I recently wrote an article on HYG, a total junk bond market ETF. I rated it a Sell and discussed that junk bonds are artificially overpriced. While researching HYG and the junk bond market, I saw something that concerned me. There is an approximately $785 billion junk-bond maturity wall that the junk bond market is getting very close to. These junk-rated companies are having to scramble to refinance, but because of interest rate hikes, that isn’t easy.

This didn’t affect HYG too much because it has a longer average maturity, but it did cause me to develop an extremely bearish outlook on short-term junk bonds. iShares 0-5 Year High Yield Corporate Bond ETF (NYSEARCA:SHYG) (as the name suggests) holds 0-5 year corporate junk bonds. SHYG has an impressive 30-day SEC yield of about 8.1% and AUM of around $5.5B. I worry that due to high rates, some of these companies will not be able to refinance. I rate SHYG a Sell.

Holdings

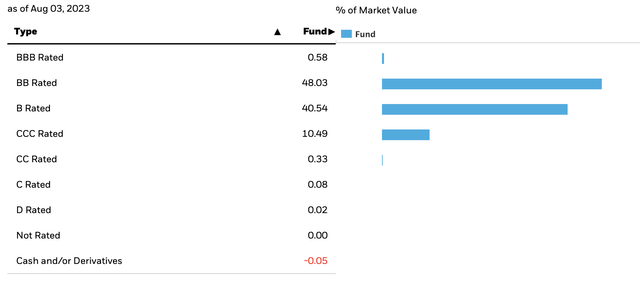

SHYG holds 860 individual junk bonds that have maturities between 0-5 years. Its largest holding is in BB rates bonds, making up about 48% of the ETF. CCC-rated bonds and below make up a little under 11%.

SHYG’s holdings by credit rating (ishares.com)

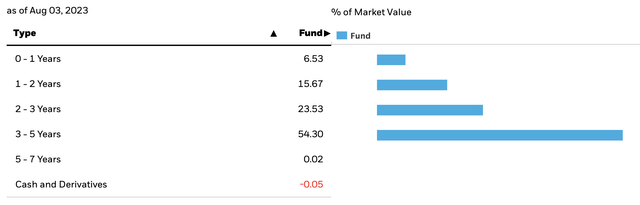

SHYG’s holdings are skewed to the longer end of maturity. Its average maturity is about 3.1 years. Over 54% of its holdings are in junk bonds with a maturity between 3-5 years.

SHYG’s holdings by maturity (ishares.com)

Overpriced bonds

In my article on HYG, I argue that junk bond prices are artificially overpriced. This is an issue for the entire junk bond market, not just HYG. Junk-rated companies have cut back on issuing bonds. Junk bond issuance is down 13% since its peak in 2021. Junk bond funds have to continue to buy junk bonds so they can accurately reflect the index. The supply has shrunk, but the demand has stayed the same. While this overpricing affects SHYG, it isn’t the main reason for my Sell thesis. Because of that, I’m going to leave my reasoning for junk bonds being overpriced at that. If you want a more detailed analysis of this, I go into depth on this issue in my HYG article.

Maturity wall

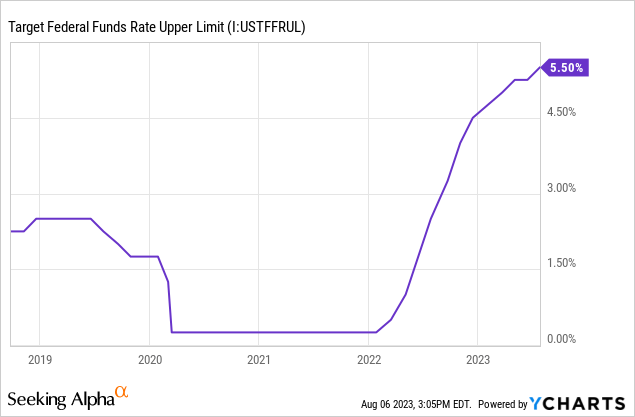

Now is not an easy time to borrow money. The Fed funds rate is higher than it has been since 2001. We are approaching a $785 billion junk-bond maturity wall. The bonds contributing to this have on average 4.7 years to put new financing in place. Normally, this should be easy, simply issue new debt. However, the era of easy borrowing is over. The chart below shows the Fed funds rate over the past several years.

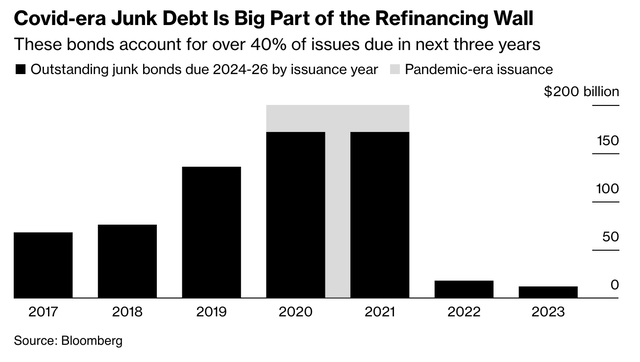

When the COVID-19 pandemic hit, the Fed cut interest rates to practically zero. This made borrowing money very cheap. Junk-rated companies took advantage of this. Over 40% of the $785 billion junk-bond maturity wall was issued during the pandemic. The image below shows how much debt due between 2024 and 2026 was issued by year.

