Article Thesis

Sociedad Química y Minera de Chile S.A. (NYSE:SQM) is a leading lithium miner that has seen its shares come under pressure in the recent past. Weak EV sales are a headwind right now, but the longer-term picture is still positive. For someone looking for exposure to the lithium market, Sociedad Química y Minera de Chile S.A. could be worth a closer look.

Past Coverage

I have covered Sociedad Química y Minera de Chile S.A. in the past here on Seeking Alpha, most recently in February, around four months ago. I gave the company a “Buy” rating back then, which, so far, has not worked out well, as Sociedad Química y Minera de Chile S.A. continued to pull back recently on the back of a weak overall EV market around the world. Still, the longer-term picture remains positive, and volatility had to be expected for SQM — the same holds true for all kinds of materials and commodity plays.

SQM: Recent Results

The company reported its first-quarter earnings results since I last covered Sociedad Química y Minera de Chile S.A., which is why we should take a look at what is happening at the company right now.

The company recorded revenues of $1.08 billion, which was down by a hefty 52% compared to the previous year’s quarter. This was the result of weak lithium pricing, as Sociedad Química y Minera de Chile did not see its sales volumes decline. In fact, the company saw its lithium sales volumes expand by around 30% compared to the previous year’s first quarter, but pricing headwinds more than offset the increased volumes that were made possible by SQM’s ongoing investments in new production.

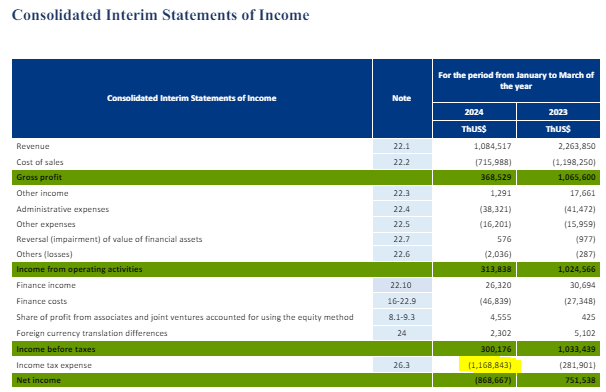

On a GAAP basis, SQM recorded a net loss of $3.04 per share, or around $870 million on a company-wide basis. But this was primarily the result of hefty taxes during the quarter, as we can see in the following table:

SQM net loss (SQM presentation)

SQM paid income taxes that were way higher than the company’s operating profits, which caused a substantial net loss during the period. This is not reflective of the typical income tax expense and was a one-time issue. The company’s CFO explained during the earnings call (emphasis added):

Our net profit was impacted by a one-time adjustment related to the accounting treatment of the lithium mining tax in Chile from previous years, adding up to almost $1.1 billion as of March 31, 2024. This is not having a significant cash impact since the majority of this amount close to $930 million was paid in prior years.

With this tax expense being related to several years in the past, and with most of it being paid in the past, thus not causing a substantial cash impact in 2024, this was mainly an accounting item. As this issue has now been dealt with, taxes should be considerably lower in the future, and SQM should be profitable again, all else equal. After all, if the tax rate had been flat year-over-year, the company would have recorded a net profit of around $220 million in the first quarter of the current year, versus a GAAP net loss of more than $800 million. Not surprisingly, analysts are thus forecasting that the company will generate positive profits this year, as Q2 to Q4 should be meaningfully better again. The analyst consensus estimate sees earnings per share of around $3.80 for the current year, which pencils out to around $1.1 billion on a company-wide basis.

The Global EV Market Is Going Through A Tough Time

While lithium is used in all kinds of batteries, including for phones, notebooks, and so on, electric vehicles use way larger batteries compared to other tech products. Naturally, lithium demand is thus heavily impacted by EV sales numbers. We saw this during the pandemic, when EV sales were booming and when lithium prices exploded upwards. But enthusiasm for EVs has waned to some degree in recent quarters, which is why sales growth has come down. In some markets, EV sales are even declining compared to a year ago, with lower incentive spending being a headwind for EV markets in France, Germany, etc.

In the United States, the EV market is looking slightly stronger, but with a growth rate of 7% in the first quarter, growth isn’t particularly strong, either. China is showing the best growth, with policies to combat air pollution being an important growth driver, but some other Asian markets including Japan and South Korea experienced sales declines for EVs during the first quarter (see link above).

Overall, the global EV market is thus in a tough spot. While growth was excellent during the pandemic, with companies also benefitting from strong prices that allowed for substantial margin increases (e.g. at Tesla (TSLA)), the market is now far more saturated. Margins are coming down due to pricing pressures, and it looks like some EV players overbuilt capacity, as sales in 2024 are lower than previously thought.

The same appears to be true for major supplier industries, including lithium mining — strong EV sales growth a couple of years ago resulted in strong profits for lithium miners, and they decided to invest heavily in new capacity. As EV sales are now growing at a slower pace, the lithium market is relatively saturated, and lithium prices are low. The good news is that “the cure for low prices is low prices.”

In other words, capacity expansion has now become less attractive for lithium miners, which is why they won’t invest a lot in new supply. With the EV market still growing in 2024 and beyond (although at a somewhat slower pace), the current oversupply will end eventually and lithium prices should improve again. These cycles are relatively common across all kinds of resource industries, as high prices cause increased investments, which cause lower prices, which cause lower investments, which cause higher prices, and so on.

For someone with a long-term investment focus, the quarter-to-quarter price swings for lithium and the ups and downs in the profits of companies such as SQM should not be all-important. As long as the longer-term thesis is intact, SQM should remain a solid investment choice. In this case, the longer-term thesis is that EV sales will grow throughout the coming decade and beyond, even if there will be some years with weaker growth and some years with stronger growth. More EV sales mean that more lithium is needed, and someone has to supply it.

Is SQM A Good Investment?

While the lithium market is rather weak today due to supply being high while demand is growing at a lower rate than previously thought, lithium ultimately is a growth market. And Sociedad Química y Minera de Chile is one of the largest players in this industry, with a market share of around 20%. SQM could thus be a solid investment eventually, although investors will always have to live with the ups and downs throughout the lithium cycle.

SQM trades for just 10.5x this year’s expected net profits, which is not a high valuation, considering 2024 will be a rather weak year profit-wise. While analyst estimates should be taken with a grain of salt, the current consensus estimate for next year implies that SQM will grow its earnings per share by a massive 67% in 2025. This means that SQM is currently trading for just above 6x next year’s expected earnings, which is a pretty low valuation.

There are some political risks, as government intervention in Chile is possible, which may help explain the rather low forward valuation for SQM’s stock. Competitors such as Albemarle Corporation (ALB) face fewer political risks, but then again, Albemarle trades for more than 30x net profits, which makes for a 200%+ premium compared to SQM.

Lithium price swings and political risks shouldn’t be neglected, but for those who can stomach these, SQM could be an attractive longer-term investment. After all, despite the current issues in the EV market, it is highly likely that the number of EVs being sold a decade from now is much higher compared to this year. One of the largest lithium suppliers could be a key beneficiary of this trend.

Read the full article here