Sabre Corporation (NASDAQ:SABR) recently delivered double digit quarterly bookings growth, and announced expectations of positive FCF in 2025. Along with FCF margins increasing thanks to acquisitions and annual savings, SABR intends to reduce its net debt/EBITDA ratio, which may enhance the stock valuation. Yes, I see risks from the total amount of debt and changes in the data privacy regulation, however SABR could trade at a higher stock price.

Business Model: Sabre May Obtain Significant Business Growth From Big Data Analysis Of Travelers’ Data

With decades of experience in the sector, Sabre appears to be a leader in distribution systems for air ticket reservations in the United States. Of course, this allows the company to establish relationships with a huge number of clients as well as access to regions and markets around the world through commercial agreements with airlines, hotels, developers, and distributors among others.

Its operations include digital services and software for various companies in the tourism and travel industry, such as international hotel reservation systems as well as medical coverage services for travelers or rental agencies.

In addition to these services, Sabre is dedicated to the programming of calendars for the airline crew, relocation of passengers in case of suspension or irregularities in flights, or day-to-day administration in hotel management. These services are accompanied by technologies developed with artificial intelligence and machine learning, which also allow the company to collect consumer data and make a precise analysis of trends in tourist spots, attractions, and other factors. Considering the importance of data analysis these days, I believe that Sabre may obtain significant business growth from big data analysis.

The global Big Data Analytics in Tourism Market is expected to grow at a significant CAGR of +13% during the forecasting Period (2023 to 2030). Source: Big Data Analytics in Tourism Market is expected to represent Significant CAGR of 13% by 2030

Sabre currently operates with two segments, one for travel solutions and the other for hospitality on trips. The first of these segments involves its global distribution system that provides solutions for both travel sellers and buyers. On the other hand, the hospitality segment is exclusively dedicated to its commercial contacts with hotel establishments, mainly through its software as a service system through which the company offers management and reservation platforms for hotels.

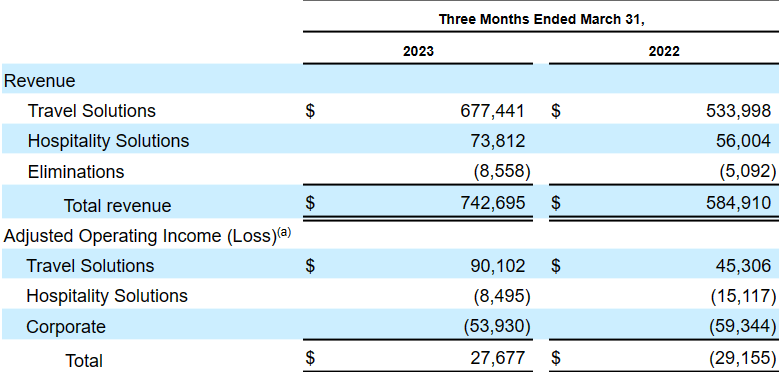

The company makes most of its revenue from travel solutions. In the three months ended March 31, 2023, revenue worth $677 million came from offering travel solutions. The total revenue for the quarter was $742 million.

Source: 10-Q

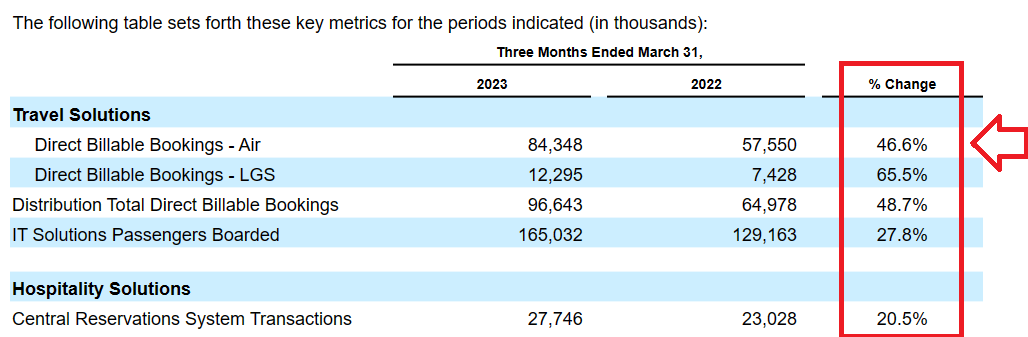

With that about the distribution of revenue, I believe that the company is worth a quick look mainly because of the recent increase in bookings seen in the last quarter. The number of bookings increased at a double digit as compared to the same period in 2022. Further increase in bookings will most likely lead to economies of scale, sales growth, and FCF growth.

