I’ve been very loud (and, so far, wrong) about my distrust for market-cap weighted passive vehicles at this point in the cycle. Yes – they’ve done exceptionally well over the past year and a half, but now are at the point where they are not only massively overvalued, but massively overcrowded.

Still – I recognize that this can continue.

And if it does, then one play to play residual strength is through the Schwab 1000 ETF (NYSEARCA:SCHK). This ETF tracks the Schwab 1000 Index, which is a modified, float-adjusted, market-cap-weighted index composed of the largest 1,000 publicly traded U.S. companies. The fund’s portfolio essentially holds the same names as this benchmark, offering investors a combination of large-cap juggernauts and market leaders.

I view this no different from the S&P 500 (SP500) or Russell 1000. This is in that large-cap equity ETF club, where there isn’t much differentiation among low-cost providers other than brand name. Because the fund tracks only the largest companies, the top end of its market‑cap spectrum includes all the familiar names. It also means SCHK has a heavy bias towards mega-cap tech stocks.

And that’s the problem.

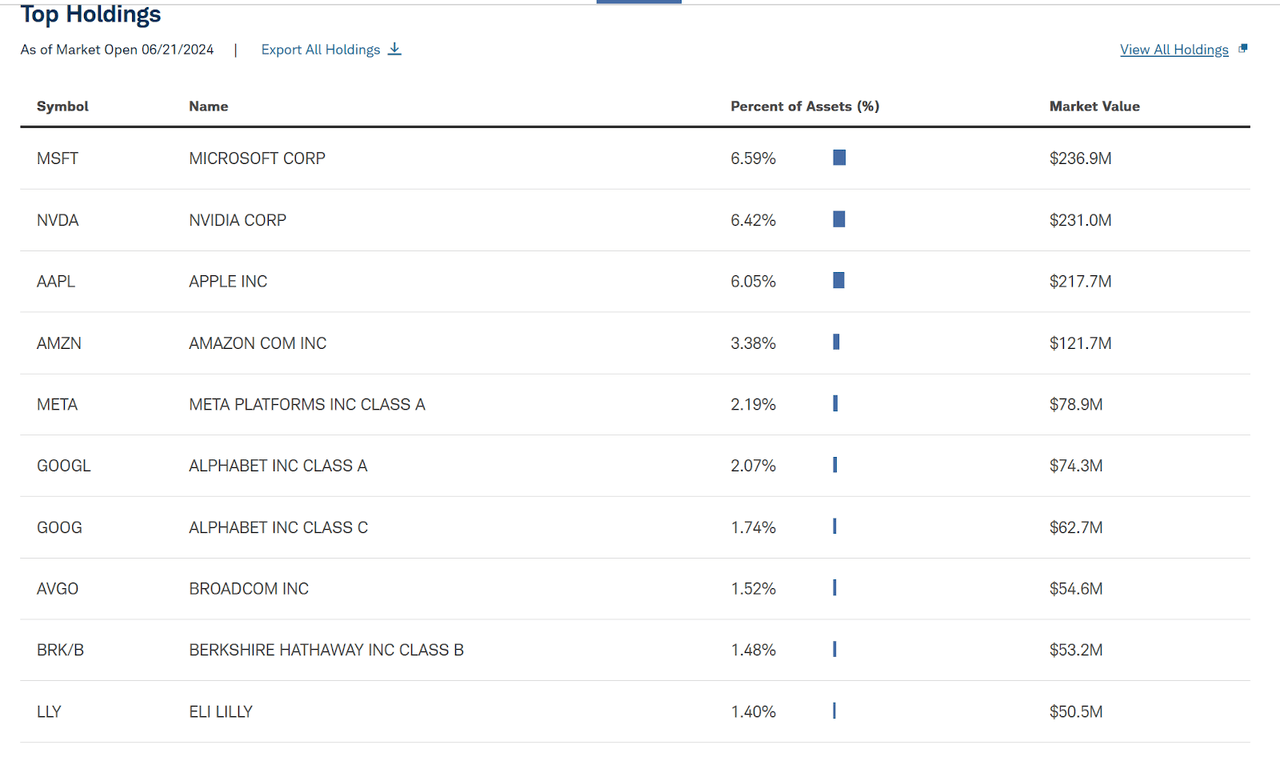

A Look At The Holdings

I wish there were more I could write about this, but there’s not much to add. It’s all the names you know, and which you likely already own with any other market-cap weighting average.

