Editor’s note: Seeking Alpha is proud to welcome Unconventional Rider as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

Rumble (NASDAQ:RUM) is significantly undervalued today and I believe the stock represents a 2x or greater opportunity over the next 12 months. This growth will be driven by a rapid increase in advertising revenue as Rumble deploys infrastructure to “turn on” the monetization engine. Rumble’s business structure is uniquely positioned to enable this rapid growth through secondary and tertiary avenues for user monetization, and the stock will outperform in the near term as investors realize that lock-up risks have been grossly exaggerated by short-sellers.

Rumble’s Structure Enables This Rapid Monetization

Rumble is set to turbo charge revenue growth over the next 4 quarters in three steps: first by “turning on” monetization with programmatic ads; then by leveraging recently acquired content to grow subscription revenue; finally, by deploying the infrastructure to facilitate sponsorship revenues.

At its core, Rumble is an intentional platform rather than a discovery platform. The Company has spent the last 3 quarters building the infrastructure to monetize users under the intentional model, and is just now beginning to deploy these tools.

A “discovery user” is someone looking for new content that they will enjoy watching in the future. An “intentional user” is someone that already knows what they are looking for and is looking to interact with the content on a deeper level. YouTube and the discovery platform business model are built around a monolithic revenue system: more content equals more impressions equals more revenue. Conversely, the intentional platform model requires less content, but promotes higher engagement. This generates second- and third-level revenue in the form of paid channel subscriptions and product placement via brand sponsorships.

Rumble’s Intentional Business Model (Company Presentation)

Rumble Has Not Fully Deployed Programmatic Ads and Will See Significant Revenue Growth From This Segment

Programmatic ads are the base of Rumble’s revenue stack and the company can scale ad revenue very quickly. YouTube currently runs 2 pre-roll ads every 6 minutes in its videos, while Rumble runs only one ad on desktop videos and none on mobile. Despite running significantly fewer ads, Rumble still generates ~$20M in ad revenue per quarter. This tells us that Rumble is able to generate significant revenue with just a fraction of YouTube’s monetization infrastructure.

What is the easiest way for Rumble to improve monetization? Run more ads. Q2 management commentary indicates that management has already begun implementing this strategy. Rumble reported a notable increase in monetization through the introduction of pre-roll ads on desktop and their self-serve platform. Increasing the number of advertisements will result in an almost immediate improvement in ARPU and, thereby, revenue growth.

Do Not Expect a Decline in MAUs

Bears might claim that Rumble’s right-leaning political content base is not able to sustain 40M+ MAUs in the long term, referencing the sharp decline in users between Q4 2022 and Q1 2023 that was attributed to the waning election cycle.

It is worth noting that such objections ignore Rumble’s impressive acquisition of opposing and apolitical content creators. Rumble recently signed left-of-center political figures such as Russell Brand and presidential candidate RFK Jr. They have inked exclusive content deals with cultural influencers like DJ Akademiks (8M+ followers) and streamers iShowSpeed and KaiCenat (20M+ subscribers, collectively), a move that insulates the userbase from political seasonality. Rumble has demonstrated that opposing and apolitical content creators can be drawn to the platform because of the monetization opportunities.

Locals & CallIn Integration Will Grow Subscription Revenue From Rumble’s Content Base

Subscriptions are an untapped revenue stream for Rumble and preliminary data indicates that we will see meaningful growth in this segment over the next 4 quarters. Rumble’s subscription product, Locals, allows viewers to pay a monthly fee for access to premium creator content, with Rumble receiving some percentage of that fee. This is a much newer product in a market that, unlike programmatic advertising, does not have a clear market leader. Locals provides the necessary infrastructure for creators to set up direct-to-viewer subscription shows. Their other acquisition, CallIn, serves as the “Rumble Studio” or an isolated app that gives creators the ability to live stream and manage content directly within the app.

This infrastructure is entering its deployment stage and there is clearly a market willing to use it. Recently, Rumble announced that Steven Crowder’s “MugClub” community has generated over $7.5M in subscription revenues in the five months since launching. Assuming Rumble takes a 30-40% share of the subscription revenue (the company has not disclosed exact revenue sharing metrics), this show alone could generate $2-3M of annual revenue for Rumble.

