One company that I became bullish on in March of this year was Science Applications International Corporation (NASDAQ:SAIC). I don’t dabble too much in the defense and technology industry that the company plays in. But every so often, I do find some attractively priced businesses in this space. At the time that I wrote my article in March, I acknowledged that the company had been experiencing mixed financial performance. Revenue had been fluctuating, but profits were impressive. Add on top of this how cheap shares were compared to similar businesses, and I felt as though it warranted a ‘buy’ rating.

In the months since then, the company has unfortunately underperformed my expectations. But that underperformance is not terribly significant. While the S&P 500 is up 7.1%, shares of Science Applications International have risen by 5.8%. Much of this improvement in share price came from a 4.7% jump that the stock experienced on September 5th after management announced financial results covering the second quarter of the company’s 2025 fiscal year. Management exceeded analysts’ estimates when it came to both revenue and adjusted profits. Unfortunately, GAAP earnings per share fell short of guidance. Having said that, the company showed a return to growth from a revenue perspective and cash flows, while down year over year, are still high enough to make the company cheap on a relative basis. Given these factors, I think that keeping the company rated a ‘buy’ makes a lot of sense right now.

A play that has nice potential

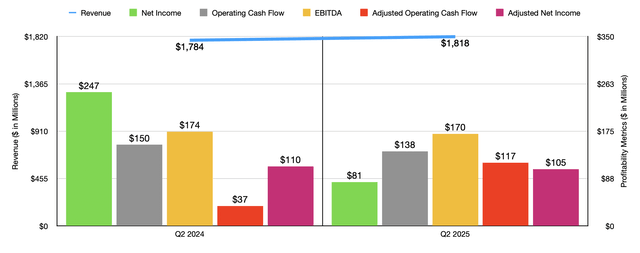

For the second quarter of the 2025 fiscal year, the management team at Science Applications International was able to generate sales of $1.82 billion. That’s an increase of 1.9% over the $1.78 billion the company generated just one year earlier. While this increase year over year might not seem significant, it is worth noting that the revenue reported by the company ended up being $30 million greater than what analysts anticipated. Even though the company suffered from the completion of certain contracts, this pain was more than offset by a ramp up in volume involving existing contracts. New contracts also contributed to the company’s top-line expansion.

Author – SEC EDGAR Data

On the bottom line, the picture is more complicated. Earnings per share came in at $1.58. This is down from the $4.56 per share reported one year earlier. And it also happens to be $0.17 below what analysts had forecasted. The second quarter of last year was significantly higher because of a $240 million gain on certain asset sales. This resulted in the company generating profits of $247 million for the second quarter of 2024. This year, profits were $81 million. Once we made certain adjustments, though, the company did quite well. The $2.05 per share that management reported matched what the company experienced the same time in the 2024 fiscal year. This resulted in adjusted net profits of $105 million, which was only slightly below the $110 million reported for the same time in 2024. By comparison, analysts had been expecting adjusted earnings per share to be about $0.20 lower than what they ultimately came in at.

Author – SEC EDGAR Data

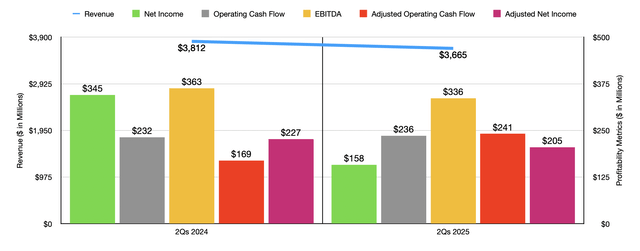

There are other profitability metrics for us to pay attention to. And in some respects, these are even more important than earnings and adjusted earnings. One of these would be operating cash flow. This declined year over year from $150 million to $138 million. If we adjust for changes in working capital, however, we get a surge from $37 million to $117 million. Meanwhile, EBITDA for the company dipped slightly year over year, pulling back from $174 million to $170 million. In the chart above, you can also see financial results covering the first half of 2025 compared to the same time of 2024. For the first half of the year as a whole, revenue actually decreased. Profits were down and EBITDA also dropped. However, operating cash flow and adjusted operating cash flow both increased.

Science Applications International Corporation

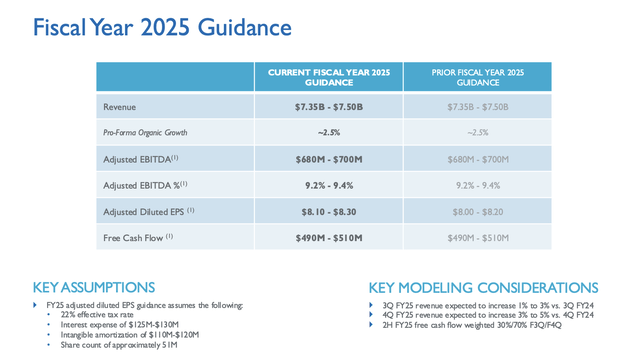

When it comes to the entirety of the 2025 fiscal year, management anticipates revenue of between $7.35 billion and $7.50 billion. At the midpoint, this would be 0.3% lower than the $7.44 billion the company reported for 2024. It also matches the prior guidance that management forecasted for the fiscal year when they announced financial results for the first quarter. Other guidance figures have changed, though. Most notably, management had previously thought that earnings per share, on an adjusted basis, would be between $8 and $8.20. Both the low end and high end of that range have now been pushed up by $0.10. At the midpoint, this would translate to adjusted net income of $419.8 million. Guidance has remained unchanged for operating cash flow, with management saying that it should come in at between $520 million and $540 million. The same can be said of EBITDA, which is forecasted to be between $680 million and $700 million.

