The great growth scare of August 2024 feels like a distant memory. The weekend of August 3 was indeed unsettling, culminating in a sharp global selloff the following Monday. But the bulls stepped up in a big way, particularly after a sanguine ISM Services report Tuesday last week and a better-than-feared Initial Jobless claims update two days later.

The stock market’s rally took a small breather before more non-recessionary data hit the tape earlier this week. July PPI and CPI figures came in on the good side, while Thursday’s Retail Sales report was decidedly above estimates. In net, inflation risks are modest (perhaps even dead) while growth data is not all that bad. Dare I say that is a Goldilocks situation? Less than two weeks removed from a massive volatility spike and the infamous carry-trade unwind, we are back in a favorable macroeconomic backdrop.

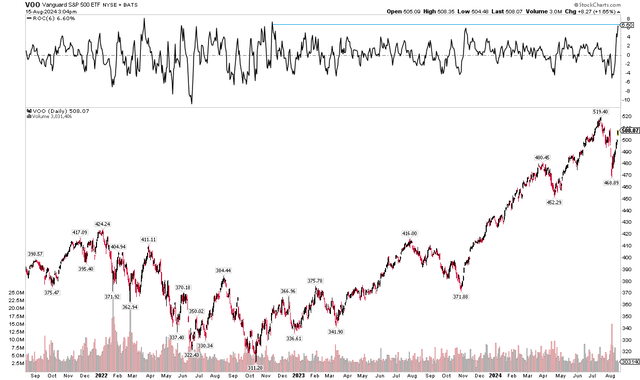

But I am downgrading the Vanguard S&P 500 ETF (NYSEARCA:VOO) from a buy to a hold. I was bullish when the summer began, but given the massive snapback in stocks – the best six-day rally since November 2022 – I see US large-cap equities as sporting a lofty valuation amid weak seasonal trends.

What’s more, there could be cracks in the AI trade. I might be setting myself up for wiping the egg off my face with NVIDIA’s (NVDA) earnings report on tap later this month, but there are some whispers that chip demand could be ebbing. And we’ve seen that play out in modest EPS forecast dips among tech companies.

VOO: Best 6-Day Rally Since November 2022

Stockcharts.com

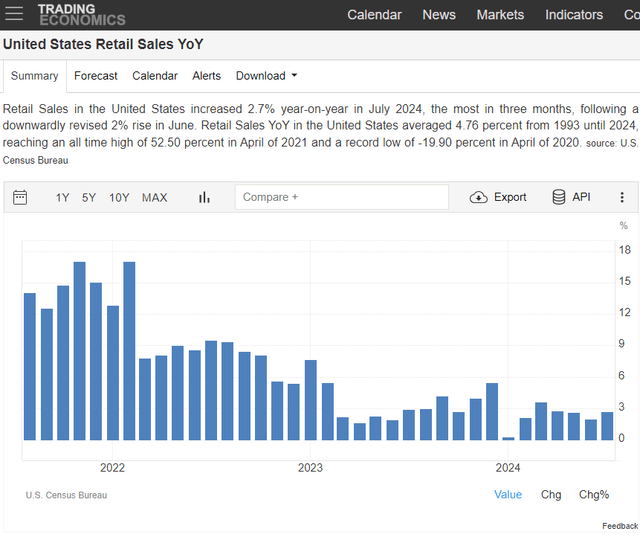

It was just about an all-skate for US and foreign stocks on Thursday following the very strong July Retail Sales report put out by the US Census Bureau. With a gain of 1% versus June, it was the strongest monthly increase since January 2023 as Americans did what they do best. It’s also a good sign for the all-important back-to-school spending shopping season – the second-largest spending period of the year next to the winter holidays, according to the National Retail Federation.

July also marked the first jump in the year-on-year Retail Sales pace since March, helping to assuage risks that households are tapped on with respect to their cash on hand. Of course, we found out earlier this month that Americans are tapping credit cards at a higher rate compared to previous months while both auto and mortgage debt delinquency trends are on the rise, at or near the highest rates going back more than a decade. So long as the jobs market hangs in there, then there’s little reason to expect a protracted hiccup in overall spending.

US Retail Sales Was Stronger Than Forecast in July

Trading Economics

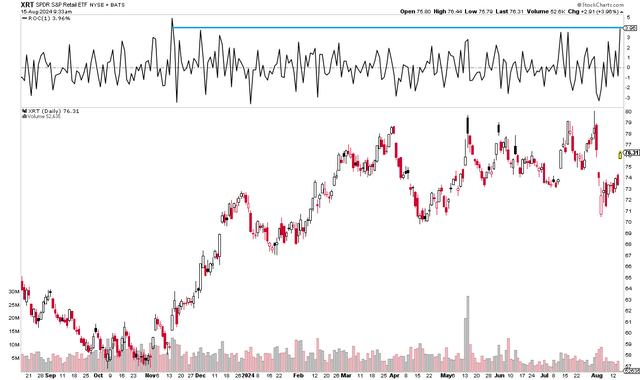

Not surprisingly, it was the retail industry group that helped to lift stocks on August 15. The SPDR S&P Retail ETF (XRT) jumped about 4% for its best single-session going back to last November. More broadly, the Consumer Discretionary sector surged by about 3% thanks to retail share as well as big gains in the sector’s pair of heavy hitters – Amazon (AMZN) and Tesla (TSLA).