schwabassetmanagement.com

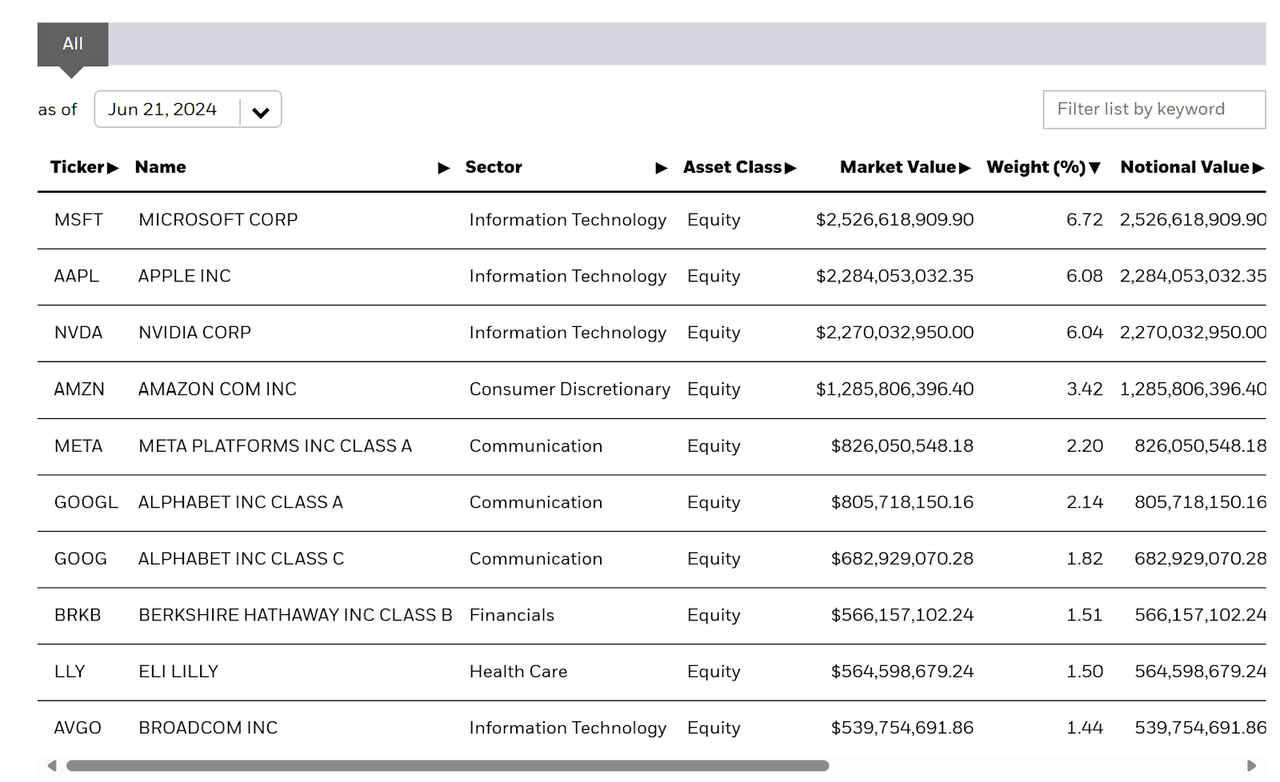

Contrast this to the iShares Russell 1000 ETF (IWB) holdings and, while there are some slight differences in weighting, it’s mostly the same thing.