Covid-era junk debt issuance (Bloomberg)

About $170B was issued in both 2020 and 2021, making the total issuance during the pandemic-era $340B. Rate hikes started in early 2022. In 2022, only about $18B of junk bonds were issued, a 90% decrease from the year prior (this supports my overpricing argument above). So far in 2023, only $12B has been issued. Taking advantage of low rates is a good thing in most cases; however, having to refinance all the debt that was taken on in a low-rate era when rates are high can really hurt a company that is already a high credit risk.

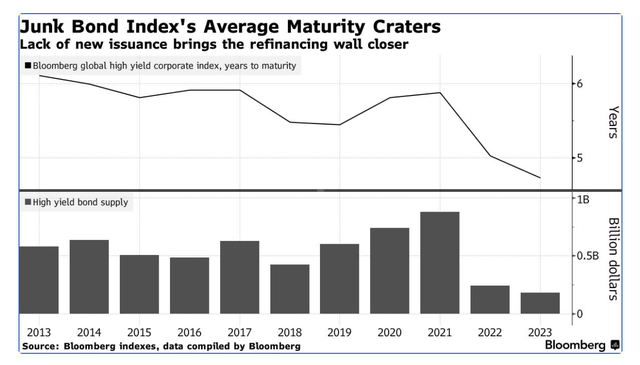

Average maturity plunge

The image below shows the junk bond index average maturity. In 2021, the average maturity plunged quickly from about 6 years to about 4.5 years.

Junk bond index average maturity (Bloomberg)

As the bottom half of the image shows, while this was happening the bond supply shrunk (again, adds to my overpriced argument).

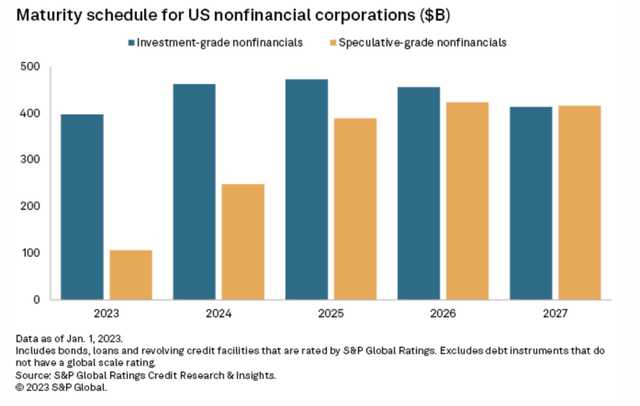

In 2023, about $106.7B of junk debt matures. In 2024, that more than doubles to $247.7B. It will increase again in 2025 to $389.3B. It increases one last time in 2026 to a little over $400B.

Maturity schedule (spglobal.com)

All this debt has to be refinanced and new debt will likely have to be issued.

Refinancing

When it comes time to issue new debt, it won’t be easy for these junk-rated companies. Interest rates are high, and there is a lot of uncertainty about their future. Right now, it would be hard for junk-rated companies to issue new debt with the high current rates. But what about issues in the next few years?

As more economic data comes out, the more it looks like a soft landing is a real possibility. There is a chance that the rates we have now stay for several years. The economy has remained strong as rates shot up and inflation is starting to go down. This would mean that the Fed has no reason to cut rates.

High-interest rates are bad for junk debt issuance. These junk-rated companies are already in financial trouble and now they won’t be able to issue cheap debt. That’s a recipe for disaster.

Another scenario

Even if rates don’t stay high, the other scenarios are just as bad if not worse. Let’s first look at the inverse of the above scenario where rates stay high. Let’s imagine that rates get cut back to near zero as they were during the pandemic. This would mean that there is another era of cheap borrowing, making it easy for junk-rated companies to refinance. But why would rates be cut that low? A severe recession. A recession hurts the economy as a whole, but will definitely hurt junk-rated companies more. They are already struggling and a recession will add to that, making defaults rise. So although cheap debt can be issued, default risk goes up.

What I forecast

While the two scenarios above are absolutely possible, I believe the outcome will be somewhere in between. The Fed will lower rates to about 3-4% and whether you want to call that a mild recession or a soft landing, there will be some economic slowdown. This isn’t ideal for junk bonds. Rates will still be far higher than they were during the pandemic era and the economic slowdown will hurt these already struggling companies.

What this all means for SHYG

SHYG holds short-term junk bonds. These will be the bonds that default. Companies may not have the cash to pay the bond owner and issuing new debt to pay the bond owners back will be expensive. As the maturity wall gets closer, expect to see more junk bond defaults.

Conclusion

Junk bonds as a whole are overpriced. However, things look even worse for short-term junk bonds. As the $785 billion junk-bond maturity wall draws closer, junk-rated companies are scrambling to be able to pay it all to their bond owners. Whether rates go down or stay high, there isn’t a positive scenario for short-term junk bonds. I rate SHYG a Sell.

Read the full article here