One Of The Greatest Secular Growth Trends

Over the last few years, we’ve spent a great deal of time discussing the idea that the growth of the digital ad market is arguably one of the greatest secular growth trends of our time.

In 2020, I specifically discussed this idea with you in “The Greatest Secular Growth Trends 1,” which you may read via the link below:

- This Is One Of The Greatest Secular Growth Trends

- As something of an aside, I highlighted therein that the digital ad revolution was principally an AI and machine learning revolution in that engineers were building AI-driven advertising marketplaces.

In TGSGT 1, I specifically highlighted that ecommerce marketplaces would be arguably the greatest beneficiaries of this revolution in the 5 to 10 years ahead. I wrote,

I am grouping the two of these (Sea Ltd. (NYSE:SE) & MercadoLibre (MELI)) together because they fit under one umbrella of advertising.

Just as Amazon’s (AMZN) ad business has begun to explode, so too, will these companies’ ads businesses explode at some point in the next 5-10 years.

In fact, I would say that very few people who own these companies are accounting for the explosion in ad revenues that will be generated once these platforms, i.e., MercadoLibre’s primary e-commerce platform and Sea’s Shopee platform, mature and achieve the status and dominance required to execute a robust ads business.

If you read MercadoLibre’s financial reports, you will see that they’ve begun to include discussions of their advertising platform. As you will see in the next section, the advertising component of these marketplaces cannot be overstated. Though I am not recommending Alibaba as an investment, I do find its business model very interesting. In China, Baidu search is not a strong business. It’s not a great stock to own, and the company has a terrible reputation in China.

Instead of searching on Baidu, Chinese citizens search on Alibaba. This drives massive ad dollars to the platform and away from Baidu, as evidenced by its stagnant revenues.

The same dynamic takes place on Amazon, and in the future, the same dynamic will take place on Sea and MercadoLibre.

So buy these companies for their business models today, but remember, that these will be digital ad giants in the next ten years. The next section on Amazon truly highlights that ad dollars are where the money is at; not retail, nor payment wallets.

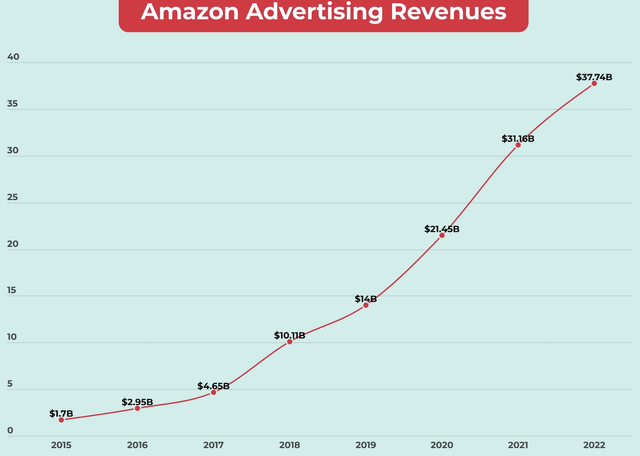

The Growth Of Amazon Advertising Revenues

Four Week MBA

At the time in 2020, MercadoLibre’s ad sales were not being broken out, as they were quite diminutive.

Today, MercadoLibre’s ad sales have achieved fairly incredible heights, with the company now generating digital ad revenue of about 1.6% of quarterly GMV. In MercadoLibre’s most recent quarter, it achieved $10B of GMV, which indicates that its digital ad revenues were $160M in the quarter.

This represents a $640M annualized digital ad revenue run rate for MercadoLibre, and these ad sales grew at over 60% in Q1 2023.

Were this segment of MercadoLibre’s business a standalone company, it could fetch between $10B and $20B in enterprise value, based on its scale, growth rate, runway for growth [TAM], and margins structure

Further, these are very high margin revenues that will serve to push up on MercadoLibre’s ecommerce margins over time. With these ideas in mind, I recently wrote,

MercadoLibre has made material progress on its digital ads business.