Source: 10-Q

Beneficial Guidance And Beneficial Market Expectations That Include Significant FCF Growth In 2025

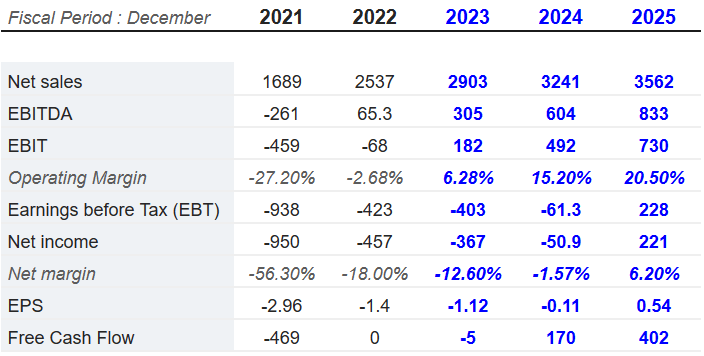

Market estimates for the year 2025 are quite impressive. Analysts out there expect 2025 net sales of $3.562 billion, 2025 EBITDA of $833 million, EBIT of $730 million, and operating margin close to 20.5%.

2025 Net income would stand at close to $221 million, with 2025 free cash flow of about $402 million. It is worth noting that investors expect significant FCF margin growth in 2024 and 2025. In my view, if the figures are as good as predicted, the stock price would most likely trend higher.

Source: marketscreener.com

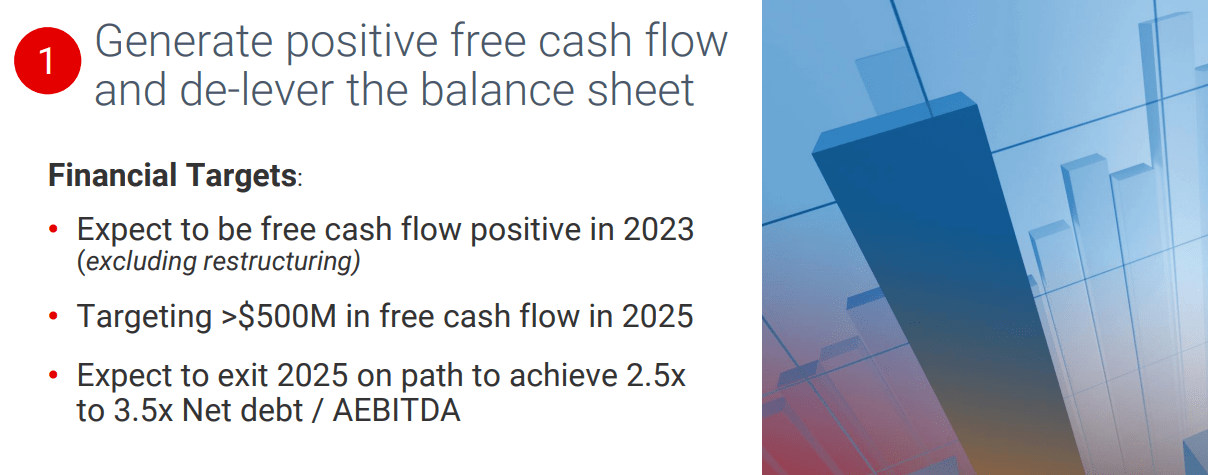

The expectations from management are also worth a look. In the last quarterly presentation, the company noted 2025 FCF of close to $500 million and net debt/EBITDA close to 2.5x-3.5x.