The Consumer Discretionary Sector ETF (XLY) enjoyed its best day of 2023, leaping past the previous high watermark set two days earlier.

Retail ETF Enjoys Its Best Day of 2024 Post-Retail Sales Report

Stockcharts.com

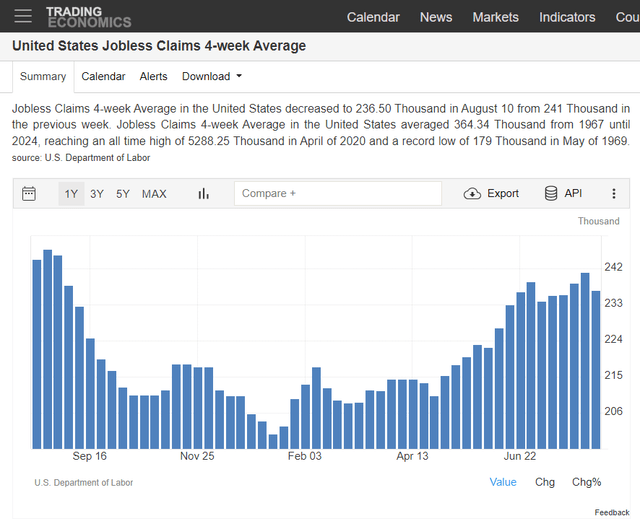

If that doesn’t sound upbeat enough, the latest set of Initial Jobless Claims reveals a pause in what had been a concerning uptrend. The four-week moving average of Initial Claims sunk to 236,500 from 241,000 the previous week.

I assert that this is our best gauge of whether a recession is on the immediate horizon or not. For now, the answer is “not.” We’d need to see a jump to, say, the mid-350,000s to really bring economic contraction risks to the fore.