ishares.com

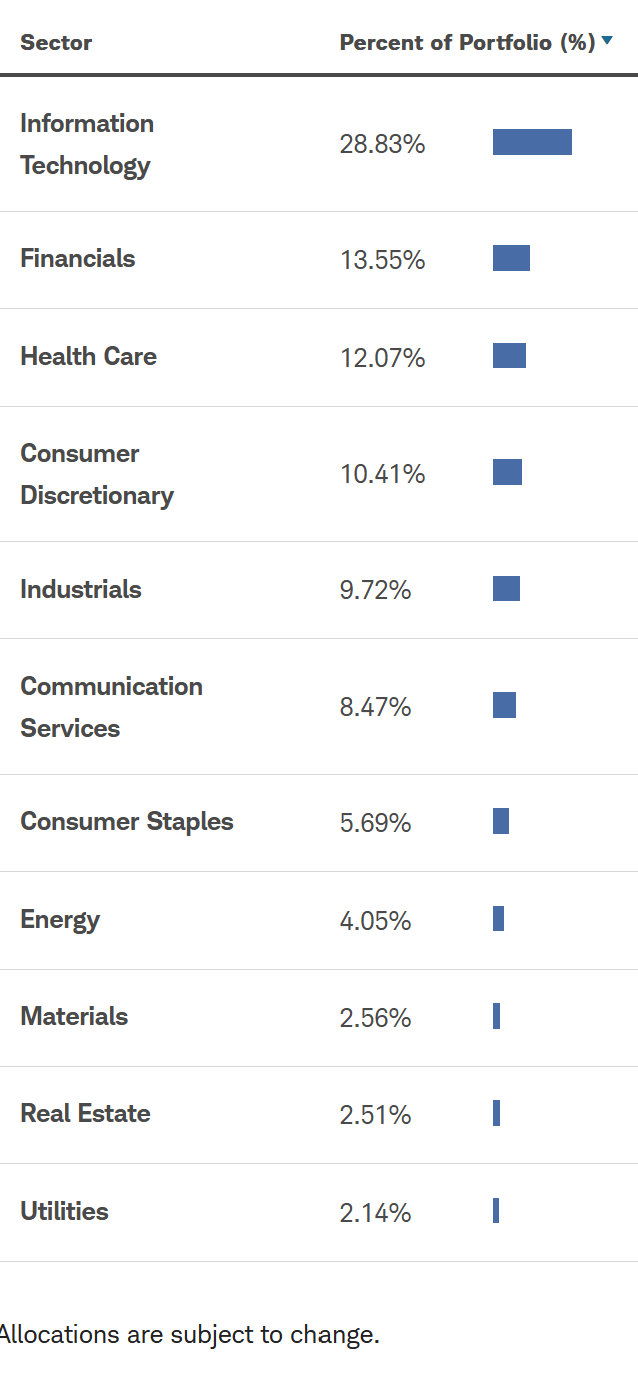

Sector Composition

With all the top 10 being the familiar holdings, the sector composition weightings are familiar as well.

schwabassetmanagement.com

The biggest sector is Information Technology, which accounts for 28.83% of SCHK’s total assets. In light of the high concentration of tech titans among its biggest holdings, this is not really a surprise. Nonetheless, it highlights the fact that SCHK’s portfolio – due to the relatively large weight of the tech sector – might be vulnerable to excessive volatility, given that the tech sector is characterized by cyclicality and subject to disruptive innovations.

Next up is the Financials sector, which makes up 13.55% of the portfolio, which reflects the fund’s exposure to the banking, insurance and investment world, while Healthcare, made up of drug and medical device drug manufacturers, makes up 12.07% of the portfolio.

Again – no different from what you expect from a broad market-cap weighted US fund.

