The worst may soon be over for Samsung Electronics’ (OTCPK:SSNLF) troubled memory chip business. Not only have Korean semiconductor export declines begun easing in May, but recent global semiconductor sales data appears to be bottoming out as well. Any cyclical rebound in memory end markets like PCs and smartphones could well be accelerated should Samsung and its peers move ahead with production cuts post-Q2. The combination of lower production (potentially even capacity cuts) and a demand recovery as the upcoming iPhone/foldable smartphone cycle kicks in could lead to a sooner-than-expected rebound in H2. AI-driven demand for high bandwidth memory and high-density server DRAM, where an SK Hynix (OTC:HXSCF)/Samsung duopoly is taking shape, also bodes well for the economics of the chip business. Samsung’s ~1.4x P/Book valuation, while above historical levels, screens very reasonably relative to key peer Hynix and its net cash position (high teens % of market cap). Key upside catalysts to keep an eye out for include progress on high bandwidth memory production, as well as updates on the capital return.

Cyclical Memory Headwinds are Finally Easing

Korean semiconductor exports may have been down again in May, but the 36% YoY decline was a marked QoQ improvement (up 24% QoQ benchmarked against February numbers). Global semiconductor sales data, as reported by the Semiconductor Industry Association, showed a similar improvement, with the rolling average moving higher yet again in the latest month.

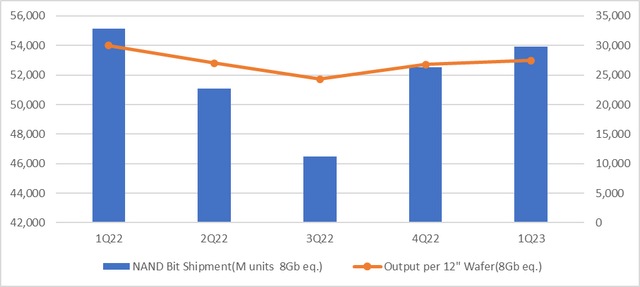

Having been the worst performer in the semiconductor space, memory demand looks poised to lead the cyclical rebound. For one, production cuts by the major players (led by Samsung) present a key inventory restocking catalyst for NAND/DRAM. Assuming an elastic demand curve, lower prices should boost overall industry demand as well, most notably on the hardest-hit NAND side. Samsung’s Q4 2022/Q1 2023, for instance, has already seen a sequential increase in NAND bit shipments; continued traction here bodes well for an earnings rebound.

JP Research

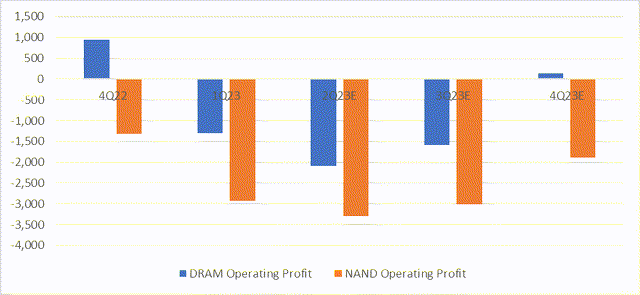

While Samsung is leading the way on industry-wide production cuts, the key question from here will be whether the production cuts (temporary supply headwind) ultimately translate into capex cuts (a structural production reset). Given the extent of the DRAM/NAND losses currently being incurred, the incentive is clear, though the discipline (or lack thereof) the industry has shown over the last year indicates a favorable supply/demand balance is far from a given.

Still, Samsung, as the largest player, is in the driver’s seat and remains well-placed to weather the cycles. Looking ahead, the pace of DRAM/NAND price improvement (in reaction to the cuts) will be key to underwriting a Q3 rebound for the segment. For now, I see a base case of improving DRAM/NAND prices and bit shipments (in response to lower prices) in H2 as the most likely scenario, driving significantly improved memory economics for Samsung.

JP Research

Lucrative New AI Profit Pools Are Emerging

Structurally, the memory business is poised to gain another growth driver from the booming AI server market. For context, AI servers come with specific memory content requirements. Firstly, from high bandwidth memory due to their data speed advantages; the most relevant example currently is Hynix’s third generation HBM3 DRAM co-packaged onto H100 NVIDIA (NVDA) cards. AI servers also come with higher density requirements for the main memory, typically served by the 128GB DRAM module. Both products carry premium price points and competition is limited; thus, the economics are highly favorable, especially in the initial years.

