Elevator Pitch

I have a Buy rating assigned to SK Telecom Co., Ltd. (NYSE:SKM) [017670:KS] shares.

My previous July 10, 2023 article was focused on SKM’s metaverse platform referred to as ifland, and the company’s share buybacks. I turn my attention now to SK Telecom’s artificial intelligence (“AI”) investment plan and its future dividends in this write-up.

SK Telecom’s plans for accelerated AI investments put the company in a good position to meet its 2028 top line goal of KRW25 trillion. Separately, the stock offers an appealing high single-digit percentage dividend yield, which I view as sustainable. Therefore, I continue to have a bullish opinion of SKM stock.

2028 Revenue Goal Will Be Supported By Increased AI Investments

Late last month, SK Telecom issued a press release revealing the company’s top line target for 2028 and its plans to accelerate investments in AI-related areas.

SKM aims to deliver a 2028 revenue of KRW25 trillion. Considering that the company registered sales of KRW12.4 trillion in 2022, SK Telecom’s recently disclosed financial goal translates into an impressive top line CAGR of +12.4% during the 2022-2028 time period. As a comparison, SKM’s actual revenue CAGR for the 2006-2022 time frame was just +1.0% as per S&P Capital IQ data.

According to CEO Ryu Young-sang’s comments at a media briefing last month cited in a September 26, 2023 The Korea Times article, SKM:

“invested 12 percent of our capital in AI” between 2019 and 2023, and the company targets to “increase it (proportion of AI investments) to 33 percent over the next five years.”

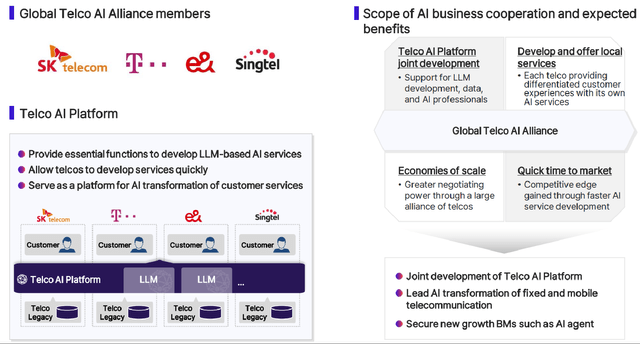

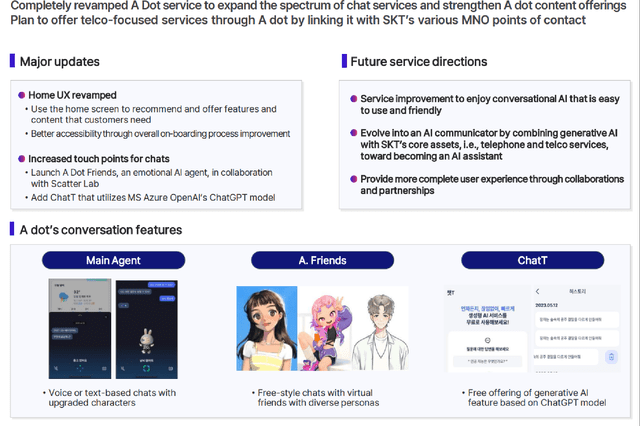

A key revenue growth driver for SK Telecom is the rollout of AI services in international markets by collaborating with other foreign telecommunications services companies. In its September 25, 2023 press release which I referred to earlier, SKM highlighted that it plans on “launching personal AI assistant services simultaneously in many countries across the world by working closely with telcos for localization” via the “Global Telco AI Alliance.” The Global Telco AI Alliance (SKM is a member) and SK Telecom’s AI chatbot known as A Dot are detailed in the charts below.

A Brief Overview Of Global Telco AI Alliance

SKM’s Q2 2023 Results Presentation

New Features And Potential Improvements For SKM’s AI Chatbot A Dot

SKM’s Q2 2023 Results Presentation

It is reasonable to expect that SK Telecom’s increased AI investments will enable the company to grow its revenue contribution from AI-related products and services. For example, the company’s AI chatbot A Dot has the potential to be introduced in a greater number of markets in a shorter period of time, if SKM is willingly to allocate more funds in this particular area.

Referring back to The Korea Times news article published on September 26, CEO Ryu Young-sang emphasized at the media briefing that the announcements relating to an increase in AI investments and its 2028 top line goal are actions taken to allow SK Telecom to “be better valued by the market.”

SK Telecom is currently trading at undemanding consensus forward next twelve months’ price-to-revenue and EV/EBITDA multiples of 0.59 times and 3.8 times (source: S&P Capital IQ), respectively. Assuming that SK Telecom’s revenue growth accelerates and a larger proportion of its sales is derived from AI services going forward, it will be realistic for SKM to command higher valuation multiples in the future.

A Dividend Cut For SK Telecom Is Unlikely

SKM’s consensus forward dividend yield is an attractive 7.0%. SK Telecom has a good track record of dividend distributions, considering that it consistently paid out dividends of KRW830 per share for the past six quarters.

But there are certain analysts who are worried that SK Telecom might not be able to maintain its current quarterly dividend payout for two reasons.

Firstly, SK Telecom has a new share repurchase plan, and this raises questions of whether SKM will prioritize buybacks over dividends in view of the undervaluation of its shares. SKM’s new share buyback authorization allows the company to spend as much as KRW300 billion to repurchase its own shares between July 27 this year and January 26 next year. At the company’s Q2 2023 earnings briefing, an analyst from Korean securities research firm, eBest Investment, questioned “if there is going to be any impact of such (share buyback) action on your cash dividend.”

Secondly, the future shareholder capital return policy of SKM’s key Korean telecommunications peer, KT Corporation (KT), is in the spotlight. A September 22, 2023 NH Investment & Securities research report (not publicly available) titled “No Need For Worry” mentioned that “KT’s share price has corrected recently on jitters over a possible dividend reduction” based on “the fact that in the past, there were changes in KT’s dividend policy upon the appointment of a new CEO.”

In my opinion, SK Telecom is very likely to stick with the company’s existing dividend payouts. SKM stressed at its second quarter results call that it has “stable operating cash flow” and it is “starting to receive dividends from SK Broadband and the invested companies this year,” which suggests that SKM has sufficient capital to support its share repurchase plan without affecting its dividends. Separately, SK Telecom isn’t undergoing leadership transition, unlike KT Corporation which named a new CEO in August. As such, there is a very low probability of SKM making tweaks to its dividend policy in the foreseeable future.

Concluding Thoughts

SK Telecom Co., Ltd.’s key investment merits are the potential revenue growth acceleration and its consistent dividend payouts. I think that there is a reasonably good chance of valuation multiple expansion for SK Telecom in time to come, which explains my Buy rating for the stock.

Read the full article here