Author – SEC EDGAR Data

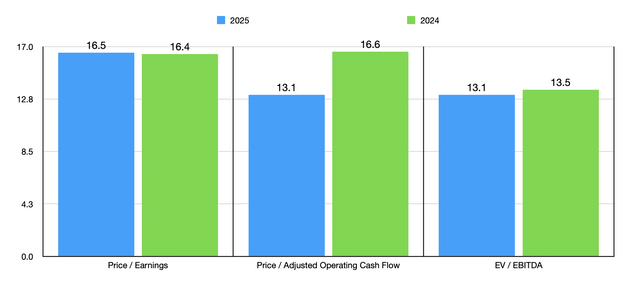

Using these figures, we can see in the chart above how shares of Science Applications International are currently priced. With the exception of the price to operating cash flow scenario, the multiples for the business are not materially different from if we were to use figures from the 2024 fiscal year. Normally, the multiples that we are seeing would be indicative to me of a company that is fairly valued, not undervalued. But the space that the company operates in is known for trading at very lofty multiples. Some of my optimism is based on this. In the table below, for instance, I compared Science Applications International to five similar companies. And using each of the three valuation metrics, it ended up coming in as the cheapest.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Science Applications International Corporation | 16.5 | 13.1 | 13.1 |

| Leidos Holdings (LDOS) | 48.8 | 14.0 | 20.4 |

| KBR (KBR) | 45.1 | 29.3 | 17.8 |

| CACI International (CACI) | 25.8 | 21.8 | 15.3 |

| Parsons (PSN) | 217.6 | 21.3 | 38.1 |

| Booz Allen Hamilton (BAH) | 33.6 | 53.1 | 19.1 |

There are some other positive attributes about the company. For starters, management is allocating capital toward rewarding shareholders directly. During the second quarter, the company paid out $19 million worth of dividends. But more impressive was the fact that this was in addition to $201 million of share buybacks. This brings total share repurchases to $304 million for the first half of 2025. That’s well above the $190 million worth of stock repurchased the same time one year earlier. Even though it’s not terribly significant, the firm did also see a slight improvement in backlog year over year. It rose from $22.76 billion in the second quarter of the 2024 fiscal year to $22.90 billion the same time this year.

Science Applications International Corporation

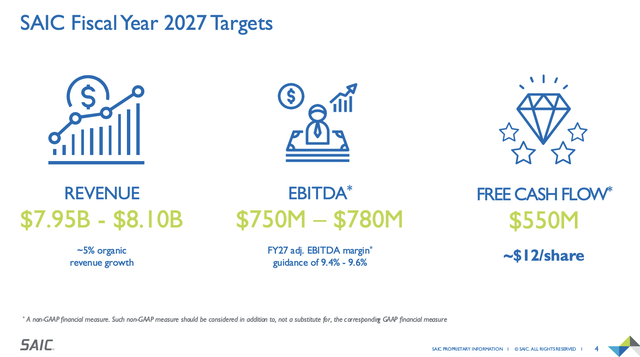

Moving forward, management also has plans for the business. If everything goes according to plan, management expects the new growth after the 2025 fiscal year to be about 5% on an organic basis. This will allow the company to grow revenue to between $7.95 billion and $8.10 billion by 2027. By that point, the company expects to be generating EBITDA of between $750 million and $780 million on an annualized basis. This translates to an EBITDA margin of between 9.4% and 9.6%. This is only slightly better than the 9.3% the company should achieve this year. If we assume that the company should trade at the same EV to EBITDA multiple that it’s currently trading at when that occurs, and if we assume that net debt remains unchanged between now and then, this would imply total upside from now through the end of 2024 of only 14%. But if we take some other assumptions, the picture looks quite a bit different.

If we remove the clear outlier that is Parsons when it comes to the EV to EBITDA valuation approach, the average of the EV to EBITDA multiples for the other five comparable businesses ends up being 18.2. Applying this to the midpoint of guidance for EBITDA for 2027 should translate to upside for shareholders of 69.8%. That’s about 25.5% on an annualized basis. Now, in the image below, you can see that Science Applications International ranks roughly even or slightly worse with Wall Street analysts and Seeking Alpha’s Quant Rating system than these other companies do. But even if we assume that the company should trade at the EV to EBITDA multiple of the cheapest of the five competitors, we still have annualized upside of about 14.9%. That’s greater than the 11% to 12% that the market achieves, on average, over the long run.

Seeking Alpha

Takeaway

Based on the data provided, I must say that things seem to be going quite well for Science Applications International right now. The company exceeded estimates when it came to revenue and adjusted earnings per share. Management plans to grow the company further and the stock is cheap on a relative basis. Shares are also not terribly priced when looking at the picture in a vacuum. Add all of this together, and I do think that keeping the company rated a ‘buy’ is logical at this moment in time.

Read the full article here