I Have Warned You

In late May, I took the contrarian stance that the equities rally will likely gain steam, defying the doom scenarios”; and I set my 2023 end-of-year target price for the S&P 500 (SP500) at ~4,700, at an implied x18 P/E multiple. I argued:

There are undoubtedly some super smart arguments to be made on why the stock market should crash soon (at least these arguments may sound smart, because fear sells). But there is one fundamental rule in trading that overshadows all the analytical ‘sophistication’ of the bears … Whenever the market is going up on bearish news, you better be sure to have a long position!

Then, mid-June I raised my end-of-year expectation for the S&P 500 to ~4,900, as I argued that price momentum, paired with a dovish FED turn, will likely push valuation to a ~x20 P/E.

Today I am confident to reiterate my bullish recommendation on the U.S. stock market, with June core inflation dropping to below 3% YoY – ending central banker’s emergency intervention to dispossess markets of capital. And with the Fed expected to shift dovish, investors should consider that stocks appear undervalued – still! In fact, if investors consider the implied equity risk premium at ~4.5%, and add the ~4% risk-free rate to the equation (10 year treasuries), the CAPM would suggest a ~8.5% implied return investing at current S&P 500 valuation levels. What is not to like here?

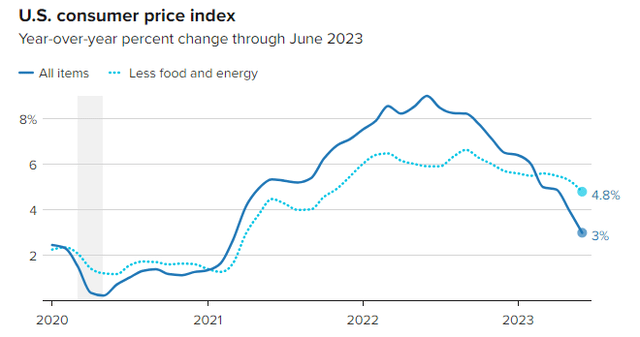

Inflation Now At Fed Target

Although inflation has started to drop materially since late 2022 already, something that I pointed out quite a few times, investors doubted that the disinflation trend would be sustainable. However, the CPI numbers for June should provide reassurance:

- Energy was -16.7% YoY, with gasoline dropping -26.5%

- Other commodities, excluding energy, increased by only 1.3% YoY

- Used car prices dropped 5.2%, after a surge in demand 2021/ 2022

- Core goods prices also experienced a slight decrease

- Food prices are still inflating, recorded at 5% YoY; however, the trend is pointing to a slowdown

Overall, core inflation has now dropped for six consecutive months; and the YoY price growth for June 2023 vs. 2022 is now below 3%!

CNBC

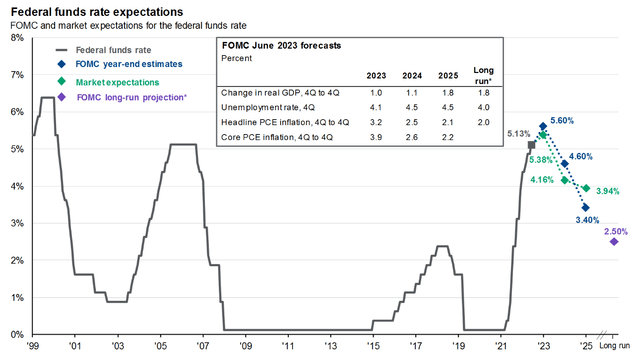

Hello, Fed Pivot

Needless to say — although some investors are certainly still in doubt — the market is right to now price in an end to the Fed’s historic tightening cycle.

Following the June CPI announcement, futures still priced for another 25 basis points, to 5.25%; however, over the following 12 months, investors also price six cuts of 25 basis points each, bringing the fed funds rate to ~3.75% by EOY 2024. While the below chart from J.P Morgan is about 2-3 weeks outdated, it still beautifully highlights how markets and the FOMC think about the yield trajectory – pointing to favorable implications for long-term equity investors.

J.P. Morgan Asset Allocation Research

Welcome Bull Market; Good Bye, Bear Market!

In line with the dovish Fed pivot, I would like to point out that both the S&P 500 and Nasdaq Composite have broken out of the “bear-market territory”, appreciating in value by 16.5% and 33% respectively. But the risk/ reward at current levels is still attractive, especially considering the aggressive market sell-off, and low valuation benchmark at the start of this year.

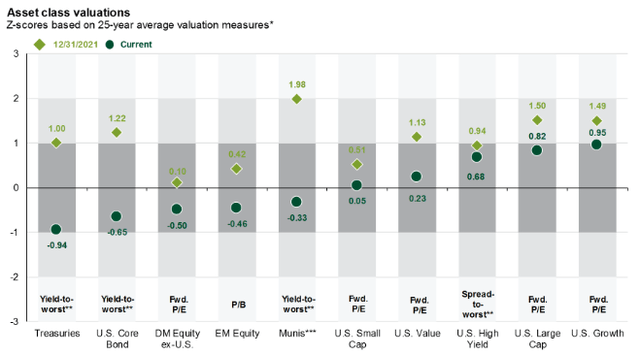

The below graph highlights how major asset classes and styles are valued as compared to their twenty five year historical average, expressed as a z-scores. For reference, z-scores are a statistical measurement that indicates how many standard deviations an data point is away from the mean of a distribution, calculated as …

Z = (X – μ) / σ

… where: Z is the z-score, X is the individual data point, μ is the mean of the data set, σ is the standard deviation of the data set. In that context, a low z-score indicates that the data point is below the mean, and the magnitude of the z-score indicates how far away the data point is from the mean in terms of standard deviations.

