In my previous piece, I looked at whether US investors should hedge their currency exposure when investing internationally. That piece elaborated on the complexity and risk borne by US investors who want to invest in international stocks and do so on an unhedged basis.

In this piece I want to ask a more fundamental question about whether US investors need international stocks at all in their portfolio. Conventional wisdom in the industry says yes, including international stocks is a no-brainer for investors. But the evidence seems to demand a different conclusion. Ultimately esoteric discussions are meaningless unless we can form a conclusion that will affect how investors should be allocating capital today.

In this piece, I will lay out the argument traditionally used to support the idea that international stocks need to be in your portfolio. Then we will take a look at the evidence from real market returns over long periods. Finally, I will conclude with practical insights on how you can design a portfolio to optimize alpha, and whether international stocks should be a part of that portfolio.

The Argument for International Diversification

The argument for international diversification goes something like this. The world economy has changed, overweighting the US is merely home country bias, one should own each country at market weight, and take the return that comes from the global stock market. Proponents of international investing will also tell you that international stocks are cheap relative to their US counterparts, and not having access to high-growth markets, especially in the emerging world, will be detrimental to your long-term returns.

When making decisions within an evidence based (EB) framework, as I do as EB Investor, I want to look at the longest data set available. The arguments for adding international stocks will accuse those who do not include them of recency bias, claiming that we are only looking at the last 15 years of US outperformance.

But in reality, the US has outperformed for a lot longer than that. Many of the arguments that are pro adding international stocks look at short, isolated periods where international stocks have outperformed the US. This is really cherry-picking data to form fit to your preconceived ideas that international diversification is good, without the evidence to back the assertion, as most in the financial community tend to believe. I demur. Here is why.

The Evidence

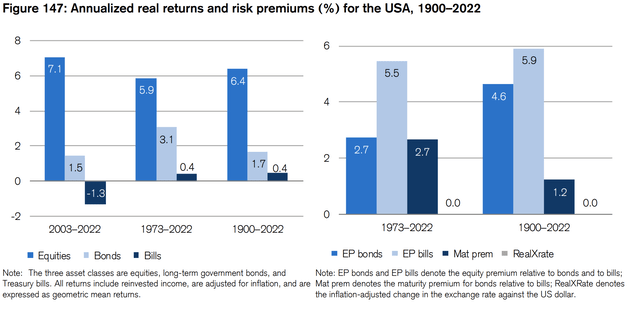

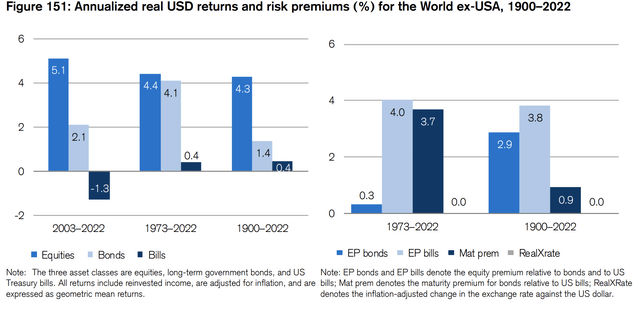

When we look at the data set presented by Dimson and Marsh that looked at the returns from global stock markets from 1900-2022, they found that stocks in the World Ex-USA market returned 4.3%, while US stocks returned 6.4%. This means that for one hundred and twenty-two years, US stocks have beaten their international counterparts. Think about that for a moment. The US also won in the sub-periods tested, from 1973-2022, and 2003-2022.