However, the true value of this announcement lies in the proof-of-concept for a standalone creator economy. Rumble has now demonstrated that subscriptions are exponentially more valuable than ad revenue, and caused creators to ask the question: “can YouTube or cable TV actually offer this kind of money?” We believe this business line will be a near- to medium-term catalyst for further revenue expansion.

Sponsorship Revenues Will Begin To Ramp Up in 2024 Following the Roll-Out of RAC

Rumble’s viewer base represents an extremely attractive market audience for product placement and sponsorships, and revenue from this segment will kick in when Rumble launches the Rumble Advertising Center (RAC) in early 2024.

RAC will provide a centralized infrastructure for brands to build sponsorships with new creators in a streamlined and efficient marketplace. Today, this process is entirely manual for Rumble, and automating the system via RAC will greatly expand the number of sponsorships and revenue to Rumble. Today, if Wrangler wants to sponsor a popular creator of Western content, Rumble must broker the deal directly with the creator. This is true across all media platforms, and Rumble is in a unique position to be the first major marketplace for creators to efficiently find sponsors for their channels.

Rumble is building the infrastructure for these interactions to be facilitated in a standardized marketplace. Brands can utilize Rumble’s content and viewer data to quickly identify and set up sponsorship agreements with the right creators. Likewise, creators can put themselves out there to partner with brands that may not be aware of their content. Rumble benefits by acting as the broker and making a commission or royalty on each sponsorship flowing through the platform.

Just as YouTube positioned itself as the funnel for creator content, Rumble wants to be the funnel for the next generation of the creator economy. It is a central platform creators can use to reach viewers, facilitate deeper interactions with their audience, and generate revenue without traditional media intermediaries.

Valuation

With this understanding of Rumble’s early position on the path to steady-state cash flow, we can better value the business based on what Rumble’s revenue could look like at certain monetization thresholds.

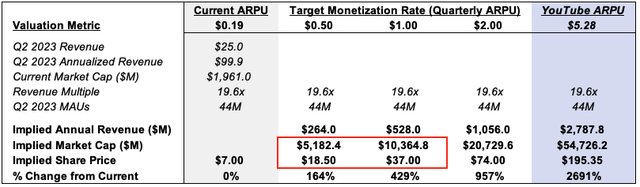

To see how different ARPU figures would impact valuation, I first calculate that Rumble’s current ARPU is roughly $0.19 (2Q23-annualized revenue of ~$100M divided by annual active users of 44M MAUs for 12 months), to establish a revenue multiple of 19.6x (based on a share price of $7.00 and ~280M shares outstanding). Using these baseline calculations, we can show implied figures for annual revenue, market cap, and share price at the $0.50, $1.00, and $2.00 ARPU levels.

Author

Rumble’s company presentation draws a similar comparison based on YouTube’s ARPU of $5.28, and we believe this is a valid “book end” to use here. Given the amount of monetization infrastructure being deployed over the next year, we believe a 3-5x growth in ARPU is a reasonable target for Rumble. At $0.50 ARPU, this implies a market cap of $5.1B and share price of $18.50.

It is then helpful to benchmark Rumble’s valuation multiples against historical data for YouTube and Facebook when these businesses were at similar stages. The data indicates that Rumble today is undervalued compared to both YouTube in October 2006 (Google acquisition), and Facebook in May 2012 (initial public offering).

Author

I do not assert that Rumble will be just like YouTube or Meta / Facebook in the next year. However I do expect to see a significant increase in monetization over the next 12 months, and believe the stock will appreciate to $18.00+ during this period. This price target is based on an ARPU of $0.50, a level that Rumble can easily reach through the expansion of programmatic ads and subscription revenue.

Short-Sellers Are Wrong About Lock-Up Risk

I believe the number of shares that will be sold after lock-up is much smaller than headline figures suggest. The bearish technical argument against Rumble is that the September 16th lock-up expiration will result in a massive sell-off. This is understandable and has been happened to many de-SPAC companies previously. Culper Research’s short report estimated 315M shares coming off lock-up in September. After digging through Rumble’s registration statements, it became clear that while 300+ million shares are no longer subject to the lock-up, the number of shares that could actually enter the market is substantially lower.

