Editor’s note: Seeking Alpha is proud to welcome Saira Quraishi as a new contributing analyst. You can become one too! Share your best investment idea by submitting your article for review to our editors. Get published, earn money, and unlock exclusive SA Premium access. Click here to find out more »

Investment Thesis

SoundHound AI (NASDAQ:SOUN) is a transformative player in the AI-driven voice and conversational intelligence market. Over the last two years, the company’s trailing revenue has skyrocketed from $20 million to $55 million, showcasing remarkable growth that, in my view, is only just beginning. SoundHound’s debt-free balance sheet, strategic acquisitions, and impressive revenue growth make it one of the most attractive growth stocks in the AI landscape today. With a customer base across automotive and restaurant industries and strategic acquisitions will allow it to capture the growing demand for voice AI solutions. I believe that the company’s huge backlog of long-term contracts is accelerating the revenue growth and strategic positioning in new verticals make it a compelling investment opportunity.

The company’s voice AI solutions are now integrated into major automotive brands including Stellantis vehicles, Hyundai, and also have penetrated the restaurant industry which constitute 25% of SoundHound’s overall revenue. According to my research, SoundHound’s voice AI technology is gaining traction not just because of its core functionality but also due to its integration with popular generative AI models like ChatGPT.

SoundHound’s recent acquisitions of Amelia, an enterprise conversational AI leader, and Allset, a restaurant ordering platform, signal the company’s intent to broaden its market reach. These acquisitions are strategic as they position SoundHound to diversify its revenue streams and capitalize on opportunities in other industries such as finance, healthcare, and insurance. The company’s management believes that this diversified approach will mitigate risk and offer new avenues for growth.

However, these acquisitions come with a cost. The company’s gross profit margins have been declining, dropping to 63% in the second quarter, down from previous levels. This margin contraction is largely attributed to integration costs and redundancies associated with recent acquisitions. In my opinion, this is just a temporary setback. As SoundHound optimizes its operations and extracts synergies from these acquisitions, margins are likely to improve and potentially will lead to a more robust and profitable business model by 2025.

Introduction

SoundHound AI is a leading innovator in the voice AI and conversational intelligence space, specializing in speech recognition and natural language processing technologies. Founded in 2005, SoundHound has spent nearly two decades developing voice-enabled AI solutions that power millions of interactions across automotive, restaurant, and various other industries.

The company’s proprietary voice AI technology is designed to enhance user experiences through smart, responsive, and intuitive voice interfaces, positioning SoundHound as a key player in the rapidly growing AI-driven ecosystem. With strategic partnerships, high-profile acquisitions and a strong financial foundation.

SoundHound’s Explosive Revenue Growth

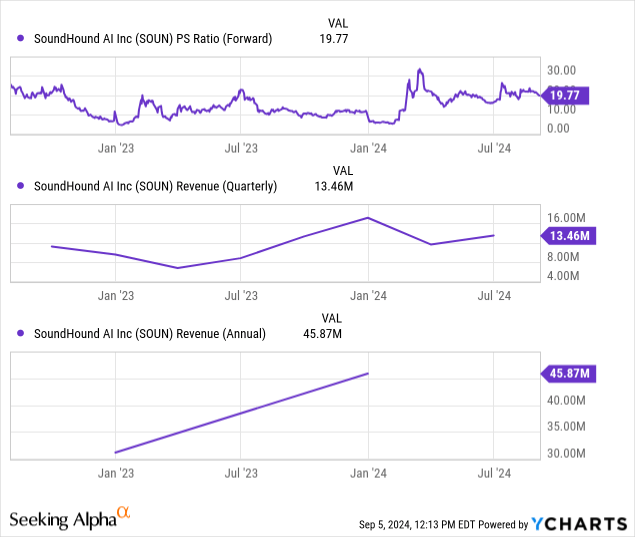

SoundHound has demonstrated an impressive trajectory in revenue growth, nearly tripling its revenue over the past two years. The company recently reported Q2 2024 revenue of $13.5 million, marking a 54% increase from the previous year. This growth is driven by a combination of expanding contracts and successful acquisitions, putting SoundHound well ahead of its competitors in the conversational AI space.

The company’s gross margin has also been solid with non-GAAP gross margins reported at 67% shows SoundHound’s ability to scale its operations efficiently. This margin expansion is mainly because of a significant backlog of long-term contracts that suggests that SoundHound’s revenue growth is sustainable over the coming years.