Credit Suisse Global Investment Returns Yearbook 2023

Credit Suisse Global Investment Returns Yearbook 2023

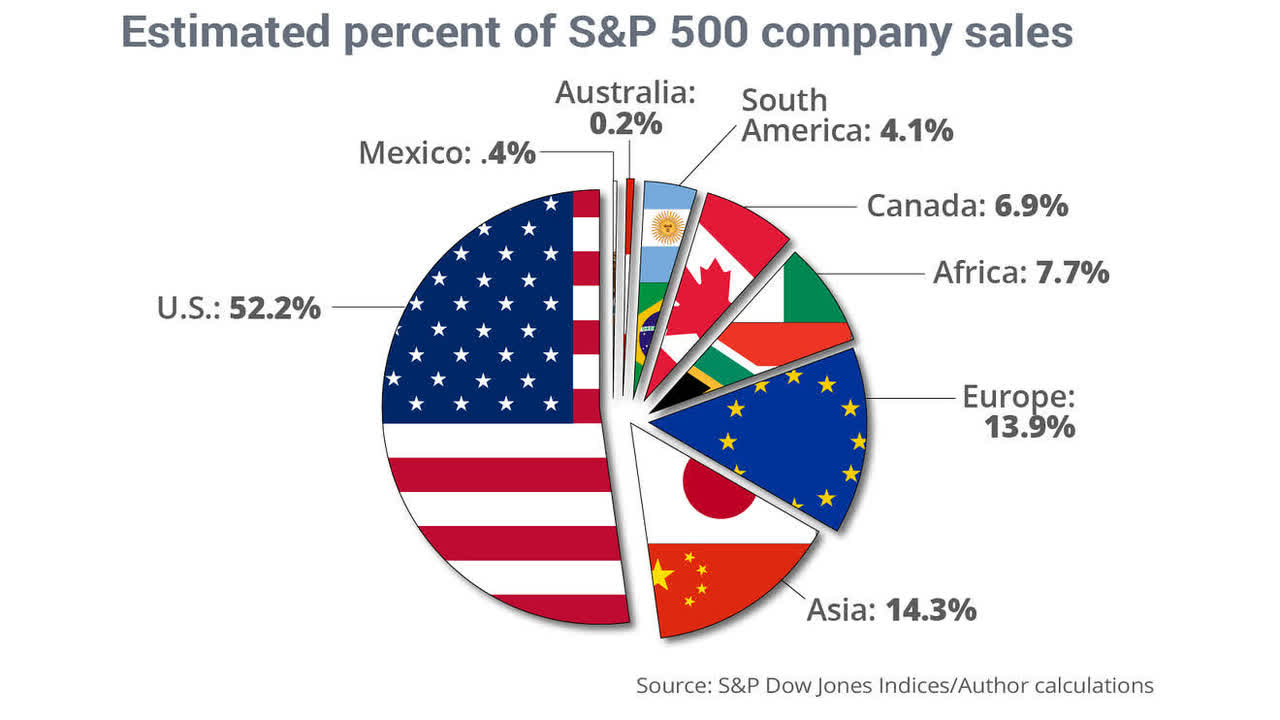

The pro adding international stocks camp also fails to consider the extent to which US stocks have diversified their revenue beyond our shores. Currently, 47.8% of the revenue for S&P 500 companies is from international markets. This means that these companies are increasingly providing access to the international consumer, and the growth in international markets without leaving the US stock market.

MarketWatch

Factor Investing: International Value and Small Cap Premiums?

Then there is the argument of factor investors who declare that the reason the US outperforms is because we are not looking at small-cap and value stocks in international markets. When we look at the data available which goes back 28 years (1995-2023), we find that international small-cap and value stocks fail to out-perform their US peers, or the US stock market as a whole, producing returns of 9.59% for US Small Cap, and only 6.38% for international small cap, with the total US market producing a return of 10.12%.

Portfolio Visualizer/Author’s own Calculations

Value stocks had a similar outcome of international underperformance with international value stocks producing returns of 5.42% vs its US counterpart of 9.35%.

Portfolio Visualizer/Author’s own Calculations

Evidence From Emerging Markets

Then there is the question of emerging markets, where many have told us that the growth of the future will come out of EM and thus, we need to hold a percentage of our portfolio in emerging markets stocks to capture this rapidly growing part of the world. The same arguments apply here, as they do to international developed stocks. US companies offer access to these high-growing markets without leaving the legal protections, and safety of US markets. There is similarly no premium in returns when looking at EM stocks.

Portfolio Visualizer/Author’s own Calculations

EM stocks produced a return of 5.37% vs 10.12% for the US market. Not only are there not any premiums but international stocks have actually detracted from investor returns over long periods of time, as evidenced by the Dimson & Marsh data above.

Conclusion

So how does this impact us today, in the decisions we make about allocating capital? Surely international stocks are far cheaper than their US counterparts. Many are convinced they are about to experience a period of outperformance relative to the US. If you decide to include international stocks understand that you are investing in both the companies as well as their currencies, which has increased overall portfolio volatility. There is no way of knowing in advance what the future brings, and which stocks will outperform in the decade ahead.

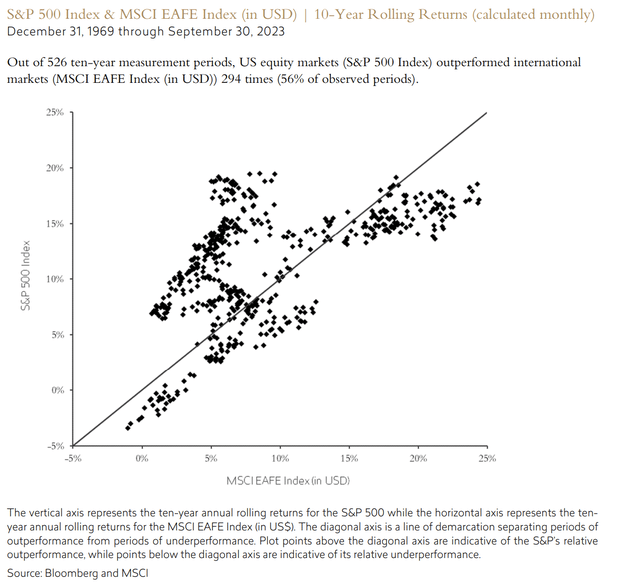

A more favorable analysis of international stocks was performed by Tweedy Browne & Co. They looked at 10-year tolling returns from 1969-2023 (54-years) showing the US beat international stocks a mere 56% of the time.

Tweedy Browne & Co.

The chart above shows a more balanced record between international and US stock outperformance. This supports my overall contention, based on the evidence, that international stocks tend to outperform over short bursts of time. Including those periods will skew the results when they are looked at in an isolated period of time, even over decades as this analysis does. It allows the momentary bursts of outperformance to count for more of the total record than when you look at a larger data set, over a century or more.

The overall record from over a century of data shows international stocks have underperformed their US counterparts. The evidence is clear that investors like Warren Buffett and Jack Bogle, who dismiss the need for international stocks, are well supported in doing so.

Read the full article here