Saab (OTCPK:SAABF) is seeing some secular push in margins in surveillance which is driving overall growth, and in general the businesses are performing well with major tailwinds from the spending push in defense that is happening across Europe. While not essential to business development, as Sweden already provides services to NATO programmes like the Eurofighter, Sweden joining in NATO will help Saab’s campaigning for its defense products in Europe where historically other countries have been more aggressive in getting their foot in the door than Sweden has. Segments like surveillance will be easier to compete in as a NATO member rather than being outside the explicit alliance. However, on balance we don’t see too much upside, although some premium over European defense peers is acceptable.

Q2 Comments

Dassault’s (OTCPK:DUAVF) Rafale has taken a lot of business unexpectedly among the 4.5th gen fighters from Europe. Beating out the Lockheed (LMT) F-35 in the UAE, and with business in more unaligned countries like India, they have been the star performer in aeronautics. The French government played a big part in the UAE win, since it campaigned to make that deal happen. Sweden has traditionally not provided this support to Saab’s business development, famously failing in Switzerland’s referendum moment some years ago.

But the Saab Gripen is solid and cheaper than other fighters, also cheaper to maintain and requires less runway infrastructure. They have just built a production line in Brazil, and they have a good offering in terms of price point for the Latin American markets. Good delivery rates as well as business with training craft with the USAF this quarter has driven sales. EBIT is being dragged down by aerostructure as well as emerging scale on new production lines as Saab has invested in capacity growth in a moment where defense budgets have been massively revised upwards.

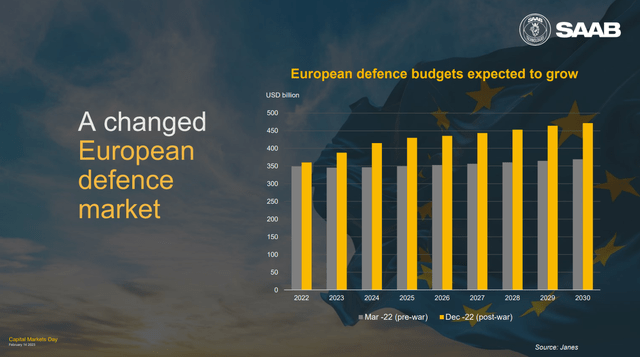

Defense Budgets (CMD)

Dynamics provides a lot of NLAWs and grenade launchers as well as their ammunition which has been essential for Ukraine’s war effort. Sales have been good but negative mix effects have weighed on profitability. Saab doesn’t like to clarify these mix effects, and repeatedly across earnings calls emphasise that it really just depends on when deliveries take place and it’s all quite random and meaningless. What matters is that Saab guides for theoretical 10% EBIT margins for Dynamics based on the backlog development, which is smoother and more important to track. Current run-rates are around 8% so there is scope for improvement, and these products are the ones that benefit from the recent growth in long-lasting, attrition-based ground wars.

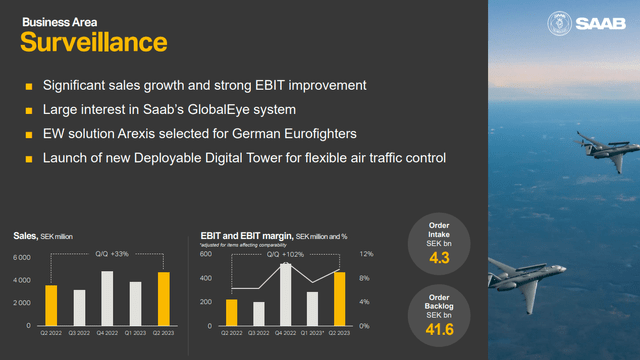

Surveillance (Q2 2023 Pres)

Surveillance has been the segment that has driven profits. Also here there are theoretical 10% margins, with current run-rate margins at 8%, so scope for improvement. Moreover, they have won an essential contract to provide an EW solution for the Eurofighter. This is testament to Sweden’s closeness to NATO despite not being a formal member, and is also a signal for more business opportunities, especially in EW which is more sensitive and financially is where the bread is buttered for Saab, if they do become a full member, although whether that will happen, both from the NATO ratification side as well as Sweden, is still a little unclear pending decisions and in light of resistance from Hungary and Turkey. New products like deployable towers as well as the GlobalEye system are positives as well.

Kockums is also going to benefit from some SIGINT contracts with Poland, another data point for the importance of rising European defense budgets for Saab’s markets. To that point, international orders are beginning to dominate the mix. Also, aftermarket exposures and strong growth in submarine spending budgets and general coast guard efforts support the Kockums business’ margins, with aftermarket mix growth supporting 100% EBIT growth.

Bottom Line

Saab trades at a premium from both Dassault and BAE Systems (OTCPK:BAESF). Dassault is a special case in terms of valuations, but on a PE basis, Saab is above 25x PE while Dassault and BAE are around 17-18x in PE.

We don’t think Saab’s price is compelling, but we disagree that it is overvalued as it is benefiting from being at the beginning of utilisation run-ups at newly opened facilities. Moreover, campaigning in Latin America for the Gripen, for SIGINT ships with Netherlands, and general business development with dynamics which is the exact exposure you want for the Ukraine war is setting it up for margin expansion in line with the CMD as this new backlog liquidates. Dassault and BAE have been more muted in terms of incremental delivery activity, although all of them benefit on the backlog side as new contracts come in for Europe’s expanding military budgets.

In a couple of year’s time the multiples will be converging. But at this premium, we aren’t terribly motivated to take any sort of position. Moreover, the opportunities in defense have already been thoroughly exploited.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here