Strategic Acquisitions And Expanding Reach

One of the most compelling aspects of SoundHound’s strategy is its acquisition of Amelia, a leader in enterprise AI software. This acquisition will allow SoundHound to penetrate new verticals, including finance, insurance, and healthcare. I see this acquisition as a critical step in broadening SoundHound’s market reach and accelerating its revenue growth.

The integration of Amelia will also enhance SoundHound’s ability to offer more comprehensive AI solutions, making it a go-to provider for businesses seeking to integrate conversational AI into their operations. The addition of high-profile clients from the automotive sector like Stellantis, Hyundai, and partnerships with leading QSR (Quick Service Restaurant) brands highlight the growing adoption of SoundHound’s technology.

A Strong Backlog With Long-Term Contracts

SoundHound’s backlog of $723 million in long-term contracts is a testament to the company’s ability to secure multi-year commitments from large, well-established brands. This backlog is growing at an impressive rate, up from $339 million a year ago. This 113% YoY growth rate, which shows the increasing demand for SoundHound’s AI solutions.

The contracts in this backlog are not just placeholders, they represent actionable revenue streams that will be realized over the coming years. In my opinion, this backlog provides a strong foundation for future revenue growth and positions SoundHound as a stable investment in the volatile AI sector.

Improving Financial Metrics Despite Losses

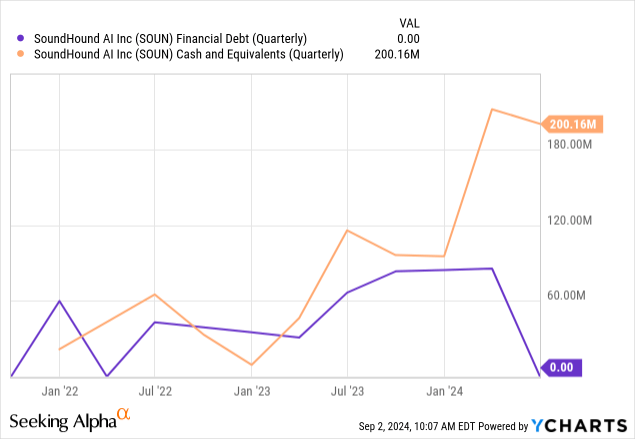

While SoundHound is not yet profitable, there are clear signs of financial improvement. The company’s adjusted net loss narrowed from $20 million in Q1 2024 to $15 million in Q2, indicating that SoundHound is moving in the right direction. Additionally, SoundHound has been proactive in strengthening its balance sheet with over $200 million in cash and prepaid $100 million in debt, saving $55 million in interest and fees.

From my perspective, these actions reflect prudent financial management and suggest that the company is taking the necessary steps to reach profitability. The management has outlined a pathway to achieve operating margins comparable to other software companies, targeting 30% or higher relative to annual revenue over the long term. This forward-looking approach to margin improvement is encouraging for investors seeking long-term value.

Expanding Customer Base And Market Penetration

SoundHound’s expanding presence in the automotive sector is a key growth driver. The company’s voice AI technology is being integrated into vehicles from prominent brands such as Peugeot, Vauxhall, Opel, and Alfa Romeo, among others. Notably, SoundHound is set to roll out its voice assistant with generative AI capabilities across a leading U.S. electric vehicle manufacturer, marking a significant entry into the North American market.

In the restaurant industry, SoundHound’s AI solutions have been embraced by major chains like White Castle, Jersey Mike’s, and Beef ‘O’ Brady’s. The company’s AI ordering systems are transforming the way these businesses operate, enhancing customer experience while driving operational efficiencies. I believe this broad adoption serves as a strong validation of SoundHound’s technology and its potential to capture market share in other sectors.