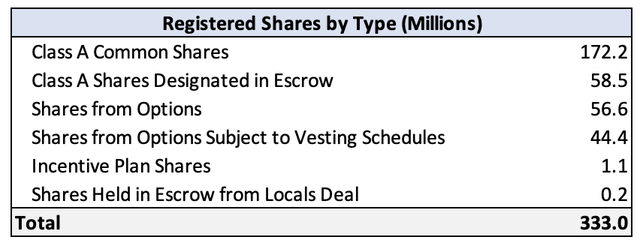

This analysis is based on the “Selling Holders” section of Rumble’s S-1/A filed on 11/4/22. The filing provides a list of registered shareholders with their total shares. However, the main table does not clarify any further breakdown of these shares until the footnotes. By going through each footnote and breaking down the “total” share count into categories, I generated Table 1.

Table 1

Rumble S-1/A

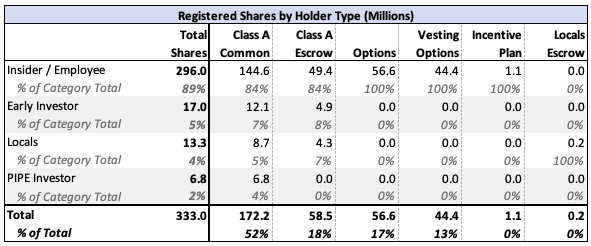

For a different view, I looked at the exact share counts in the footnotes for each listed registered holder, placing each into a category to generate Table 2. The “Early Investor” category was used for any names that did not have a clear place in a different category. All PIPE Investors and individuals connected to the Locals deal were noted as such in the S-1 footnotes.

Table 2

Rumble S-1/A

What does this tell us? First, we see that 296M shares, or 89% of the total are held by insiders and employees. Of these, 282M are held by the CEO and other executives / board members. These high level employees that would understand that would understand the significance of filing for a sale. The only notable exception in this category is the SPAC Sponsor, Cantor Fitzgerald / Howard Lutnick, with ~11.6M shares. Since options and incentive shares are also held by insiders, we can group them in the “not available for sale” category. PIPE investors have been off lock-up for a long time and it is safe to assume they have already sold.

Second, it shows that 58M of those shares are held in escrow per the lock-up agreement. Those shares only vest if Rumble meets the $15.00 and $17.50 trading thresholds for a certain amount of time. That obviously isn’t going to happen before the lock-up expires so we can count them out of the lock-up equation.

Culper’s short report listed 315M shares available for sale when the lockup comes off. We believe that figure is closer to 172M. Of that amount, 133M is the CEO, management, and board, categories that historically do not sell immediately after the company has gone public. These holders are not foolish, and would not file to sell their shares as that will severely hurt the stock.

To summarize, when removing the insider holders, I found that the number of lock-up shares that could actually be sold in September is ~32.4M, made up of 12.1M shares held by early Rumble investors (Narya, Peter Thiel, etc.), 11.6M shares held by Cantor Fitzgerald, and 8.7M shares held by parties related to Locals.

Risks

The largest risk facing Rumble is the company’s ability to execute on this monetization strategy. Rumble has already proven that it can attract users, and management’s commentary on the Q2 earnings call indicates that they have finished buying up new content. As such, we do not believe Rumble will face a large decline in users or liquidity issues. We would become bearish on the stock if Rumble does not show improved user monetization within 2 quarters, or reports significant delays in rolling out their monetization infrastructure.

Closing Thoughts

To summarize, Rumble is now primed to rapidly grow revenue as it “turns on” user monetization over the next 12 months. RUM’s lackluster recent trading performance has been driven by a fundamental misunderstanding of the lock-up, and will be reversed as short-sellers unwind positions after realizing. Rumble has been undervalued by the market and will begin to realize its true value potential as it the company fully deploys its monetization infrastructure.

Read the full article here