Source: IR Presentation

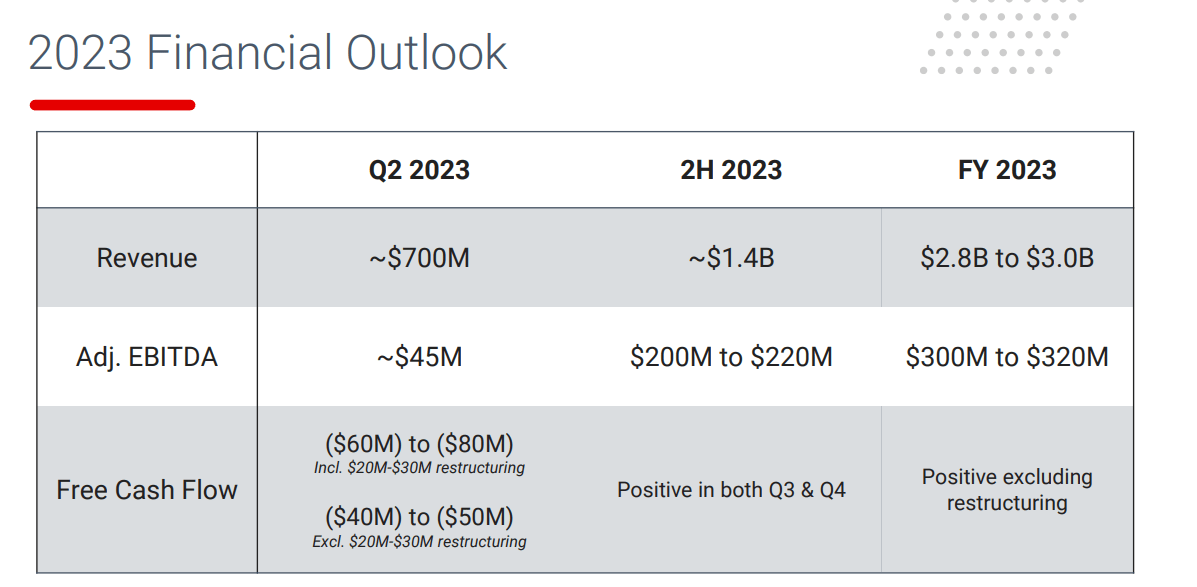

For the year 2023, management noted net sales close to $2.8-$3 billion, an adjusted EBITDA of $300-$320 million, and positive FCF excluding restructuring.

Source: IR Presentation

Balance Sheet

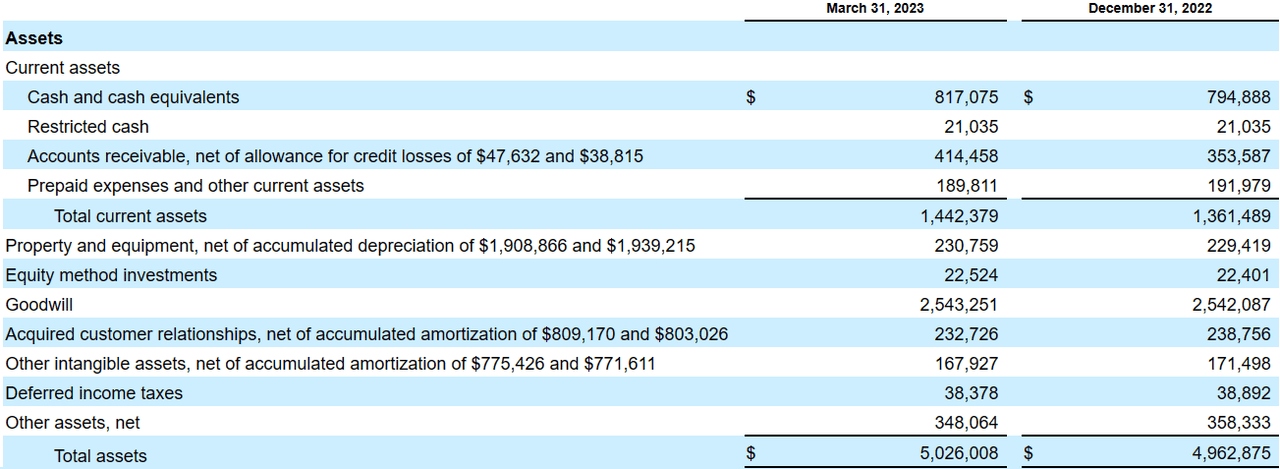

As of March 31, 2023, the company reported cash and cash equivalents worth $817 million, restricted cash of $21 million, accounts receivable of $414 million, and total current assets worth $1.442 billion. I am not really worried about potential liquidity issues because the total amount of current liabilities is less significant than the total amount of current assets.