Valuation And Price Target Analysis

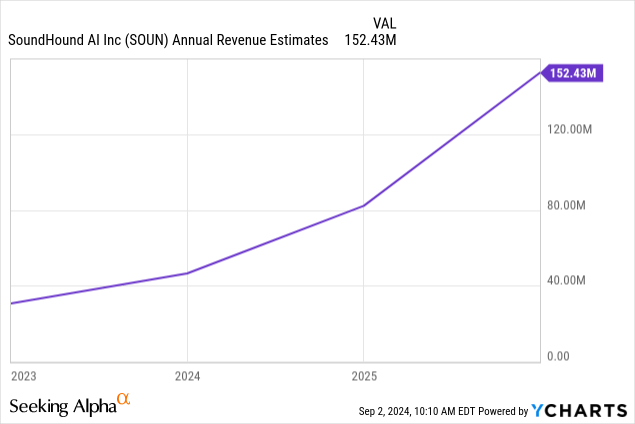

Given the current market cap of approximately $1.58 billion and SoundHound’s expected revenue growth, I believe the stock is undervalued compared to the rest of stock in the tech sector. SoundHound’s guidance suggests revenue could exceed $80 million by the end of 2024 and $150 million in 2025 driven by the Amelia acquisition and expanding market opportunities. If SoundHound can achieve these targets, its stock could easily justify a price closer to $15 per share over the next couple of years, representing an over 3x return from current levels.

Despite the strong growth prospects, there are risks to consider. SoundHound is still unprofitable, and any delays in achieving profitability or integrating acquisitions could weigh on the stock. Additionally, competition from larger players like Google, Amazon, and Microsoft, which are also heavily investing in voice AI, could pose challenges. However, SoundHound’s niche focus on automotive and restaurant applications provides a distinct competitive advantage that helps mitigate these risks.

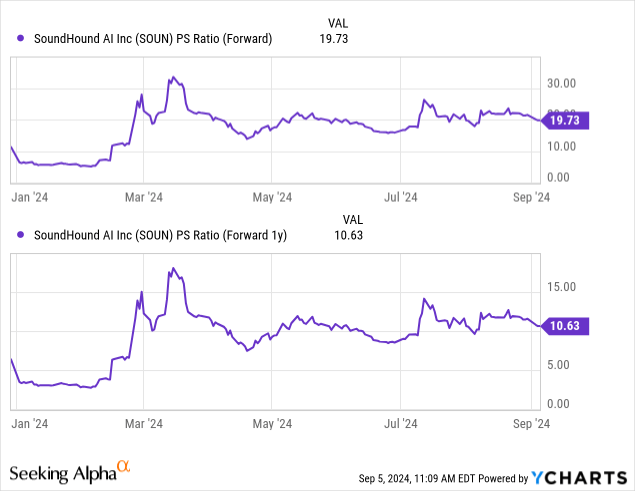

Given SoundHound AI’s early-stage nature and robust growth, I use a Revenue Multiple approach, as this is the most appropriate method for high-growth tech companies that are not yet profitable. With the market cap of $1.58 billion, the company is slightly overvalued based on its current and projected revenue growth.

Current Revenue Multiple Calculation

Current Market Capitalization: $1.58 billion 2024 Projected Revenue: $80 million

Price-to-Sales (P/S) Ratio Calculation:

-

P/S Ratio = Market Cap / Projected Revenue (2024)

-

P/S Ratio = $1.58 billion / $80 million = 19.73x

2025 Projected Revenue: $150 million:

- P/S Ratio (2025) = $1.58 billion / $150 million = 10.63x

Data by YCharts

Industry Benchmarking and Comparison

SoundHound’s current and forward-looking P/S ratios place it on the higher end compared to industry peers:

-

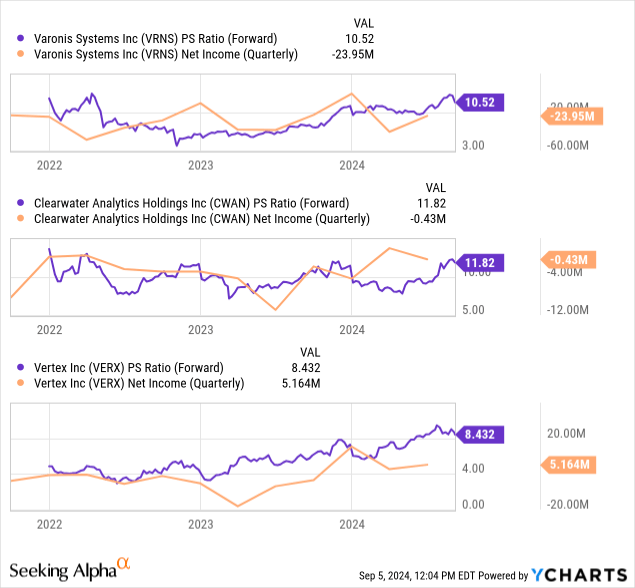

High-Growth AI Companies (7x to 12x P/S): Firms like Varonis Systems (VRNS), Clearwater Analytics (CWAN), and Vertex (VERX) and other growth-stage AI companies often traded at similar or slightly lower multiples, particularly when they have shown a clearer path to profitability.