US Jobless Claims Plateauing, Not A Recession Signal

Trading Economics

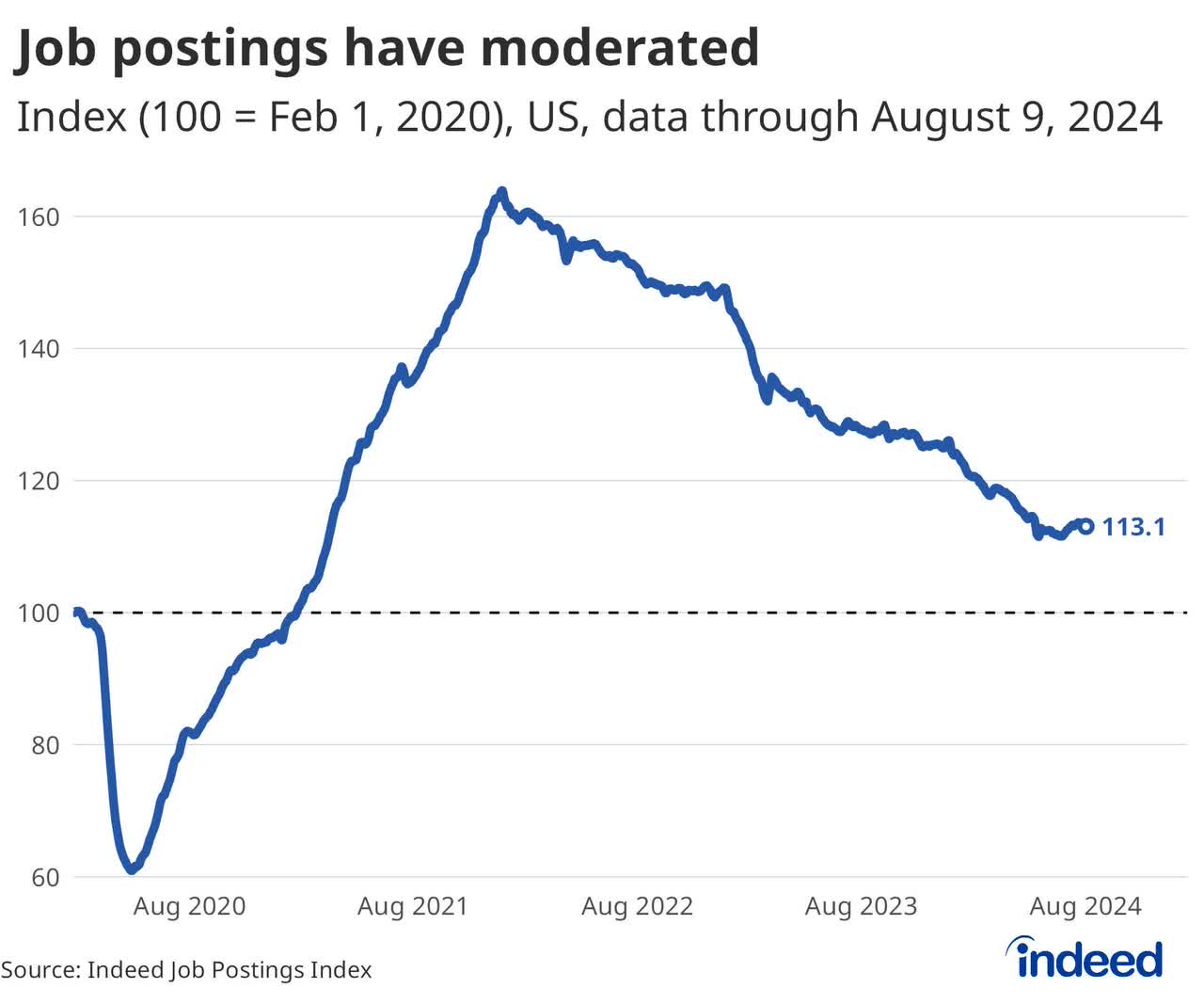

Job Postings Moderating After A Protracted Decline

Indeed

While the growth side of the ledger appears optimistic after the early month scare, inflation is clearly yesterday’s war. It was reported last Wednesday that the July Headline CPI dipped to a fresh cycle low of under 3%. The Core rate, which strips out the volatile food and energy categories, was a touch higher at 3.2%, but about in line with estimates.

The data came after soft PPI numbers on Tuesday. With both reports in hand, macroeconomists now have a decent beat on what the PCE Price Index will verify on the final Friday of the month.

US CPI Rate Fell Further in July

WSJ

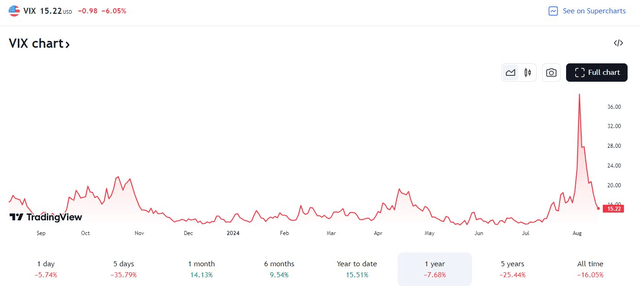

Turning back to price action, the S&P 500 fast fall from 5670 to 5119 culminated in a spike in the VIX to 65 after hanging out in the low to mid-teens for weeks on end. But that volatility surge was deceiving.

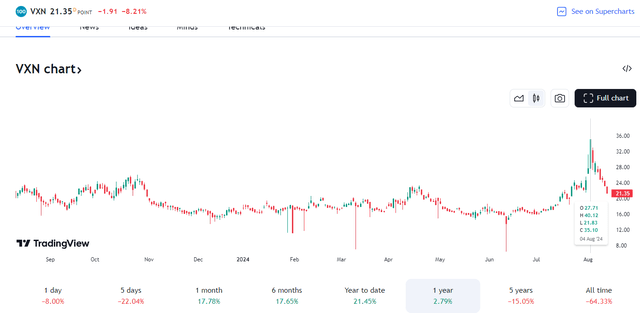

Here’s why: options pricing on the S&P 500 were particularly illiquid on the morning of August 5. That led to the VIX calculation spitting out a non-indicative number. Other implied volatility measures, such as the Nasdaq 100 Volatility Index or the Russell 2000 Volatility Index, were much more tame, closer to 40 or 45 on those normally more volatile indexes.

S&P 500 Volatility Came and Went

TradingView

Nasdaq 100 Volatility Index: Only Spiked to 40

TradingView

Now with 30-day implied volatility back in the mid-teens and the S&P 500 a mere 2.3% from a fresh all-time high, the market’s P/E ratio has returned to about 21, assuming $266 of operating earnings per share over the coming 12 months.