Long term liabilities include property and equipment, net of accumulated depreciation of $230 million, goodwill worth $2.543 billion, acquired customer relationships of close to $232 million, and total assets close to $5.026 billion. The asset/liability ratio appears to be lower than 1x, which some investors may not appreciate.

Source: 10-Q

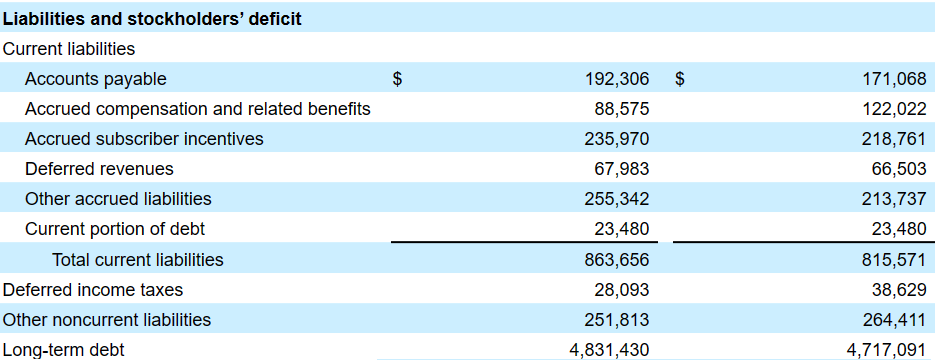

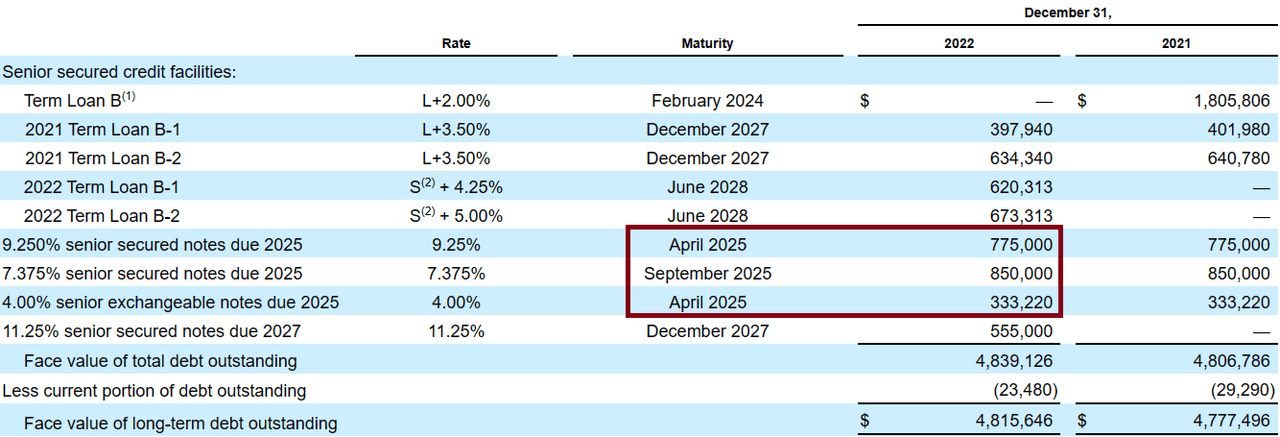

The list of liabilities includes accounts payable worth $192 million, accrued compensation and related benefits of about $88 million, accrued subscriber incentives worth $235 million, deferred revenues of $67 million, and current portion of debt close to $23 million. Long-term debt stands at about $4.831 billion, which does not seem small. I would understand some investors who do not invest in Sabre because of the total amount of debt.

Source: 10-Q

DCF Model

Considering the quarterly increase in direct billable bookings and passengers boarded, I believe that the big data technologies and AI technologies are working in the right direction. I would expect further successful development of innovations through investments in technological programs that allow customizing the experience of its clients as well as maintaining the high quality of its services and expansion of FCF margins.

I would also expect further extension of business relationships with new customers besides sustaining existing relationships, offering the products such as data analysis services for advertising positioning. I also assumed that authorities may not stop or regulate the freedom that Sabre enjoys to treat information from clients as well as to work with third parties.

