Rubrik, Inc. (NYSE:RBRK) reported Q2 ’25 earnings with exceptionally strong top-line growth paired with improved operating margins as the firm rotates more heavily into subscription-based revenue streams. Management was exceptionally optimistic relating to their forecast for the duration of eFY25, with a total revenue growth rate of 31-32%. Modeling the firm’s growth based on known figures, management set the tone of 31-32% growth for Q3 ’25, which will result in Q4 ’25 coming in at roughly 26-30% growth. Given the strong growth trajectory and being in the right market at the right time for data resiliency, I recommend RBRK shares with a BUY rating with a price target of $45.27/share at 7.92x eFY26 price/sales.

Rubrik Operations

Rubrik’s core focus is relatively niche in a high-growth market, data resiliency. The driving factor behind Rubrik’s products is ensuring that when, not if, a breach occurs, companies can get their operations back online as quickly as possible. This has driven major partnerships with companies like Microsoft (MSFT), Mandiant, an Alphabet company (GOOG) (GOOGL), CrowdStrike (CRWD), and Salesforce (CRM), among others. As management stated in their q2’25 earnings call, Rubrik was boots on the ground with CrowdStrike after the July 19, 2024, IT outage.

Given the firm’s subscription-based offerings focused on cyber resilience, a differentiated product that caters to data security, I believe Rubrik has the ability to reach these growth targets, especially as enterprises transition to leveraging more AI/ML applications.

Rubrik’s niche isn’t necessarily competing with the large platforms like CrowdStrike (CRWD) or Palo Alto Networks (PANW) in which these firms’ primary focus is stopping the threat before a breach occurs. Rubrik’s focus primarily relates to what happens post-breach, providing technology that allows for a faster recovery. This factor has led Rubrik to partner with companies who one might think would be competitors, such as CrowdStrike, Cisco Systems (CSCO), and Microsoft (MSFT), among others. As CrowdStrike’s Falcon platform provides 98% coverage and a time to detection of 4 minutes, Rubrik’s platform has demonstrated a time to recovery of 35 seconds, significantly lower than an unnamed competitor’s 5-hour time to recovery.

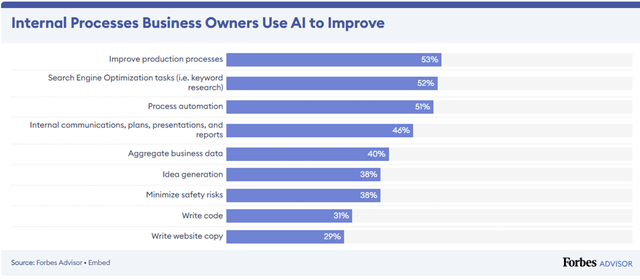

These features are exceptionally necessary when considering the transition to machine learning and artificial intelligence for business applications. According to a Forbes report issued in April 2024, 53% of businesses leverage AI to improve business production processes and 51% of businesses use AI for process automation.

Forbes

These figures are likely to continue growing as GPU availability becomes more widespread for enterprises. Accordingly, Nvidia (NVDA) reported that 60% of deployed AI infrastructure in q1’25 was driven by non-hyperscaler customers. This may suggest more enterprises are enhancing their private data centers to support AI/ML testing and inferencing. Given the level of interest in utilizing AI/ML applications, I believe Rubrik has a long runway for growth, well beyond their $919mm subscription-based ARR reported in Q2 ’25.

I think the ultimate question an investor has to ask is whether Rubrik will maintain its independence or position itself to be acquired. Arguably, one of the larger cybersecurity vendors would make for a prime facilitator for such an acquisition; however, an acquisition by a CrowdStrike or a Palo Alto Networks may create some challenges given Rubrik’s universal approach to cloud security. A potential acquirer could be Snowflake (SNOW) given the firm’s need for cyber resilience. Arguably, Microsoft would be a strong acquirer given the two firms’ relationship and customer overlap; however, given that a deal hasn’t already occurred, I don’t believe it will be likely that one will occur in the future given the likelihood of a higher buyout premium.

Though there have been no acquisition talks, at least that are public, the possibility is there given the drive for platformization across cybersecurity departments. For example, CrowdStrike acquired Flow Security in CYq1’24 to expand its cloud security features with DSPM. Palo Alto Networks acquired Dig Security at the end of CY23, a company that also provides DSPM features.

Similarly, Rubrik acquired Laminar in August 2023. Laminar brought Rubrik DSPM into the platform to couple cyber recovery with cyber posture across enterprises, cloud, and SaaS platforms.

Risks Related To Rubrik

Bull Case

Rubrik is in the right market at the right time, with data recovery being at the top-of-mind post-IT incident as a result of the CrowdStrike update in July. One of the greatest challenges IT faces right now is ensuring data security, and in the instance of a breach, recovery. This should push growth for Rubrik further along as investments in AI/ML applications continue to grow.

Bear Case

Larger cybersecurity platforms such as CrowdStrike and Palo Alto Networks have similar offerings as part of their respective integrated platforms. This may make Rubrik disadvantaged when considering the platformization trend in cybersecurity. Rubrik is also in the early stages of growth, posing a risk to share decline is hints of a slowdown show.

Rubrik Financials

Corporate Reports

Given that some information is not publicly available, historical financials will not be fully presented. Do note that Q3 ’24 & Q4 ’24 are estimates based on management’s revenue forecast for Q3 ’25’s growth rate of 31-32%.

Rubrik has realized strong revenue growth since going public in April 2024. Looking at the quarterly financials, Rubrik’s revenue has grown sequentially every quarter, with no expectation of this trend letting up in eFY25. I’m forecasting revenue to grow by 31% in eq3’25 with eFY25 revenue growing 33% to $834mm. In addition to this, I’m forecasting ARR to grow by 32% on a year-over-year basis for eFY25 to $1,032 mm and 26% in FY26.

I believe subscription growth will be driven by the adoption of AI/ML applications. Many cybersecurity firms, including CrowdStrike and Palo Alto Networks, have stated multiple times that these large language models provide a significant gap for highly valued data that needs to be secured. As Mr. Bipul Sinha, CEO, Chairman, and Co-Founder of Rubrik said on the earnings call, it is no longer about “if” but “when.” Given the expectation of a data breach inevitably occurring, enterprises having the ability to bring systems back online at a faster rate can be considered a cost-saving measure. I believe that this business solution provides a durable case for enterprises adopting Rubrik’s data integrity platform.

Valuation & Shareholder Value

Corporate Reports

RBRK shares currently trade at 7.75x TTM price/sales. RBRK is currently trading on par with its peer cybersecurity cohort, which holds a market cap-weighted average price/sales multiple of 7.92x.

Seeking Alpha

Using my financial forecast for eFY26 sales growth paired with its peer average trading multiple, I believe RBRK shares can price at $45.27/share at 7.92x eFY26 price/sales. Given the company’s strong presence in data resiliency and being in the right market at the right time, I recommend RBRK shares with a BUY.

RBRK shares have significant underperformed the NASDAQ Index (COMP:IND) since going public, suggesting that investors haven’t yet bought into the company’s outlook. Now that the lock-up has expired, investors will have the opportunity to buy into new positions.

TradingView

Read the full article here