In 2021, it was only .4% of GMV, and GMV was much smaller than what it is today.

Today, not only has MercadoLibre grown its ad business, but also it’s grown its GMV materially.

Today, MercadoLibre’s ad business is 1.6% of $10B worth of quarterly GMV, and MercadoLibre’s ad business grew at over 60% in Q1 2023.

This suggests that MercadoLibre’s ad business currently generates about $640M in annualized, 80% gross margin sales, and this is likely growing at well over 50%, in the midst of an economic environment where ad spending has entered a state of paralysis, relatively speaking.

Source

Turning to Amazon, I originally began highlighting the growth of Amazon’s digital ad business in 2018, and, since then, Amazon’s digital ad business has 4x’d.

I’ve now been a part of two ecommerce businesses experiencing hockey stick growth of their digital ad businesses, and I am quite confident that Sea Ltd. (SE) will be next (with Coupang (CPNG) also set to experience similar growth in its digital ads business).

In this vein, I recently remarked,

Sea Ltd. will likely do billions in high margin digital ad sales.

The net present value of these sales alone likely justifies the company’s current valuation.

Even with lower market share than its current ~50%, it could build a huge digital ad business (note that MercadoLibre only has 35% market share in LatAm; no fevered panic).

As I said, even with a substantially lower market share, Sea could build a fairly giant, multi-billion dollar, high margin revenue digital ad business in the next 5-10 years.