We collect, process, store, use and transmit a large volume of personal data on a daily basis, including, for example, to process travel transactions for our customers and to deliver other travel-related products and services. Personal data is increasingly subject to legal and regulatory protections around the world, which vary widely in approach and which possibly conflict with one another. Source: 10-Q

One of the positive points to highlight in Sabre’s service offering is that it facilitates the development of other business models, avoiding large or emerging companies from concentrating time and investment on the development of their own distribution systems. In addition to travel agencies and commercial airlines, the company currently has 42,000 hotel agencies of different sizes throughout the world. I assumed that more clients will learn about the business potential of Sabre, which will most likely serve as a revenue catalyst.

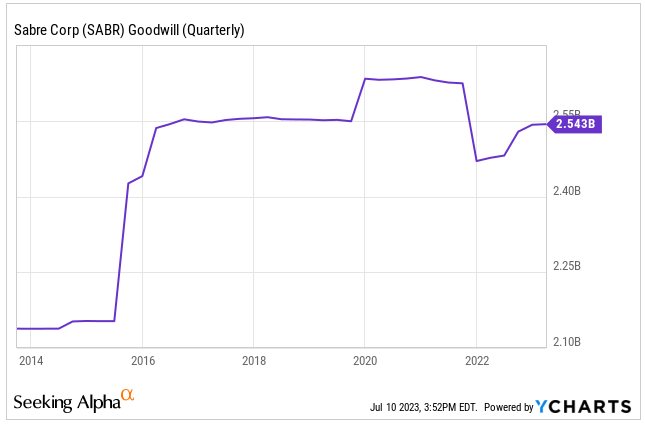

Under my financial model, I would also expect new acquisition of small competitors, which may bring new technologies and capabilities. The company is well-known for acquiring peers. Techsembly was a recent acquisition, but the past growth of goodwill indicates significant expertise in the M&A markets.

Sabre announced the acquisition of hospitality e-commerce provider Techsembly. Terms of the transaction were not disclosed. Source: Sabre acquires e-commerce provider Techsembly to expand and accelerate its hospitality retailing solutions

Source: YCharts

Besides, I believe that Sabre Corporation may soon announce new divestitures to reshape the balance sheet. Considering the expectations of net debt/EBITDA for 2025, I do believe that some sale of assets could occur. As a result, I believe that the demand for the stock could increase. In this regard, it is worth noting that Sabre sold some business interests in Conferma in 2023.

On February 1, 2023, Sabre sold common shares, representing a 19% interest in Conferma’s direct parent, to a third party for cash consideration of $16 million. Source: 10-Q