Peer Comparison

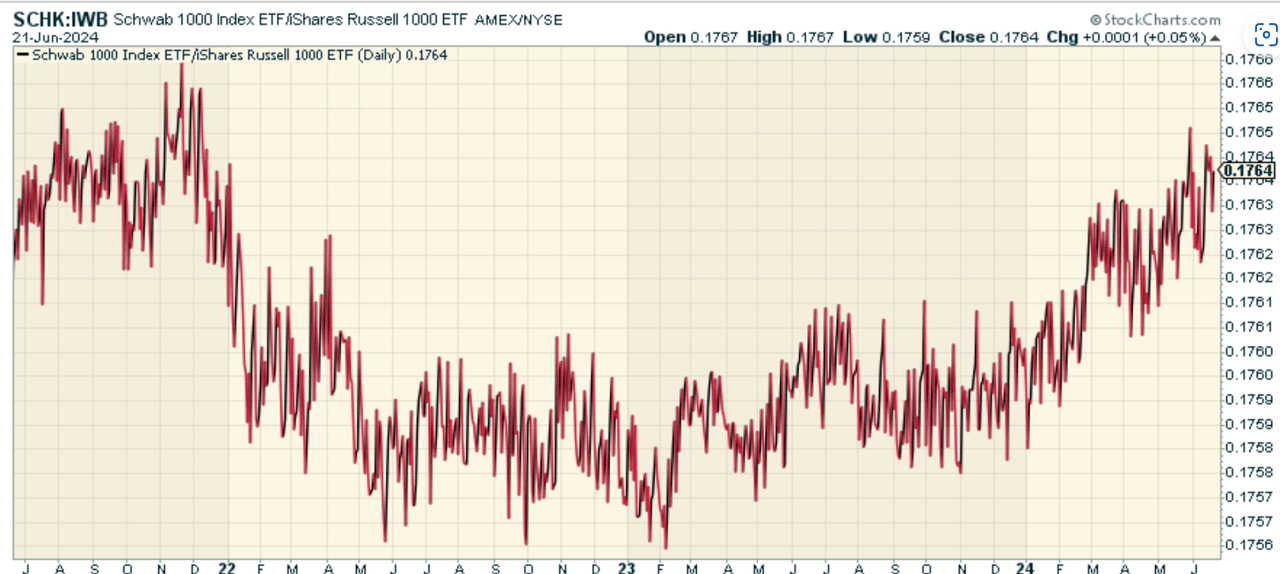

I mentioned the holdings of IWB earlier, and this is the fund that makes the most sense to compare SCHK to. IWB mirrors the Russell 1000 Index. IWB has a fee of 0.15%, while SCHK is at 0.05%. When we look at the price ratio of SCHK to IWB, we find that, no surprise, the two have performed in line with each other.

stockcharts.com

Pros and Cons

On the positive side, SCHK’s portfolio construction offers some of the supposed benefits of index investing. By focusing on the largest 1,000 companies by market capitalization, SCHK exposes you to a well-diversified basket of industry leaders, with many of these companies having strong balance sheets, well-established brands and robust business models. And for that reason, it could potentially offer lower volatility and downside risk than many small- and mid-cap shares.

Beyond that is the fact that SCHK offers an ultra-low expense ratio of just 0.05%, which will appeal to investors who are price-sensitive and want to maximize their long-term returns. On long-term horizons, tiny differences in fees can grow into meaningful sums, and eat into profits.

The problem for me is the cycle. Because it holds the market’s largest stocks in disproportionate amounts, benchmark-beating periods will often come at the expense of lagging times when smaller companies dominate returns. The fund’s tilt towards tech will exacerbate volatility because that sector is cyclical.

Conclusion

There’s nothing wrong with Schwab 1000 ETF at all. It’s just no different from any other market-cap weighted product. For core equity exposure? Sure – it’s great. But is it different? Not at all. If your objective is simply to get a broad market proxy, SCHK is solid. I just don’t favor large-caps here and think there are more undervalued investments out there.

Read the full article here