With a current P/S ratio of approximately 19.73x based on 2024 projected revenue, SoundHound AI is trading at a higher premium to many of its industry peers. This premium reflects market expectations of continued high growth and successful execution of its backlog and strategic initiatives.

Valuation Insights

Given the above multiples, SoundHound’s current valuation implies high expectations for future performance:

High Premium for Growth: The 19.73x P/S ratio for 2024 suggests that investors are pricing in not just current growth but also significant future execution, likely banking on the full conversion of its backlog and continued expansion into new markets.

According to the metrics above, SoundHound AI is slightly overvalued, but it is mainly because the overall tech sector is much overvalued because of the AI Boom. I don’t think the stock price will go below $4 because they have enough cash to burn for the next 6 quarters if the losses continue at the same pace, but that is less likely to happen. The company’s losses are decreasing each quarter, and it is expected to reach profitability by early 2025, making the price range of $4.20 to $4.80 reasonable. Importantly, with a short float exceeding 23%, any continued positive momentum could lead to short covering, potentially driving the stock price higher.

Is SoundHound AI Overvalued?

Yes, SoundHound AI is currently overvalued based on traditional revenue multiples relative to its peers, particularly in the short term. The market cap of $1.58 billion and a high P/S ratio of 19.73x (2024) place it significantly above average, suggesting that the market is pricing in a lot of future success today. Here’s why this matters:

-

Execution Risk is High: The premium valuation assumes seamless execution, successful acquisition integrations, and substantial backlog conversion into revenue. Any delays or operational missteps could cause the stock to re-rate downwards.

-

Profitability is Not Yet Visible: Despite narrowing losses, SoundHound still faces challenges in reaching profitability. The high valuation multiple assumes that profitability is on the horizon, but if this is delayed, it could lead to a market correction.

-

Market Sentiment Risk: AI and tech valuations are particularly sensitive to market sentiment. In the event of a broader tech sell-off or negative news specific to SoundHound’s operations, the elevated multiples could contract quickly.

While SoundHound’s growth potentials are strong, investors should be aware that they are paying a premium that reflects high growth expectations and minimal tolerance for execution risk.

For current and prospective investors, this means closely monitoring SoundHound’s quarterly performance, particularly the realization of backlog into tangible revenue and progress towards profitability. Any deviation from high expectations could lead to downward pressure on the stock.

Risks To Consider

SoundHound AI is not without risks, but the combination of its technological capabilities and increasing demand in the market makes it a high-reward play in the burgeoning AI space. For investors looking to capitalize on the next wave of AI innovation, SoundHound offers a unique opportunity to invest in a company that is shaping the future of voice and conversational intelligence.

While SoundHound’s growth potential is notable, investors must be aware of the risks. A key concern is the dilution of shareholders, as the company has increased its share count by over 30% in the past two years. Additionally, SoundHound remains unprofitable, and any further delays in its path to profitability could weigh heavily on its stock. With the Amelia acquisition not expected to be accretive until 2025, there is significant execution risk. Additionally, competition from larger players like Google, Amazon, and Microsoft, which are also heavily investing in AI and voice AI technologies, could pose challenges. However, SoundHound’s niche focus on automotive and restaurant applications provides a distinct competitive advantage that helps mitigate these risks.

Conclusion

SoundHound AI is a compelling investment opportunity for those willing to take on some risk for potentially outsized returns. I believe that SoundHound’s unique focus on voice AI, its expanding market reach through strategic acquisitions, and its solid financial foundation position it well for future growth. While the stock may face short-term challenges as the company works toward profitability, the long-term outlook remains highly attractive.

In my opinion, SoundHound represents a high-conviction buy. The company’s robust financial position, strategic partnerships and accelerating revenue growth create a compelling case for significant upside. While there are risks, I believe SoundHound’s unique market positioning and strong execution make it one of the best growth stocks in the AI space today.

Investors should consider building a position in SoundHound, especially on any dips near the $4.20 support level. I am looking forward to the company’s progress in expanding its contract backlog, new partnership announcements, and revenue growth metrics. If SoundHound continues on its current trajectory, I believe it has the potential to significantly outperform the market over the next 12 to 18 months and beyond.

Read the full article here