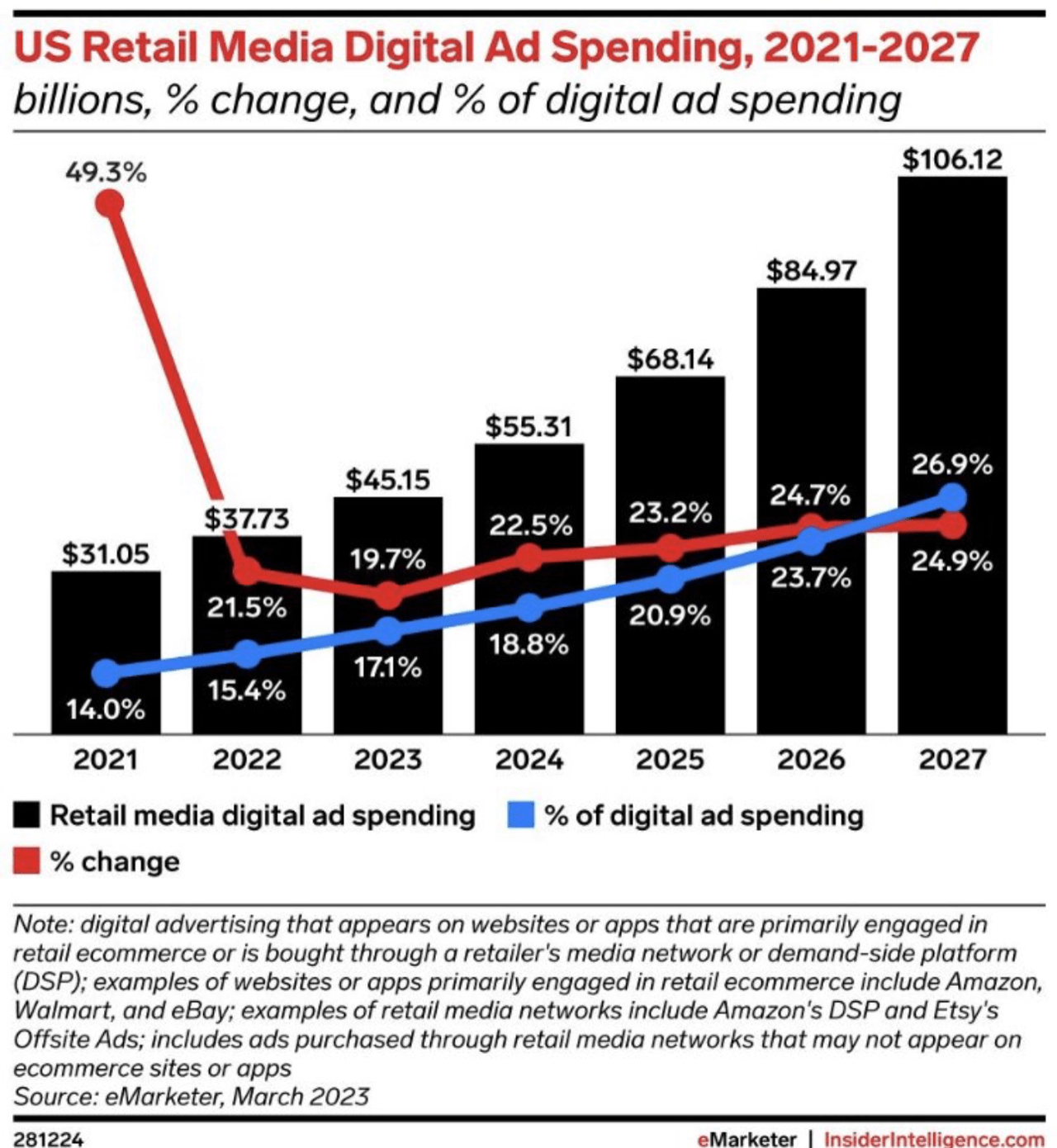

It is difficult to find data for international ecommerce digital ad spend; however, we can see the exceptional growth of this subset of the digital ad market via the graph below, which depicts U.S. digital ad spend on ecommerce platforms, such as Amazon (AMZN) and Walmart (WMT). These, of course, are analogues to MercadoLibre (MELI) and Sea Ltd.