The catch for Samsung is that Hynix is in the lead for HBM3 production, though the company is accelerating its production timeline in response (news flow indicates both are well ahead of MU). Having reportedly integrated its HBM3 with AMD’s MI 300 accelerated processing units, Samsung is clearly moving in the right direction.

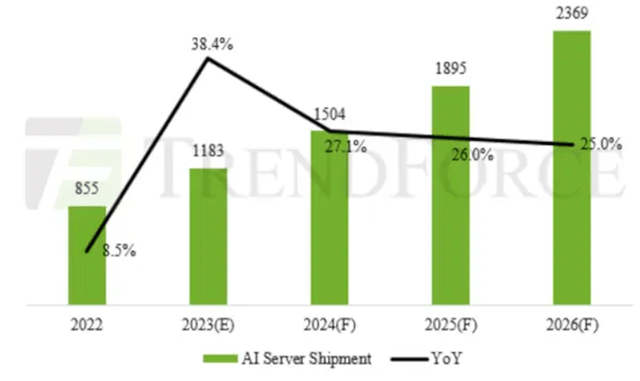

Assuming Trendforce’s forecast for H2 mass production holds true, expect a nice tailwind for Samsung DRAM shipments and pricing post-Q4. Full top-line benefits, on the other hand, are unlikely to accrue until 2024 when Samsung deepens AI server penetration (+29% projected CAGR through 2026 per Trendforce). With MU also trailing on the higher density 128 GB module relative to the Hynix/Samsung duopoly, these high-growth AI profit pools, along with mobile LPDDR5X (Samsung’s energy-efficient/high-performance DRAM for Snapdragon flagships), could more than offset headwinds from PC and server DDR4.

Trendforce

Smartphone Cycle Offers an Additional Near-Term Boost

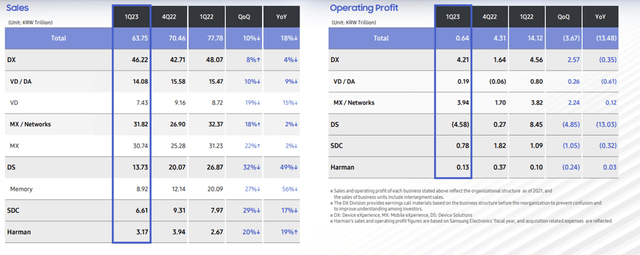

Having served as a useful profit anchor throughout the semiconductor downturn in recent quarters, Samsung’s smartphone division (i.e., ‘MX’ or mobile experience) looks poised for further outperformance. As the Q1 results showed, sales of the Galaxy S23 Ultra flagship series are already off to a good start, boosting blended smartphone pricing and margins for MX. As a result, the division’s operating profit has rebounded to W3.9tn at a ~12% operating margin (~13% for handsets. ~5% for network equipment).

Samsung Electronics

Given the stronger launch (vs. the Galaxy S22) and solid feedback thus far, management’s full-year total sales target of 30m units seems well within reach. Assuming sales can be sustained without compromising on the higher price tag, expect the S23 to be accretive to the operating profit margin. In comparison, current guidance for a smartphone margin of ~10% in Q2 seems conservative. The foldable phone and iPhone 15 releases later this year present incremental tailwinds to the OLED business as well.

Coming Out of the Memory-Driven Doldrums

Having been dragged down by declines in its semiconductor business in Q1, Samsung appears poised for an inflection in Q2 or later in the year. Beyond the improved near-term demand indicators, production cuts are also set to kick in, reversing the steep price declines in recent months. Alongside a structural AI-driven demand boost, all signs point to an eventual reversal for the memory chip business. In the meantime, the smartphone and display businesses are also poised to benefit from the upcoming Galaxy foldable/iPhone cycle. And with cash generation potentially surprising to the upside, higher capital returns could well be on the cards. Having lagged key peer Hynix and other AI plays this year, the Samsung rally still has legs, particularly with the stock still priced very reasonably at ~1.4x book.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here