Introduction

SkyWest, Inc. (NASDAQ:SKYW) is the holding company that owns SkyWest Airlines and SkyWest Leasing. At SkyWest Airlines, the company owns nearly 500 aircraft that connect millions of travelers each month (over 38 million annually) to over 250 destinations across North America. The company has about 1800 daily flights. Its fleet of aircraft includes 89 CRJ200 aircraft, 105 CRJ700 aircraft, 41 CRJ900 aircraft, and 240 E175 aircraft.

Over the years, SkyWest has emerged from the pandemic as the strongest American regional airline. That’s a big claim, but one backed up by its results. Coming out of a nightmare situation during the pandemic, the company has unlocked significantly better asset utilization, which has translated to revenue growth and margin expansion. The company has significant operating leverage to continue expanding margins, and the Embraer aircraft in its fleet will be fully paid for starting in 2026. In my view, as pilot staffing continues to improve, lighter capex needs should boost the company’s free cash flow profile and translate to strong shareholder returns. In this article, I’ll discuss my outlook for the company, my thoughts on valuation, and why I believe the SkyWest story is underappreciated by the market.

Company Website

Investment Thesis

Over the last few years, U.S. regional airlines faced significant crises which put their businesses at risk. The first was a global pandemic where fears with respect to COVID-19 put a damper on travel as travelers were forced to stay home due to lockdowns and most were afraid to travel even after that. The second was a pilot shortage, where the pandemic accelerated the retirements of pilots, many of whom were already near retirement. These issues, among many others, meant that many of the regional operators faced significantly worse balance sheets. The burden of long-term debt and dilution to equity holders put off most investors as the outlook looked very weak.

Today, some of that is now behind us, but these challenges have shown who will be and who won’t be the long-term winners. With respect to SkyWest, the company is now seeing higher demand, as demand for regional capacity is consolidating around SkyWest, Republic, and the wholly owned regional airlines (Endeavor, Envoy, PSA, Piedmont, and Horizon) with the smaller third-party carriers losing significant share. In my view, this should allow SkyWest to continue taking share from competitors. As I’ll discuss later, SkyWest has a decent balance sheet that’s well-positioned relative to struggling smaller carriers.

Another key point to my investment thesis is that SkyWest has managed the pilot situation much better than peers. To fill their own gaps when post-pandemic demand for flights skyrocketed, the U.S. major airlines, to have recruited heavily from the regionals, effectively stealing their pilots from underneath them. At many of the larger careers, the minimum requirements have changed to be more relaxed. Whereas it used to be a minimum of a bachelor’s degree and a minimum of 2,000 hr. of command experience before they would be considered by a major, many of those qualifications are now removed.

While SkyWest is still doing much better than other regionals, it is still short by 2000 pilots relative to demand. Compared to pre-pandemic, when they had about 5400 pilots, today, they are now short by 1000 and could still use another 1000, given demand. While it will take several years for demand and supply to reach equilibrium, I believe SkyWest is well positioned to continue taking share from competitors, particularly from regionals.

In my view, SkyWest could see a multi-year improvement in both margins and free cash flow as better pilot staffing drives higher revenue production and more and more of the debt associated with the E175 fleet begins to be fully paid off. By year-end 2024, optimization of the Embraer should be close to full utilization. On the latest earnings call management expects that they should be able to increase CRJ flying by 30% as captain staffing is solved.

Recent Results

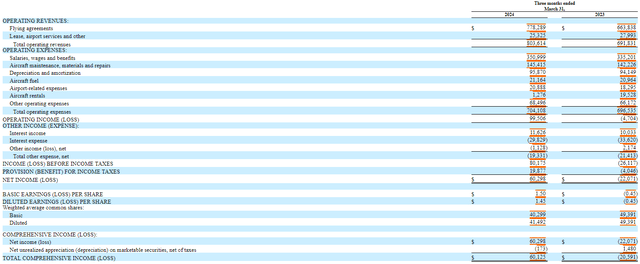

When looking at the recent results for SkyWest, the company reported revenue of $804mm, which was up 16.2% year over year, primarily as a result of flying contract rate increases along with higher production for the quarter. On margins, operating margins clocked in at 12.4%, about 3.4 percentage points better than analyst estimates of 9.0% (source: Bloomberg). Block hours for the quarter were 4.9% higher year over year but were essentially flat compared to Q4’23.

Company Filings

Overall, I think the outlook looks pretty strong for SkyWest. Block hours are projected to be up 6% sequentially next year, driven by a meaningful improvement in captain attrition (adding net new captains each month during the quarter) along with strong demand from flying partners. With modest capex needs, I expect that this incremental demand will boost margins and trickle down to FCF growth.

With the free cash flow, I expect that management will be active in buying back stock. Back in May 2023, the company authorized a share repurchase plan to buy up to $250 million of company shares. As at the end of the quarter, there was $82.2 million available under the May authorization. I wouldn’t be surprised to see the buyback limit renewed and upped next quarter.

With respect to the balance sheet, SkyWest is in a strong position. As per the company’s filings, it has 202 debt-financed E175s and took delivery of over half of these between 2014 and 2017. The debt used to acquire these aircraft is 12-year fully amortizing, so they will begin to be fully paid off in 2026. Per management, they are expected to have over 13 years of remaining life after the debt is paid. At the end of the quarter, the company had a net leverage of 3.6x compared to 4.9x just six months ago. About 41% of the 475 aircraft that are in scheduled service are owned outright.

Company Filings

Net debt is now lower than pre-pandemic levels. Following the planned repayment of $400mm in debt by the end of the year, the company’s debt could be at the lowest point it’s ever been in over a decade (source: S&P Capital IQ).

The airline industry is a slow-growing, mature industry. Despite this, I still think SkyWest has opportunities for growth. Management expects 100 65-76 seat aircraft to be made available by its mainline partners, and it should be in a strong position to win a lot of this business. During the last few years, I’m of the news that management has shown forward-thinking during the last few years, especially in extracting value from its CRJ-200 fleet. These assets are fully depreciated and unencumbered. From an accounting perspective, that’s great because that expense has already been recorded. At the same time, in practice, management is monetizing them through multiple initiatives, including SkyWest Charter and its investment and arrangement with Contour.

Valuation and Wrap Up

From a valuation perspective, consensus EPS estimates for SkyWest are at $6.56 in 2024 and $7.56 in 2025. This implies that the company is trading for 12.2x earnings or 10.6x on a forward basis. Overall, I find the valuation to be quite reasonable, despite the share price run-up. For one thing, I don’t think we are at peak earnings yet; historically, SKYW has traded in the low double-digit P/E multiples in prior growth cycles. As a cyclical stock, I wouldn’t be inclined to hold the company long-term, but letting the stock run its course makes a lot of sense, in my view. With a positive outlook and a track record of navigating recent difficult periods well, SkyWest deserves its premium valuation. While there are risks to any investment (continued industry uncertainty around the lack of qualified pilots, economic weakness, and the threat of pandemics, terrorism, and war), I SkyWest offers compelling value at the current price and is a best-in-class operator. As such, I rate shares a ‘buy’ and would consider adding on any short-term dips.

Read the full article here