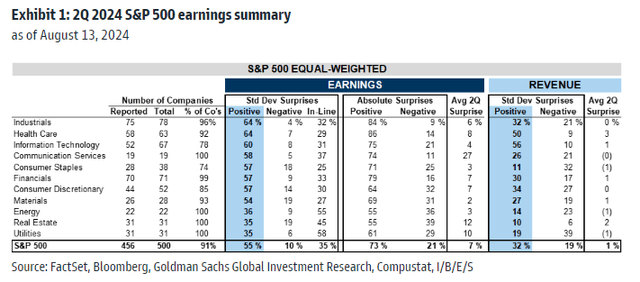

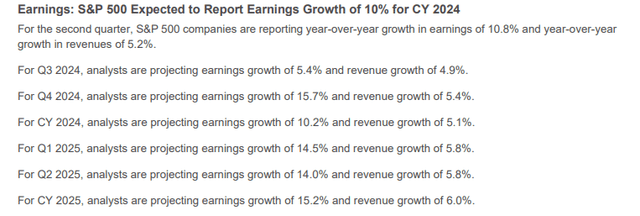

That said, it was a solid Q2 reporting season. Goldman Sachs predicts that the SPX EPS growth rate will verify near 11% compared to Q2 of 2023. While bottom-line growth is expected to dip in Q3, perhaps closer to 5% or 6%, the final quarter of 2024 is forecast to see a double-digit earnings rise.

Q2 S&P Earnings Summary: Strong Positive Surprises

Goldman Sachs

EPS Growth Expected to Dip in Q3, But Then Re-Accelerate in Q4

FactSet

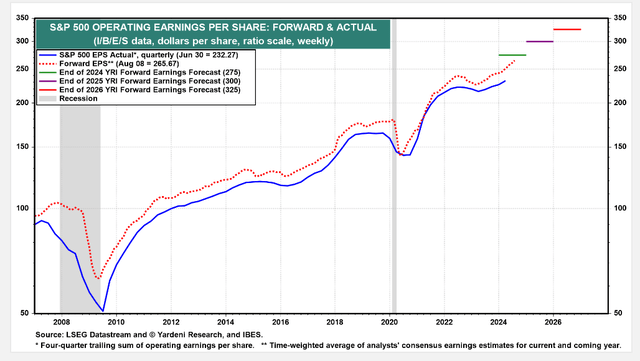

$266 of Non-GAAP EPS Expected on the S&P 500 Next 12 Months

Yardeni Research

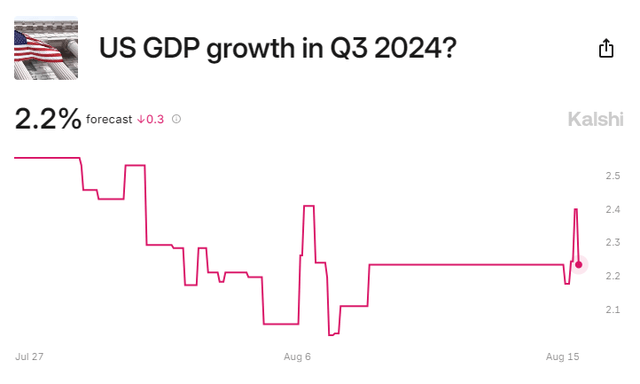

Decent Q3 US Real GDP Growth Expected

Kalshi

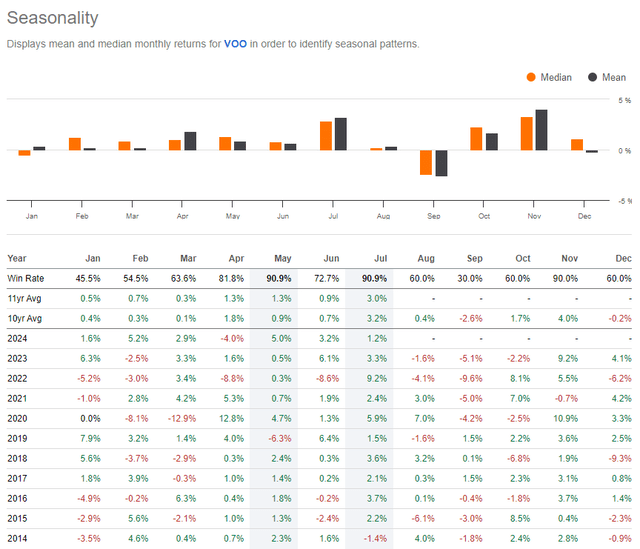

With stocks already back in expensive territory after the short-lived correction, seasonality is a clear headwind for the equity bulls. According to Seeking Alpha’s seasonality tool, VOO has averaged a 2.6% decline in September in data going back to 2014.

Domestic large caps have finished in the red in each of the previous four Septembers, too. I suspect that the onus is on the bulls to beat the trend, and dip-buying could wane now that the strong Q2 reporting period is finishing up.

VOO: Bearish Seasonal Stretch Dead Ahead

Seeking Alpha

The Bottom Line

I have a hold rating on VOO. I see mixed risks, with much better-than-feared macro data coupled with solid earnings. The downside is a high valuation and weak seasonality on tap in the next two months.

Read the full article here