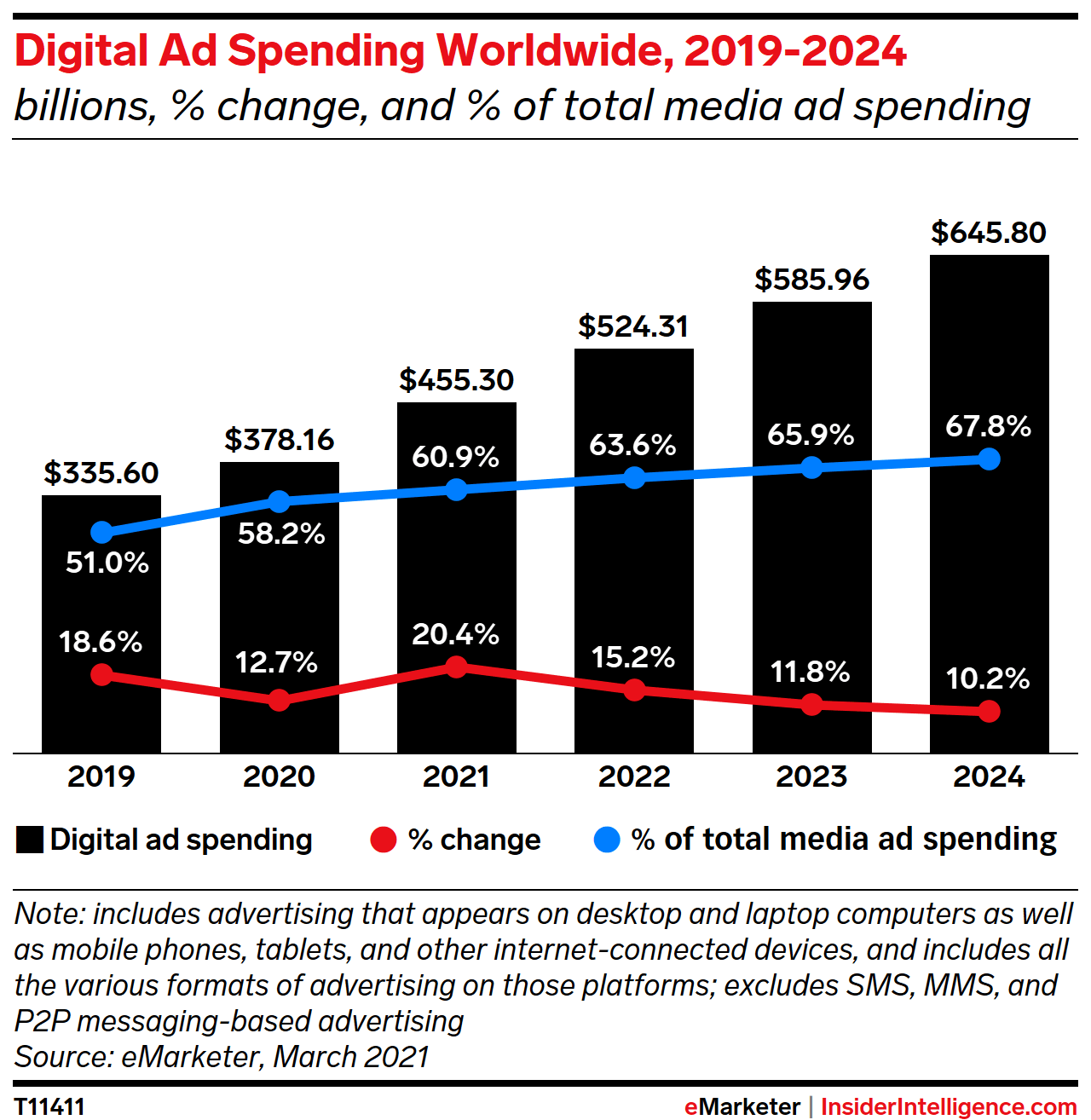

Growth Of Total Digital Ad Spend Worldwide

eMarketer

And, of course, this is a subset of the overall digital ad market worldwide, which is set to grow at healthy rates for many years to come.