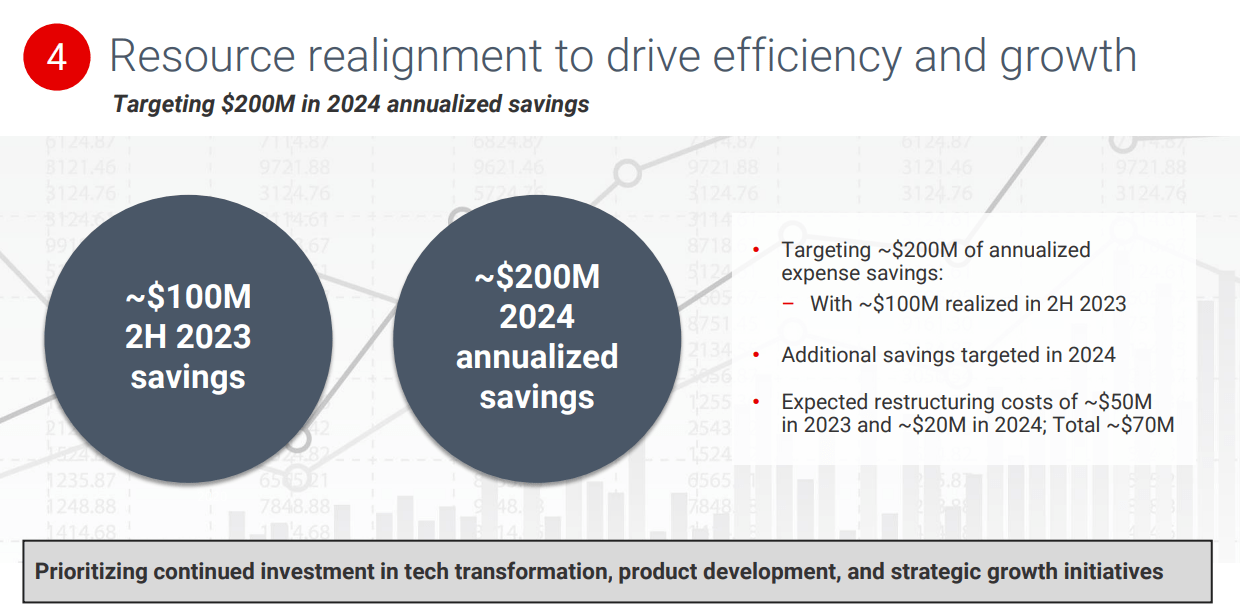

Additionally, I am optimistic about the annualized savings expected in 2H 2023 and 2025. If the efforts lead to FCF margin expansion, I think that we could see FCF growth and increases in the stock price.

Source: IR Presentation

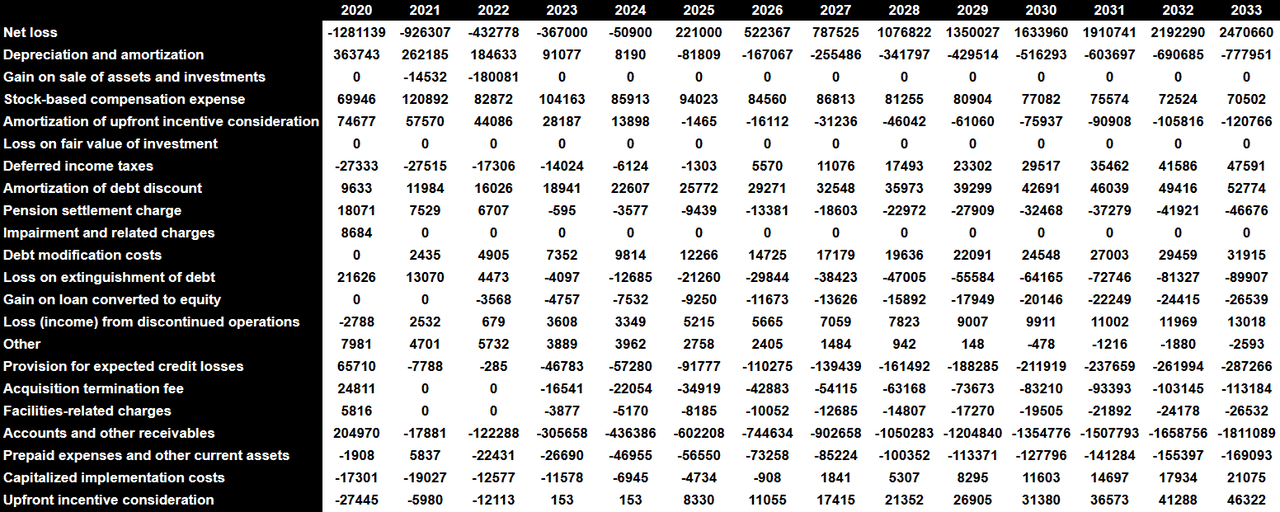

My financial model included 2033 net income of about $2.47 billion, depreciation and amortization of -$778 million, stock-based compensation expenses worth $70 million, and amortization of upfront incentive consideration close to -$121 million.

I also included deferred income taxes worth $47 million, amortization of debt discount close to $52 million, provision for expected credit losses of -$288 million, facilities-related charges of about -$27 million, and changes in accounts and other receivables worth -$1812 million.

Additionally, with prepaid expenses and other current assets of about -$170 million, capitalized implementation costs of $21 million, upfront incentive consideration close to $46 million, and changes in accounts payable and other accrued liabilities of $2.229 billion, cash used in operating activities would be close to $1.425 billion. I also assumed 2033 additions to property and equipment of -$117 million, which implied 2033 FCF of $1.308 billion.