As I pointed out in the introduction section of this article stocks, indeed look attractive: While international equities look somewhat discounted at the P/E and P/B reference, U.S. equities are far from stretched in their valuation.

J.P. Morgan Asset Allocation Research

Arguing about the attractiveness of equity investing, J.P. Morgan analysts go on to explain:

When investors feel gloomy and worried about the outlook, their natural tendency is to sell risk assets. However, history suggests that trying to time markets in this way is a mistake. This slide shows consumer sentiment over the past 50 years, with 9 distinct peaks and troughs, and how much the S&P 500 gained or lost in the 12 months following. On average, buying at a confidence peak returned 3.5% while buying at a trough returned 25%.

Importantly, this is not to suggest that U.S. stocks will return anything like 25.0% in the year ahead, as many other factors will determine that outcome. However, it does suggest that when planning for 2023 and beyond, investors should focus on fundamentals and valuations rather than how they feel about the world

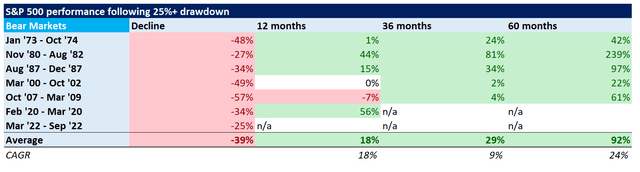

Where The S&P 500 Might Go Next – A Historical Perspective

In theory, a bear market is defined as a price decline of magnitude greater than 20%. Respectively, it would make sense to argue that a bear market ends, once the 20% decline has been recovered.

With that frame of reference, I researched the past 50 years of bear markets, where the S&P 50 price decline has scored a magnitude equal or greater than the ~25% experienced in the Mar ’22 – Sep ’22 episode.

The goal of this research exercise is to show that after the “initial decline”, and subsequent recovery, equity markets have a strong tendency to continue appreciating in value. Notably, for the average of the past bear markets (N=7), markets returned 18%, 29% and 92% for the next 1 year, 3 year, and 5 year period, respectively — materializing a CAGR of 18%, 9% and 24%!

Take a look at the table below, with data retrieved from Refinitiv (Rounding errors possible).

Data Refinitiv; Author’s Calculation

Risks

Of course, investing in equities is not without risks — and the economic challenges still lingering around may not be ignored. That said, I would like to point to four core risk considerations that should always be kept in mind: Market volatility: The S&P 500 can experience significant price fluctuations, leading to potential losses.

-

Economy: The likelihood for a (mild) recession in the U.S. is still pegged somewhere around 50-80%, depending on the analyst. And in a recession, equities may be pressured due to reduced corporate earnings.

-

Sector-specific risks: Certain industries’ performance can impact the index, leading to sector-related vulnerabilities. Specifically, I believe the S&P 500 is currently over-exposed to the big technology companies.

-

Volatility risk: Stocks are volatile by nature. When asked where stocks will do next, legendary financier J.P Morgan commented: “They fluctuate”. Volatility may not be suited (emotionally) for every investor.

-

Long-term commitment: S&P 500 investments require time to realize substantial returns.

Conclusion

Today I am confident to reiterate my bullish recommendation on the U.S. stock market, with June core inflation dropping to below 3% YoY – ending central banker’s emergency intervention to restrict capital. And accordingly, as I expect the Federal Reserve to adopt a more accommodating approach, I view equities as undervalued. In fact, when considering the implied equity risk premium at approximately 4.5% and combining it with the risk-free rate of around 4% offered by 10-year treasuries, the Capital Asset Pricing Model (CAPM) suggests an implied return of approximately 8.5% for investing in the S&P 500 at its current valuation levels.

On The Risks Of Being A Bear

As much as some people advocate for it in their investment analyses, we don’t get a global financial crisis every year. Call me crazy; but I find it just much more appealing to be an optimist about long-term economic growth, technological progress (AI reference driving stocks higher) and people’s ability to avert disaster (government support, etc.), instead of constantly seeking opportunities for negativity and pessimism. And in general about the negativity – judging from a contrarian perspective, the continued negativity in the market can actually be seen as a good sign for investors and risk-seekers. Because, when people are pessimistic about the market, it means there is potential for more buyers to enter the market and push stock prices even higher. In fact, this pattern has been materializing consistently throughout the year, as investors sitting on cash (or even shorting stocks) felt pressured to chase after opportunities for making gains (or buying back stock).

Being always bearish is a fools game – and you have been warned.

Read the full article here