Growth Of Total Digital Ad Spend Worldwide

eMarketer

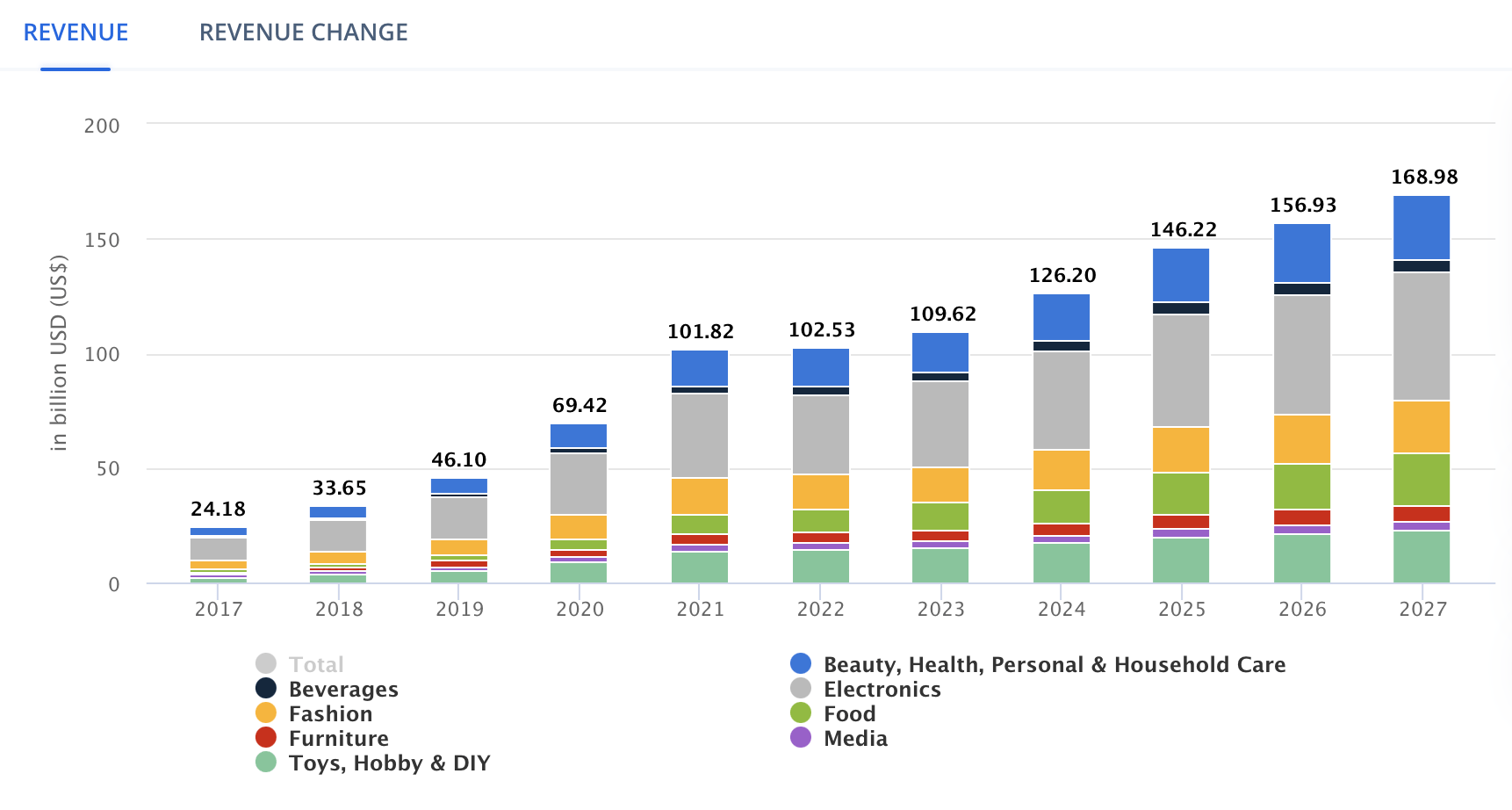

Sea Ltd. Digital Ad Revenue Estimates

Presently, Sea has roughly 50% market share of the total $100B in GMV in ecommerce spend in SE Asia in 2023.

Statista

Were Sea to follow in MercadoLibre’s footsteps, which, as a reminder, only has 35% market share in Latin America’s ecommerce market, and generate 1.6% of total GMV in digital ad revenues, it would generate $3B in high margin digital ad sales based on only its GMV today.

At about $23B in enterprise value, Sea’s entire valuation would be justified by the net present value of these digital ad cash flows. Even at 30% market share, 1.6% of $30B in GMV would likely justify today’s entire enterprise value, considering SE Asia’s (the region as a whole) ecommerce GMV will likely grow at elevated rates for decades and decades to come.

Note that Sea’s conglomerate also includes:

- Garena, a gaming platform that hosts 500M+ users and generates ~$1B in annualized cash flow

- Sea Money, a FinTech platform, with ~60M users, which generates about $2B in profitable, annualized sales as of today

- Shopee Logistics

- Future products that Sea will create and launch. It has built this incredible, diversified conglomerate in just about 13 years. Likely not done!

Based on Sea’s current valuation, we’re getting all of the businesses for free.

Concluding Thoughts: There’s 10 Baggers All Around Us And Nobody Wants To Buy

I don’t believe any of these ideas are controversial. Everybody and their mothers agreed on these statements of objective fact over the last five years with respect to Sea.

Incredibly, in the blink of an eye, the market has experienced a severe bout of amnesia and no longer sees these realities.

But, as we know quite well, the market has a curious especial predilection for hating the best businesses to own long term. It hated Walmart. It hated Lowe’s. It hated Amazon. It hated MercadoLibre, once upon a time.

Why should Sea be any different in the process of defining ecommerce in SE Asia?

In short, I still think Sea is arguably the most attractive public company on earth today, into which very real money can be invested (by which I mean it’s arguably one third of a SE Asian tech oligopoly with an outrageously large net liquidity position and nearly 1B active users across its platforms. It’s not a small, dubious enterprise. It’s massive, dominant, and established, and it could generate 20-40% annualized returns in the decade ahead with relative ease).

Thank you for reading, and have a great day.

Read the full article here