Source: My DCF Source: My DCF

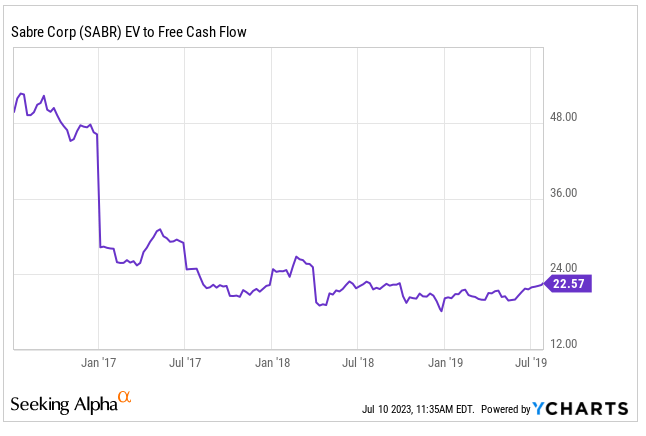

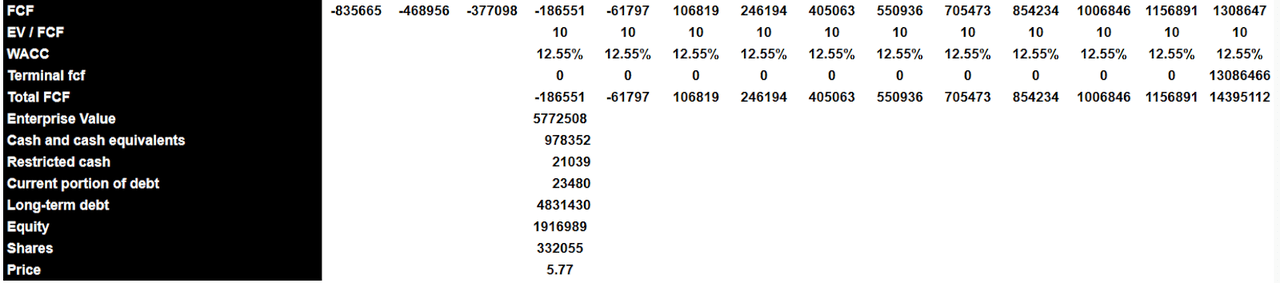

I believe that a terminal EV/FCF multiple of 10x would make sense. In the past, when the company reported positive FCF, the EV/FCF stood at close to 22x.

Source: YCharts

With a WACC of 12.55%, the enterprise value would stand at $5.772 billion. In addition, I added cash and cash equivalents worth $978 million and restricted cash of $21 million, and subtracted the current portion of debt close to $23 million, long-term debt worth $4.8 billion. I obtained an implied equity of about $1.9155 billion. Finally, the fair price would be close to $5 per share.

Source: My DCF

The company reported notes that include interest of close to 9.250% and 11.25%. Management may have to make payments to debt holders in 2024 and 2025. With this in mind, I believe that the WACC of 12.55% that I assumed is conservative.

On April 17, 2020, Sabre GLBL entered into a new debt agreement consisting of $775 million aggregate principal amount of 9.250% senior secured notes due 2025. The April 2025 Notes are jointly and severally, irrevocably and unconditionally guaranteed by Sabre Holdings and all of Sabre GLBL’s restricted subsidiaries that guarantee Sabre GLBL’s credit facility. Source: 10-k

Source: 10-k

Risks

Although Sabre is currently positioned in a place of recognition, prestige, and success in its commercial operations, the company also lives with emerging risks in the travel market as well as particular situations of its corporate presence.

In addition to being exposed to a highly competitive market, in which it has not yet managed to position itself internationally as it has done in the United States, Sabre is highly dependent on the operations of its client companies as well as the growth and development of the market. As this industry was brought to a standstill during the Covid pandemic, any similar event could affect it again, and force the company to undergo an accelerated transformation and adaptation.

Besides, the inability to expand its contact with new clients or to retain current clients, due to the appearance of other companies providing better quality services as well as cheaper costs, could complicate the company’s FCF growth.

Finally, any change in the regulation or legality of the use of consumer data for market analysis and marketing strategies could lead the company to an urgent situation in relation to its FCF, commercial activities, and future strategy approach.

Conclusion

Sabre Corporation recently delivered an impressive quarterly bookings increase, and with annual savings and new acquisitions, it intends to deliver positive FCF in 2025. In my view, further reduction in the net debt/EBITDA would most likely interest market participants and may enhance the stock valuation. I do see risks from the total amount of debt and changes in the regulation about data privacy, however I believe that Sabre stock could trade at a higher price mark.

Read the full article here