the lasted guidance and navigation systems installed (maximum precision and moving target engagement capability) and fly at an altitude that keeps them off radar (“hide” behind hills, “mix” with ground clutter such as trees and birds). But most importantly, the latest version has counter-jamming technology installed. As we have seen in the Ukrainian war with Russia, the HIMARS missile system albeit very precise, was quiet susceptible to mass jamming efforts.

The cost of a Tomahawk Missile has been declining over time. It can range from $0.9 million up to $3 million. (AFP)

From a value perspective, the missile costs about $1 million and holds a 450 kg (1,000 lbs) warhead, which is the equivalent force of 23 Russian BM-21 GRAD rockets or that of 5 M31A1 GMLRS (HIMARS) missiles. On top of that, the Tomahawk missile can use its own fuel to increase the blast. But it’s only worth investing in such a system if one is buying a “bulk” package, as the initial infrastructure investment covers more than 50% of the purchase price (e.g. Australia’s order of 220 missiles for approximately $1 billion).

Major competing missile: Kalibr

One of Tomahawk’s greatest adversaries is the Kalibr cruise missile. Based on reports that relate to Russian test launches from the Caspian Sea, by ship and submarine, the missile has proven quiet precise and reliable. Although we should take data distribution from Russia with a grain of salt, the nation is famous for its reliable rocket science technology.

Although the Kalibr has a similar average travel range, the missile is prone to jamming and has no two way data sharing link. It is however much more flexible in terms of deployment, as it has been fitted both on Frigates and even Corvettes (the US has Tomahawks installed on Destroyers). On top of that, it is reported that some versions have a second propulsion system installed, which grants the missile a “supersonic sprint” at its final stage of descent.

Cost-wise, if we study Russia’s Kalibr export versions (Klub/Club) and then deduct a reasonable gross profit margin, the domestic equivalent missiles would stand at about $1-1.5 million per – for the simplest land attack version, as per purchases made by Algeria (for example).

Raytheon and its Missile & Defense Segment

Raytheon’s business consists of four segments:

- Collins Aerospace (commercial aircraft services and more)

- Pratt & Whitney (commercial & military aircraft engine production)

- Raytheon Intelligence & Space

- Raytheon Missile & Defense Systems.

The Tomahawk Missile System “falls under” the RMDS segment, which covers about 20% of Raytheon’s Total Net Sales ($4 billion Q2/23, backlog at $35 billion). Even though the P&W segment includes the construction of the F135 engine (that of the F-35 Lightening II Jet), overall the company is primarily a “commercial” one.

This is a good thing. It means that when demand for military equipment runs low (prolonged peace), cash from other segments (e.g. Collins, which is Raytheon’s “Cash Cow”) can be used to maintain existing production capacity, as well as finance further expansion of it. And the Tomahawk Missile System in particular will require investment for capacity.

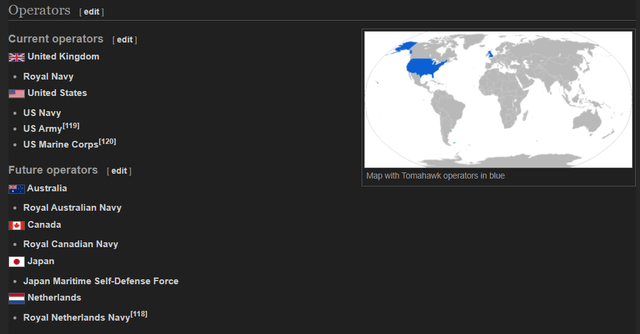

Until recently, the US and the UK were the only two nations that had the system, as exports were forbidden. That has now changed. Below is the list of nations that have so far shown an interest in the system.

Tomahawk Missile System – Current and future operators of the system. Initial infrastructure investments will be required, which will give Raytheon an additional revenue bump. (Wikipedia)

In fact, at least two orders have already come in, one from Australia (valued at $1 billion) and another from Japan (for about 400 missiles). The latter nation is most likely going to order more missiles in the future, as it has set plans to spend as much as $37 billion over the next five years, just for long-range missiles.

But it’s not hard to imagine other nations following suit. In Asia, we have countries like the Philippines, South Korea and Taiwan that wish to deter China’s expansionary ambitions. And this system could work well in conjunction with US provided intelligence.

The US Marine Corps have also successfully tested and activated a ground version of the system. This in turn allows for potential demand coming in from Europe, from countries like Poland, which has ordered as much as 500 HIMARS units – an indication (together with recent EU policies) that the continent will be investing heavily in missile systems in particular.

But Raytheon’s sky is clouded. The Pratt & Whitney recall case will limit cash flows significantly. Aside from reimbursing its clients (for lost revenues), it will also take on servicing expenses and it will have a reduced capacity to build new engines.

The sale of Collins’ flight control system business to Safran will bring in about $1.8 billion in cash, but that won’t be enough to cover the gap. Repairs are scheduled to last at least three years and the initial reimbursement alone was about $3 billion.

On top of that, there will always be the “China problem”. Raytheon’s Missile & Defense segment is not directly affected by Chinese China reveals new details of Raytheon, Lockheed sanctions, but many of the segment’s minor subcontractors are shipping in rare earth materials from the Asian nation. If that would become an issue, the Tomahawk Missile System (and other RMDS systems) would come in more expensive to buyers, company margins would drop below industry average and delivery rates would deteriorate.

The Tomahawk “distribution” is at risk

All in all, there seems to be limited mid-term capability for RMDS capacity expansion. And that at a time when the market for the Tomahawk missile has “opened”.

The Collins segment has never before been so important for Raytheon to maintain its financial balance. The company might need to raise funds soon and should also opt for securing rare earth minerals contracts – maybe in Australia, India, Vietnam and Brazil.

There is limited competition for the Tomahawk Missile System in the world, from the perspective of a long range cruise missile that is highly reliable and can utilize US intelligence and expertise. It’s currently the US’s only long range cruise missile and works well with other missile systems (supersonic and decoy systems).

Raytheon’s outlook and checklist

Demand for both defense and commercial “products” will not decline anytime soon. The current report looks at RTX from the viewpoint of Raytheon’s Missile & Defense Systems (RMDS) segment, specifically focusing on the Tomahawk Missile System (TMS) product. So we assume ceteris paribus (all else equal), when stating that Raytheon will benefit from TMS growth.

Growth potential stems from the fact that the TMS market is an entirely new one, since until recently only the US and the UK could place relevant orders. New orders only came in after navies made test fires (post Syrian war). But now things have changed for good.

In regards to the TMS, we assume that its ROS ratio is that of its segment (~10%, RMDS), which means a bit below the average ratio of all four segments combined (Collins has the highest ratio, ~14%, 2Q/23).

Now, from a broad multi-segment perspective, we should monitor Raytheon’s defense backlog (as of Q2/23 it stands at ~$70 billion, RMDS alone at $35 billion) and track developments in regards to the Pratt & Whitney recall case, so that when

- P&W news have been fully digested by investors (post Q3/23 at least, as the stock price could still move lower) and,

- the company’s backlog has continued to swell (with delivery rates remaining the same or do better, i.e. no new delays),

we can consider taking a stake in the company. That would especially be enticing if the price of RTX’s shares move a bit lower still, in which case the dividend yield will move past 3% – a good yield for a company of this size (and low risk profile).

Read the full article here